15 Days Price Change

URVASHI TOTLA

URVASHI TOTLA

MBA post graduate and CFA Level II cleared, with NISM certifications in Series VIII and XV... MBA post graduate and CFA Level II cleared, with NISM certifications in Series VIII and XV. Skilled in Financial Modeling, Valuation, and Portfolio analysis, with a strong interest in equity research and investment strategies. Read more

Summary

Founded in 2013 as Aspire Home Finance, Motilal Oswal Home Finance (MOHFL) was built to serve one underserved customer — the Indian borrower the big banks turned away. A decade later, it has grown into a ₹4,857 crore loan book spread across 12 states and 112 locations, backed by a CRISIL AA rating and a $60 million commitment from the US Development Finance Corporation.

In the summer of 2013, a quiet subsidiary was registered in Mumbai's Prabhadevi — far from the trading floors and wealth management desks that made Motilal Oswal a household name. Nobody called it a bold bet. Nobody predicted it would one day have 2,780 employees spread across 12 states. It was called Aspire Home Finance Corporation — and its mandate was simple: lend to people the big banks won't touch.

Fast forward to FY25, and that quiet bet has turned into Motilal Oswal Home Finance Limited (MOHFL) — a ₹4,857 crore loan book, a CRISIL AA credit rating, a $60 million commitment from the US government's development finance arm, and a PAT of ₹130 crore that management calls its highest ever.

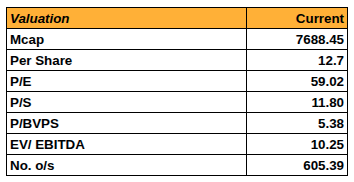

And yet, the stock trades at just ₹12.70 per share — unlisted, thinly known, and quietly debated.

So the question is simple: is this a diamond buried in affordability finance, or a slow-growth lender stuck between ambition and execution?

"We focus exclusively on the lower and middle-income Indian family — the borrower who has a real home to build but no banking relationship to lean on."

— MOHFL Company Philosophy

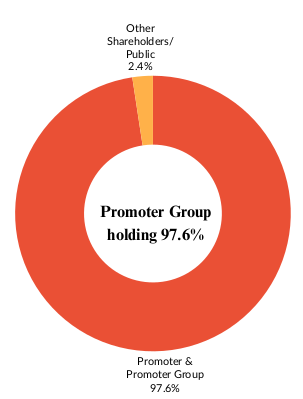

Motilal Oswal Financial Services Limited: ~75.35%

Motilal Oswal Finvest Limited: ~9.94% Motilal Oswal Wealth Limited: ~7.99%

Motilal Oswal Investment Advisors Limited: ~4.32%

Other Shareholders: ~2.40%

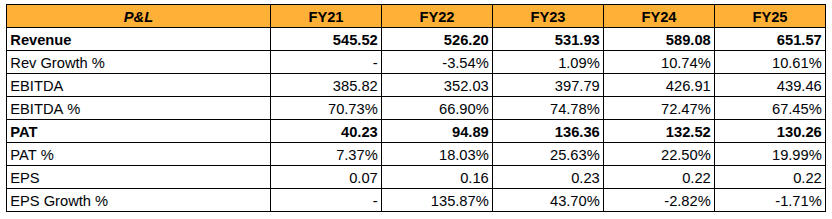

After declining in FY22, revenue growth picked up speed again, reaching ₹652 crore in FY25 with a CAGR of roughly 10–11% from FY23 to FY25.

EBITDA margins were maintained between 67% and 75 %, indicating a high-efficiency cost structure, and operating margins remained structurally strong.

With PAT rising more than 3x from ₹40 crore (FY21) to ₹130 crore (FY25), profitability increased dramatically. After FY23, margins stabilised.

After a robust increase in FY22–FY23, EPS plateaued in FY24–FY25, indicating a slowdown in earnings growth.

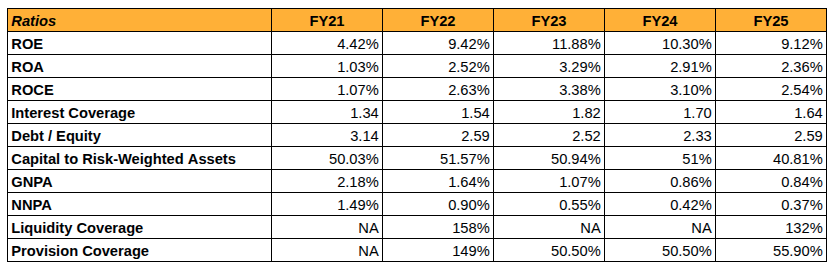

The balance sheet grew steadily, with capital employed surpassing ₹5,130 crore in FY25 and total assets reaching ₹5,530 crore.

In order to support growth, debt increased to ₹3,703 crore while equity increased to ₹1,429 crore, strengthening net worth along with increased leverage.

