15 Days Price Change

Kashvi Dhamija

Kashvi Dhamija

CFA Level I pass and BBA graduate, with strong foundation in finance and analytical concep... CFA Level I pass and BBA graduate, with strong foundation in finance and analytical concepts. Read more

Zepto CCPS Series D Zepto CCPS Series II G

Summary

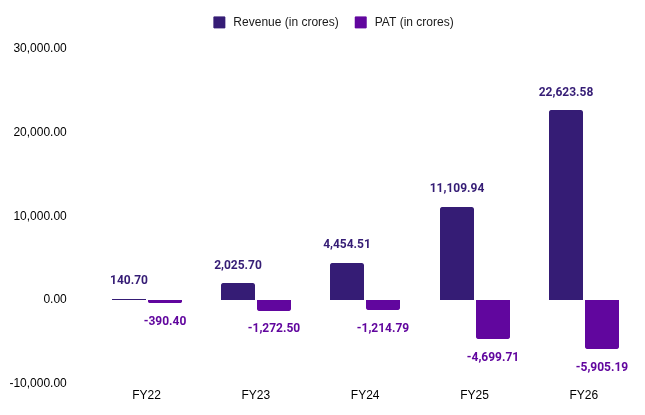

Quick commerce startup Zepto filed its Updated Draft Red Herring Prospectus (UDRHP) on 8th June, 2026, moving closer to what is expected to be one of the largest IPOs in FY27, with a target valuation of $1 billion. The offering includes a fresh issue of ₹8,010 crore alongside an OFS of 11.35 crore shares. While revenue doubled to ₹22,623 crore in FY26, net losses widened to ₹5,905 crore. At the current unlisted price of ₹40, the valuation scenarios imply listing prices ranging from ₹46 to ₹84. Regulatory proceedings and sustained losses remain key risks.

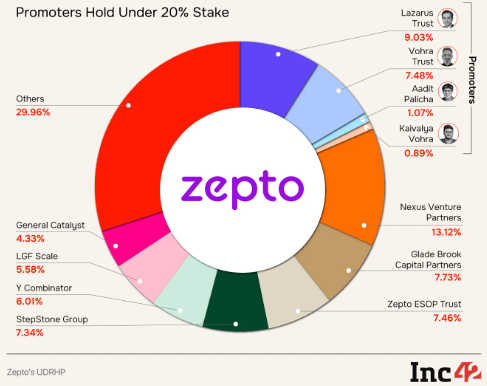

Founded in 2021 by Aadit Palicha and Kaivalya Vohra, Zepto built itself into one of India's top three quick commerce players in just four years. The company has raised over $2.4 billion from names like Glade Brook Capital, General Catalyst, Y Combinator, and Nexus Venture Partners.

The current shareholding pattern is as follows:

Source: https://inc42.com/buzz/zepto-drhp-a-look-at-shareholding-pattern-key-executives/

The company competes directly with Blinkit, Swiggy Instamart, and now BigBasket, Flipkart Minutes, and Amazon Now. The quick commerce market itself is projected to hit $40 billion by 2030, so the runway is massive.

The IPO comprises a fresh issue of shares worth ₹8,010 crore along with an offer for sale (OFS) component of up to 11.35 crore equity shares. On the OFS side, Nexus Venture Partners plans to offload 8.78 crore shares, Razor Capital is looking to sell 93.64 lakh shares, and Contrary aims to exit 78.01 lakh shares. Notably, the promoters are not participating in the OFS, meaning they will retain their stake until the lock-in expiry post listing. The shares are proposed to be listed on both NSE and BSE.

The funds will be used for expansion of dark store network (Zepto plans to open approximately 1,904 new dark stores), lease rentals for existing dark stores, technology and cloud infrastructure, marketing and business promotion, inorganic growth and general corporate purposes.

Revenue more than doubled to ₹22,623.6 crore in FY26 from ₹11,109.9 crore in FY25, a strong indicator of Zepto's scale trajectory. However, net losses also widened 26% to ₹5,905.2 crore in FY26.

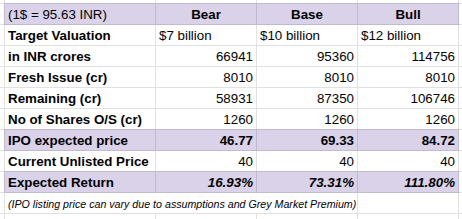

With approximately 1,260 crore shares outstanding, the valuation math works as follows. The fresh issue of ₹8,010 crore represents new capital being added to the business. To estimate the implied market value of existing shares, that amount is subtracted from the total target valuation, and the remainder is divided by the number of shares.

Bear Case: Anchored to Zepto's last funding round valuation of roughly $7 billion, the implied price comes to approximately ₹46.77 per share, a modest 16.9% premium.

Base Case: Using Zepto's own stated target valuation of $10 billion, the implied listing price works out to ₹69.33 per share, representing a 73.3% return. This scenario assumes Zepto successfully commands a valuation in line with its internal expectations at the time of listing.

Bull Case: Assuming a $12 billion valuation, this case yields an implied price of ₹84.72 and a potential return of 111.8%. This scenario is slightly optimistic and prices in a degree of post-listing momentum and market optimism.

The DRHP also outlines several regulatory and legal risks. These include an Enforcement Directorate (ED) summons issued to the founders, consumer protection complaints, labour-related matters, and food safety compliance issues across certain locations. While such disclosures are not uncommon for large startups preparing to go public, investors tend to monitor these developments closely.

Zepto is looking to enter the public markets carrying a history of substantial losses with no near-term path to profitability clearly defined.

Structurally, the business is dependent on three fragile pillars - dark store network, large and loyal user base, and technological infrastructure - all of which must remain operationally sound at all times.

Zepto operates in an industry characterised by low entry barriers with established players like BlinkIt and Instamart and new players like Flipkart Minutes and Amazon Now, with significant financial backing, all competing to find their footing with the customers.

At the current unlisted price of ₹40, Zepto appears fairly priced relative to the bear scenario but leaves meaningful upside on the table in base and bull cases. For risk-tolerant investors with a view on India's quick commerce opportunity, the base case return of ~73% offers a reasonable risk-reward. However, accumulating losses, pending regulatory proceedings and profitable competitors could drive the valuation down. The opportunity is real, and so are the risks.

Independent Research Powered By - Actionable data