15 Days Price Change

Manika Bhalla

Manika Bhalla

Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills... Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills and a solid foundation in finance. Experienced in financial modeling and valuation, with a keen interest in equity research and investment analysis. Read more

Summary

Hero FinCorp Limited is a rapidly expanding NBFC focused on retail and MSME lending, supported by strong promoter backing from Hero MotoCorp and growing digital capabilities. While AUM and revenue have more than doubled over five years, profitability has come under pressure due to margin compression and rising credit costs. The upcoming IPO and capital infusion aim to strengthen Tier-I capital and support future lending growth. Long-term value creation will depend on stabilising asset quality, improving return ratios, and executing disciplined expansion in high-yield segments.

Hero FinCorp Limited is an NBFC of India that has been instrumental in enhancing the availability of credit to retail and MSME customers in India. The operation of Hero FinCorp within the larger Hero ecosystem has enabled it to grow into a financial services company that provides access to financing that assists the aspirational middle class and the entrepreneurial citizens of India.

Hero FinCorp is positioned between the traditional banking industry and the underserved and unbanked populations and has made it its focus to provide financing to those customers who may be excluded from the traditional banking system's credit criteria.

Hero FinCorp has achieved a strong pan-India presence through a technology-oriented operating model that enables the company to develop and execute scalable operations that provide customised credit products and comply with prudent risk management practices. The use of a dual approach with respect to the delivery of credit products being via traditional methods and digital underwrite enables Hero FinCorp to reduce turnaround time for customers and provide a higher level of customer satisfaction.

Hero FinCorp has a multi-faceted lending business that provides products to retail clients and micro, small and medium enterprises (MSMEs). The company's three primary areas of business include the following:

The company's two-wheeler business drives the continued growth of the company, and customers who are part of the Hero ecosystem (Hero Moto Corp, etc.) give the company a distinct advantage in its financing efforts with the company.

The company's goal in providing these products is to support small companies in upgrading technology, producing new products, and generating additional jobs, therefore creating additional economic activity.

The shareholding structure of Hero FinCorp showcases significant promoter support and also highlights the trust that has been built with institutional investors over time. The primary promoters of Hero FinCorp are the members of the Hero family, with Pawan Munjal in a dominant leadership position as Chairman. In addition, the company has received considerable investment from top-tier global investors and private equity through the years that has strengthened both its capital resources and governance standards. Having reputable institutional shareholders adds transparency, fiscal discipline and aligns with the company’s long-term strategy.

Hero FinCorp’s current shareholdings are comprised of:

The shareholding structure indicates that although the majority of the ownership is considered promoter-led, there is also a significant portion (approximately 19%) of the ownership that is held by non-promoter investors. This illustrates the external, institutional element that represents some degree of oversight as well as the involvement and interest of these independent institutions, creating a balance of governance.

The presence of the major promoters – most notably Hero MotoCorp Ltd. – provides significant strategic, brand credibility and distribution synergies in the overall ecosystem of the business. At the same time, the outspreading of ownership across many external institutions enhances the financial stability and fiscal discipline of the company’s overall capital structure

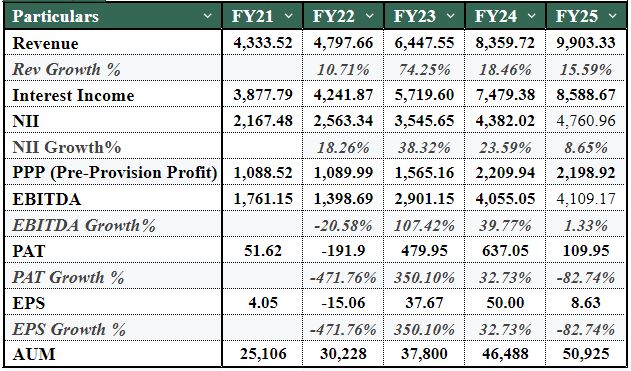

Trends in Profitability and Margin Volatility

Thus, the continued erosion of profitability, despite the continued increase in revenue, tells us that Hero FinCorp is currently experiencing earnings stress.

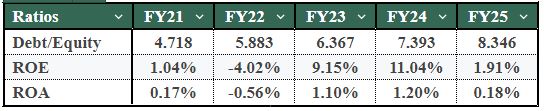

Hero FinCorp continues to develop as an expanding Non-Banking Financial Institution (NBFC) with a solid foundation of sound business practices and a growing size. However, the recent decline in profitability indicates that there are operational costs which must be monitored closely. If profitability continues to improve and the leverage of the business is cautiously managed, the business will be able to establish reasonably consistent future growth; however, if the pressures on earnings continue, the business's future financial stability will be negatively impacted.