If there is one number that defines MOHFL's journey, it is the GNPA. In FY21, after years of aggressive lending to informal-economy borrowers — many hit hard by demonetisation, RERA, and Covid — the gross bad loan ratio stood at a worrying 2.18%. By FY25, it has fallen to 0.84%. That's not incremental improvement. That's a fundamental transformation of how the company lends.

The architects of this change: a 5-layer credit approval system based on loan ticket size, a collateral-first underwriting philosophy, and a vertical team structure separating sales, credit, collections, and legal into distinct accountability zones. It is not glamorous. But it works.

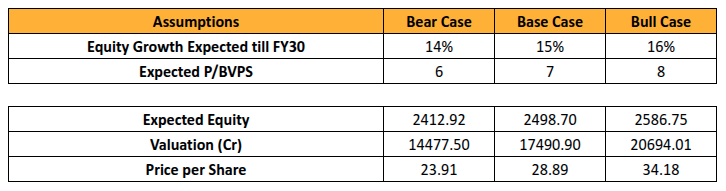

Without making aggressive capital raise assumptions, a 14–16% increase in equity is anticipated until FY30, driven by consistent internal accruals and balance-sheet compounding.

Anchored to P/BV multiples of 6–8x, the valuation reflects scenario-wise differentiation based on execution consistency and return ratios.

With a projected FY30 equity of ₹2,413–2,587 crore, the capital base is expected to continue to grow in all scenarios.

With an implied valuation range of ₹14,478–20,694 crore, it captures both upside potential under sustained execution and downside protection in the bear case.

The base case suggests a balanced risk-reward at ₹28.9, while the estimated price per share ranges from ₹23.9 to ₹34.2.

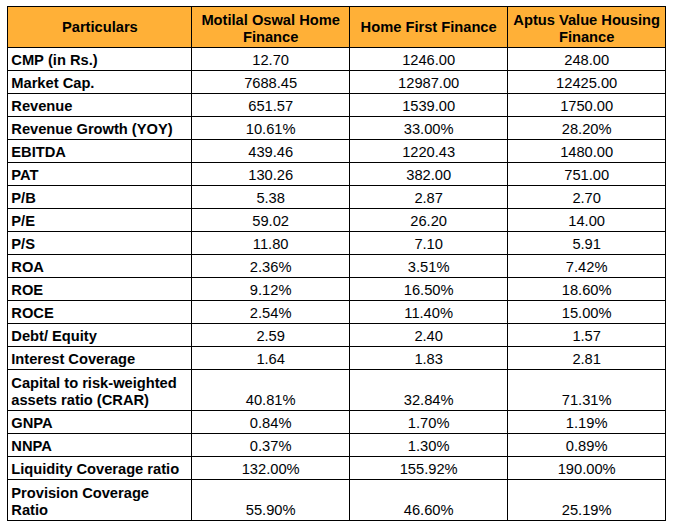

Context matters in finance. MOHFL doesn't operate in isolation — it competes with Home First Finance and Aptus Value Housing Finance, both listed, both aggressive. Here's the honest picture:

Despite having a lower ROE (9.1%), Motilal Oswal Home Finance trades at a clear valuation premium (P/B 5.38x, P/E 59x), suggesting that balance-sheet safety, not earnings strength, is driving pricing.

With YoY revenue growth of 33% and 28%, respectively, Home First Finance and Aptus Value Housing Finance outperform MOHFL's approximately 11%.

With ROEs of 16.5% (Home First) and 18.6% (Aptus) compared to MOHFL's 9.1%, profitability metrics favour peers, with higher ROA and ROCE supporting the former.

With the lowest GNPA (0.84%) and NNPA (0.37%), MOHFL leads in asset quality and demonstrates excellent underwriting discipline.

With a CRAR of 40.8%, comfortably above regulatory requirements, capital strength is still a key differentiator for MOHFL, even though Aptus has a larger buffer.

Motilal Oswal Home Finance is a rare breed in India's lending landscape — a conservatively managed, CRISIL AA-rated housing finance company with a ₹4,857 crore loan book, best-in-class GNPA of 0.84%, and its highest-ever PAT of ₹130 crore, all built on the back of a decade-long mission to serve borrowers that big banks overlook. The balance sheet is strong, asset quality is exemplary, and the long-term housing story is intact — but at a P/E of 59x with ROE slipping to 9.12% and EPS flat for two consecutive years, the stock is priced for safety, not growth. Currently trading in the unlisted market at ₹12.70 per share, MOHFL suits the patient, risk-aware investor who understands the illiquidity premium that comes with unlisted investing — and sharescart.com continues to track it as one of the most closely watched names in the unlisted space, with a base-case FY30 target of ₹28.89 per share and an eye firmly on any IPO or M&A development that could change the story overnight.

Independent Research Powered By - Actionable data

Comprehensive Equity and Strategic Research Report...

February 2026