15 Days Price Change

Manika Bhalla

Manika Bhalla

Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills... Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills and a solid foundation in finance. Experienced in financial modeling and valuation, with a keen interest in equity research and investment analysis. Read more

Summary

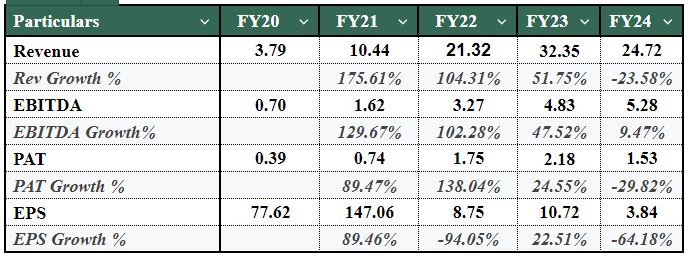

ZAK Venture grew rapidly between FY2020 and FY2023 through aggressive expansion in gas infrastructure projects, but this strategy exposed financial vulnerabilities. FY2024 marked a turning point with declining revenues, margin pressure, high working capital stress, and rising leverage. While execution capabilities and order book remain strong, future growth depends on deleveraging, cash flow discipline, and efficient use of existing assets.

The company, ZAK Venture Private Limited, focuses on the planning and development of city gas distributions (CGDs) within the energy infrastructure industry in India, as well as executing natural gas pipelines and laying out related infrastructure. ZAK will provide the necessary technical solutions for these types of projects by laying down Auto LPG systems, gas dispensers and offering technical assistance, etc. The majority of ZAK's work is dependent on project contracts; hence, ZAK's revenue is dependent on the awards of these contracts, their timely execution and the amount of money spent within the Indian oil and gas sector to support CGDs, etc.

ZAK Venturing is primarily active in the following sectors:

The company's business is project-driven; revenue comes from the contracts they obtain (in-bound orders), how long it takes to execute them, and their our customers (generally public sector undertakings) will pay for services rendered

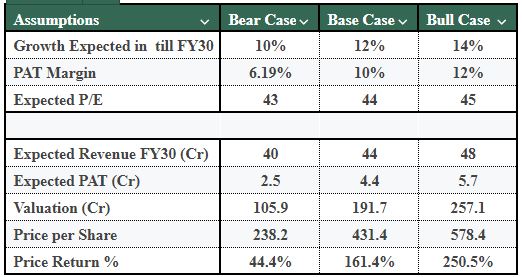

ASSUMPTIOMS

Based on these assumptions, ZAK Venture may be valued between approximately ₹106 crore to approximately ₹257 crore for FY2030, thus presenting investors with significant upside potential, provided that ZAK Venture can execute in an orderly manner and continues to improve its profitability through cost discipline. The projected values should be used only for illustrative purposes and viewed as potential outcomes of varying scenario's execution.

