15 Days Price Change

URVASHI TOTLA

URVASHI TOTLA

MBA post graduate and CFA Level II cleared, with NISM certifications in Series VIII and XV... MBA post graduate and CFA Level II cleared, with NISM certifications in Series VIII and XV. Skilled in Financial Modeling, Valuation, and Portfolio analysis, with a strong interest in equity research and investment strategies. Read more

Summary

GFCL EV Products has rapidly emerged as a strategically critical player in India’s EV battery supply chain, operating in a high-entry-barrier segment of electrolyte and battery materials. Between FY21 and FY23, the company scaled aggressively, supported by strong EV demand, capacity expansion, and deep fluorine chemistry expertise from its parent, Gujarat Fluorochemicals (INOXGFL Group).

FY24–FY25, however, marked a cyclical slowdown, with moderation in revenues, margin pressure, and lower return ratios driven by EV demand softening and inventory correction across the battery value chain. Importantly, unlike many high-growth peers, GFCL EV enters this phase with a strong balance sheet, conservative leverage, and robust solvency, positioning it well for a recovery as utilisation normalises.

GFCL EV Products Limited was founded in 2021 as a fully owned subsidiary of Gujarat Fluorochemicals Limited, which is part of the INOXGFL Group. The company aims to create a supply chain for electric vehicle and energy-storage battery materials both domestically and globally. This area relies heavily on chemistry, emphasizes safety, and requires a lot of capital.

GFCL EV works in the early stages of the battery value chain. It provides battery manufacturers and energy storage companies with essential materials that affect battery performance, safety, and lifespan.

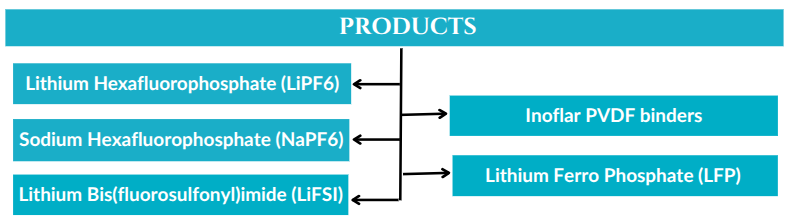

GFCL EV’s product portfolio includes:

Lithium Hexafluorophosphate (LiPF₆) – a core electrolyte salt for lithium-ion batteries

Sodium Hexafluorophosphate (NaPF₆) – catering to emerging sodium-ion battery technologies

Lithium Bis(fluorosulfonyl)imide (LiFSI)

PVDF / PTFE binders

These products require high-purity manufacturing, strict quality controls, and significant R&D. This creates very high entry barriers. The company’s connection with GFL’s fluorine chemistry ecosystem gives it an advantage that is hard to replicate.

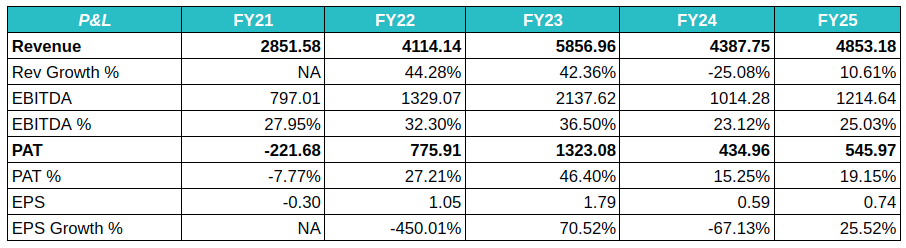

GFCL EV showed significant growth between FY21 and FY23. Revenues increased from ₹2,852 crore to ₹5,857 crore, driven by increased capacity and strong EV demand. EBITDA margins rose to about 25%, showing good operating leverage and pricing strength in a specialized market.

However, FY24 and FY25 saw a slowdown.

Revenue fell to ₹4,388 crore in FY24, then slightly increased to ₹4,853 crore in FY25.

EBITDA and PAT decreased due to lower capacity use, a drop in EV demand, and adjustments in inventory among customers.

Yet, profitability remains fundamentally strong:

PAT margins are around 19%.

There is positive cash flow at the operating level. There is no sign of major price drops or changes in competitive strength.

One of GFCL EV’s biggest strengths is its financial discipline.

Interest coverage stays above 5x, even during the economic slowdown.

Unlike many capital-heavy chemical and EV-related companies, GFCL EV has steered clear of heavy debt. This approach lets it handle short-term fluctuations without stressing its balance sheet.