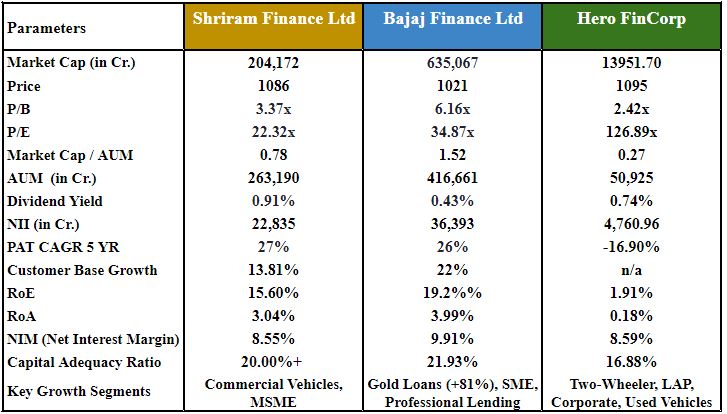

In the non-banking finance company (NBFC) sector in India, Bajaj Finance is the industry benchmark for scale and profitability, and Shriram Finance is the second runner-up with a strong presence in asset-backed lending and vehicle financing. Hero FinCorp has a highly focused and ecosystem-aware lending model, with a defined approach to growth.

While Hero is smaller and less profitable than Bajaj and Shriram, it has substantial lending margin advantages along with conservative underwriting practices. Hero's primary strategic opportunity lies in improving its overall return ratios and achieving operational efficiencies.

As we look towards the future, the outlook for HFCL's growth from FY26 to FY30 is fundamentally positive due to India's evolving demand for credit, MSMEs being formalised and the adoption of digital lending. Additionally, being a systemically important NBFC-ML under the RBI regulatory framework provides HFCL with credibility through regulatory compliance as well as the ability to operate with flexibility.

Key contributors to future growth include:

1. Continued MSME credit growth, where a large proportion of financing needs remain unmet;

2. Increased digital underwriting and collection capabilities result in higher cost efficiencies and less leakage of credit;

3. Ability to increase penetration into underbanked regions, provide portfolio diversification, and

4. Embedded finance partnerships allow for accelerated loan origination at a lower cost of acquisition.

Approval has been granted by SEBI for Hero FinCorp to proceed with an IPO, which now includes both a ₹1,790 crore new issue and a ₹1,568.1 crore OFS.

Before the IPO, Hero FinCorp was able to secure ₹50 crores from Vattikuti Ventures at a price of ₹1,400 per share, resulting in a valuation of the company of ₹25,014 crore. Thus, Hero FinCorp has now raised ₹310 crores towards its planned pre-IPO fundraising target of ₹420 crores.

Also, as a result of this placement, the size of the new issue was reduced from ₹2,100 crores to ₹1,790 crores; the proceeds from which will be applied to enhance the Tier-I capital and to help support lending growth.

Hero FinCorp has a strong footing among the growing Non-Banking Financial Company (NBFC) sector due to its solid fundamentals in lending to individuals and MSMEs, its constant growth in AUM and revenue and a wide range of products from 2W, LAP, Corporate Lending and Vehicle Financing. The Company should also continue growing operationally and reach new customers through its investment in technology (Digital Underwriting) and analytics.

When compared to its larger, more established peers - Bajaj Finance and Shriram Finance, Hero FinCorp has some way to go to catch up on profitability and returns metrics. The Company's RoE and RoA metrics are severely below those of these leading competitors. The Company has experienced earnings fluctuations, margin compressions and will experience further decreases in FY25 and FY26 results due to an increase in credit provisions and higher levels of NPAs, indicating asset quality strain.

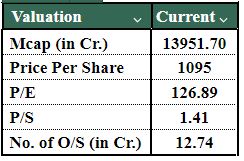

Regarding valuation, Hero FinCorp's multiples are probably stretched compared to its current earnings profile. Unlisted stock data shows this Company is trading on much higher earnings multiples and book multiples as a result of perceived future growth potential versus actual earning potential, as illustrated by comparing valuation multiples for Hero versus its NBFC peers.

Hero FinCorp's future growth potential is based on three things: the company stabilising its credit costs, managing Non-Performing Assets (NPAs), and improving overall profitability. Additionally, Hero FinCorp will have to efficiently deploy its Initial Public Offering (IPO) proceeds to enhance Hero FinCorp's capital ratios and provide the necessary support for future lending growth. Given the resolution of these items, Hero FinCorp may begin to close the gap that exists between Hero FinCorp and its larger competitors.

INVESTOR RECOMMENDATION PERSPECTIVES: Long-term growth-focused investors with higher risk tolerance, especially those interested in early-stage financial investments, may find Hero FinCorp worthwhile if they feel comfortable with Hero FinCorp's overall ability to stabilise margins and execute its growth strategy. Conversely, income-based or risk-averse investors should avoid it. This share is available at SharesCart.

Independent Research Powered By - Actionable data

Comprehensive Equity and Strategic Research Report...

February 2026