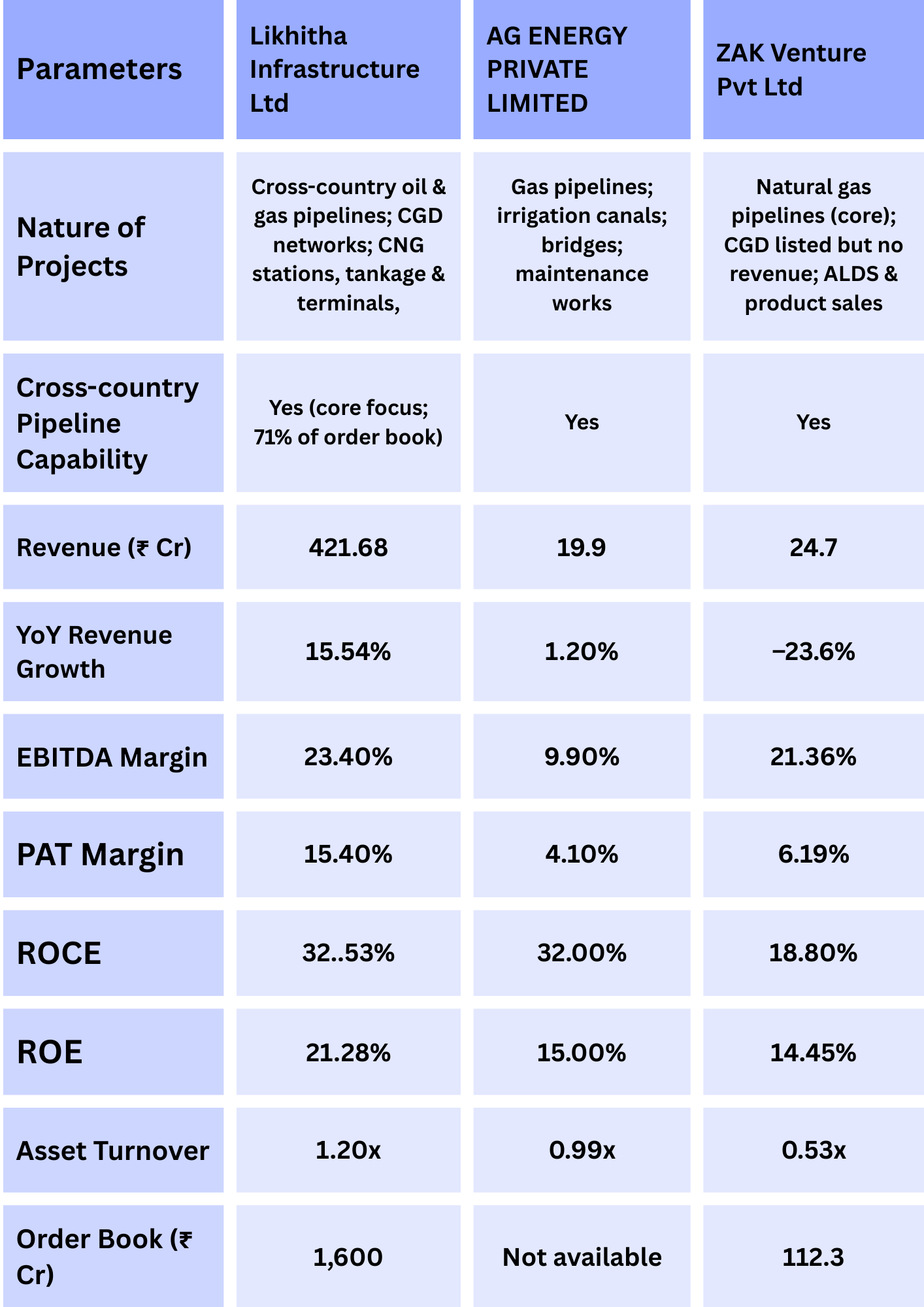

ZAK Venture Pvt Ltd's peer comparison with Likhitha Infrastructure Ltd and Aargee Pipeline Services Pvt Ltd highlights the fundamental differences in their business models even though all three companies are actively involved in providing pipeline infrastructure and oil and gas EPC services.

To summarise, Likhitha is the benchmark for scale, profitability, and strength in the industry. ZAK Venture is positioned in the middle; it has operational capabilities and will achieve significant growth in the future but has short-term financial and operational issues. Aargee continues to be a small and low-growth player with little visibility.

While there was a significant amount of both operational and financial stress placed upon ZAK Venture in FY 2024, the company has retained a number of potential growth levers which could help with recovery and stabilisation, provided that management executes with financial discipline and Improves working capital efficiency.

ZAK Ventures' core competency is laying gas pipelines for PSU & CGD clients. A revival in project execution, whether by way of reviving previously stalled contracts or by securing new orders can assist in the restoration of revenue momentum. Furthermore, the Government focus upon expanding India's Natural Gas Infrastructure & CGD Penetration represents a long-term structural opportunity for the business, although the timing and visibility of orders remain highly uncertain.

The fall of 75% in Product Sales experienced in FY 2024 appears to be an abnormal occurrence compared to prior performance. Should there be a return to stabilisation or recovery in Auto LPG, Dispensers or associated equipment, this represents the potential for incremental revenue streams and offsets for ZAK Ventures. In order for this to occur successfully, there needs to be increased visibility into the demand for these products along with a tightening of inventory planning in order to mitigate any increase working capital strain which may be experienced.

ZAK has a significantly expanded asset base. Should ZAK be able to grow revenue in the future there will be operating leverage generated by costs which will benefit margins. The areas of focus should be optimising Manpower Costs, Logistics Efficiencies and Overhead, all of which are essential in order to increase profitability without the need for any accompanying increases in capital investment.

The next immediate opportunity is to free up cash flow by reducing inventory levels or speeding up the collection of accounts receivable. By doing so, it will be possible to improve working capital by freeing up liquidity and reducing the need to borrow money in the short term, thereby also decreasing interest expense, which would support improving net profit.

The second near-term opportunity is if the Company changes its strategy from aggressive expansion to one based on consolidation. This would allow the Company to achieve financial stability by generating cash, rather than simply focusing on scaling its business. Successful de-leveraging and controlling capital will enhance the confidence of investors and increase the sustainability of their valuations over the next several years.

These variables cumulatively infer, and indicate that FY2024 is not merely an anomaly but rather a stress test for the company’s Growth strategy.

The company is in the process of moving from a period of hypergrowth to a period of recovery and stabilization, during which time it will rely more on execution quality, working capital discipline, and debt management than on the rapid expansion of its business. Going forward, any meaningful growth will rely on the company's ability to utilize its existing assets efficiently to generate revenues, rather than on the addition of new capacity.

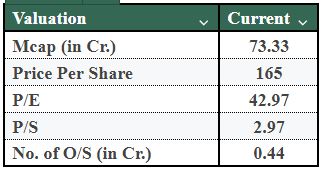

In conclusion, the financial history of ZAK Venture Private Limited illustrates the classic risks and rewards associated with pursuing an aggressive growth strategy. The company went through a period of rapid growth between FY2020 and FY2023, whereby its revenue base and asset base grew substantially, utilizing a combination of equity and debt to finance its expansion. FY2024 is a significant turning point for the company, with a decline in revenues, reduced profitability and increasing amounts of working capital stress. As such, the company's minimal product sales, growing amount of inventory and increasing reliance on short-term loans all illustrate that the company's operations are inefficient and that the company is facing a heightened liquidity risk. The shares of ZAK Venture Private Limited are available on SharesCart. Interested investors may contact their Relationship Manager (RM) for further details.

Independent Research Powered By - Actionable data