Return metrics clearly show cyclicality.

ROE and ROCE peaked in FY23 at about 24% and 22% respectively.

These fell to around 7% in FY24 and FY25. This drop is mainly due to underuse of expanded capacities and normalizing margins.

This decline seems to be cyclical instead of structural. Asset productivity should improve once EV demand stabilizes and utilization rises.

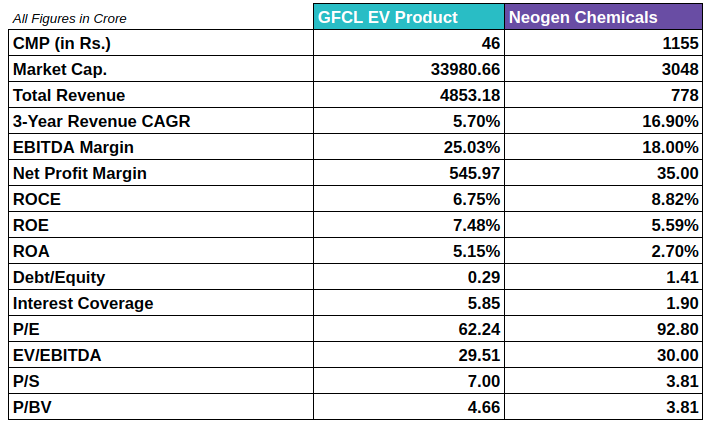

GFCL EV has no direct listed peer in India due to its almost exclusive focus on EV electrolyte chemistry.

Neogen Chemicals is often referenced as a peer, but it is a diversified specialty chemical company. Battery chemicals make up a small and still-growing part of its revenue.

GFCL EV operates on a much larger scale and has better EBITDA margins, at 25% compared to approximately 18%.

GFCL EV’s balance sheet is significantly stronger. It has lower debt and better interest coverage, which lowers financial risk.

The valuation premium for GFCL EV shows its focused EV exposure, scale, and high barriers to entry. In contrast, Neogen’s higher P/E ratio indicates growth potential rather than current profitability.

The long-term outlook for GFCL EV is supported by structural trends in the electric vehicle market:

India’s EV battery market is expected to grow at about 24-25% CAGR.

The EV electrolyte industry should see growth at around 12-13% CAGR.

GFCL EV is projected to grow at approximately 18-20% CAGR until FY30, showing a return to typical levels instead of projecting peak growth.

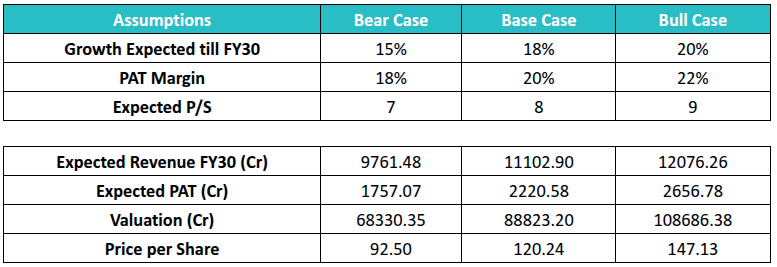

Assumptions:

PAT margins are expected to be around 18-22% in a typical cycle.

Valuations are based on price-to-sales multiples of about 7-9 times, considering operating leverage along with raw material price fluctuations and execution risks.

In these scenarios, GFCL EV presents a significant opportunity for long-term value creation as earnings stabilize.

Prolonged EV demand slowdown

Raw material price volatility

Slower-than-expected capacity utilization

Execution risks in scaling new chemistries

However, these risks are operational and cyclical; they are not driven by the balance sheet.

GFCL EV Products is a high-quality unlisted EV ecosystem business that is currently facing a temporary slowdown. This recent decline in performance comes from an industry-wide inventory correction, not from any problems in core operations or competitive strength.

With strong backing from its parent company, solid chemistry capabilities, sensible debt levels, and favorable long-term trends for electric vehicles and energy storage, GFCL EV Products seems well-prepared for earnings recovery and value growth as utilization returns to normal.

For long-term investors who recognize the cyclical nature of capital-intensive specialty chemical businesses, GFCL EV Products presents an attractive unlisted investment opportunity that fits with India’s shift toward electric mobility. Investors can find such opportunities on platforms like SharesCart, which specialize in curated unlisted investments.

Independent Research Powered By - Actionable data

Comprehensive Equity and Strategic Research Report...

February 2026

Motilal Oswal Home Finance: Best-in-Class Asset Qu...

February 2026