15 Days Price Change

Nikhil Singh

Nikhil Singh

I am a versatile professional known for my expertise as a technical analyst, insightful co... I am a versatile professional known for my expertise as a technical analyst, insightful contributions as a part-time investor, and creative talents as a content writer. With a strong background in finance, I seamlessly combine technical know-how and fundamental analysis in my role as a part-time investor. Read more

Summary

The article analyzes Garuda Aerospace, an Indian drone company (backed by MS Dhoni), focusing on its upcoming IPO, business model, financials, growth potential, and risks. It is essentially an investment research report for people considering buying its unlisted shares before IPO.

Garuda Aerospace, a Chennai-based drone manufacturer backed by MS Dhoni, is India's most-watched pre-IPO drone investment with shares not listed publicly at ₹485 each on Sharescart and an implied total value of around ₹2,500 crore.

Garuda has transitioned from purely agricultural applications and now produces drones for various sectors, such as the defence through partnerships with technologists and the government; logistics companies; disaster recovery; infrastructure inspection; pre-celebration inspections, etc supported by global technology partners. The company pre-filed a confidential Draft Red Herring Prospectus with SEBI in early April 2026 for a ₹1,000 crore IPO and is targeting a post-listing valuation of ₹4,000–5,000 crore. That ambition rests on a fast-growing topline which is ₹118–123 crore in FY25, four straight years of reported profitability, and a 25%+ share of all drones flying in Indian airspace. Yet behind the aviator-like ascent sit real questions on margin compression, ballooning receivables, negative operating cash flow, and a rich valuation against listed peers like ideaForge and Zen Technologies. This report unpacks the investment case, business model, financials, peer set, and risks for investors evaluating Garuda Aerospace shares in the unlisted market.

Garuda Aerospace Private Limited was founded by Agnishwar Jayaprakash (founder, vice-principal at Harvard), and co-founder Rithika Mohan, in Chennai on October 6 of 2015. The company will convert into a public limited company — Garuda Aerospace Limited — by the end of 2026. Registered office address: Agni Business Centre, K.B. Dasan Road, Alwarpet, Chennai.

The story of how the company was founded may seem unbelievable at first but actually has some truth to it. Agnishwar (a competitive swimmer who won multiple gold medals at Asian Games) first began working with drone technology for entertainment-based applications; for instance, using drones to shower contestants with gifts during reality shows and to light up wedding ceremonies.

The company was on the verge of closing its doors in January of 2020 but was able to pivot after creating a drone for sanitizing buildings for state government during the COVID-19 pandemic. Shortly after that, Agnishwar received a seed of $1 million from an overseas investor (Silver Swan Investments) after Elon Musk responded to one of his tweets. As a result of continuing to grow while being on the verge of bankruptcy, Garuda's market capitalization has reached ₹2,000 crores by the end of 2025.

As of April of 2026, Garuda is reporting:

- More than 400 currently in operation by DGCA-certified pilot across 84+ cities in India

- The current customer base is more than 750 businesses including companies like Tata, Reliance, Adani, Godrej, Swiggy, Flipkart, L&T, IFFCO, NTPC, NHAI, ISRO, HAL, and DRDO.

- The company has been granted 20+ patents and attained the ISO 9001/AS9100 quality certifications for its aerospace historical manufacturing processes.

- The first drone manufacturing company in the country that has both obtained DGCA Type Approval (for its aircraft) and been approved as an organisation to operate a DGCA-certificated Remote Pilot Training Institute.

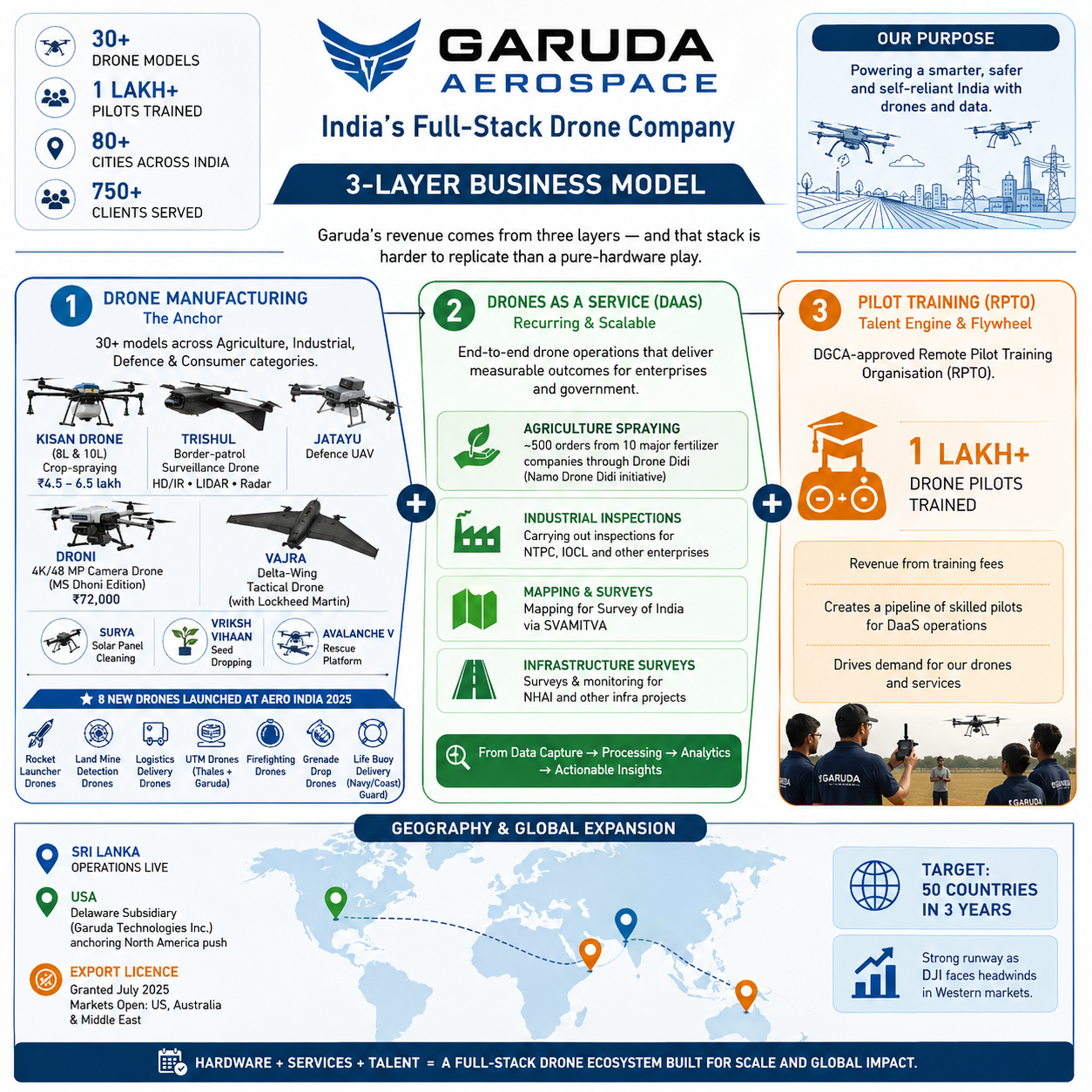

Garuda's revenue comes from three layers — and that stack is harder to replicate than a pure-hardware play.

Drone manufacturing is the anchor. The company sells 30+ models across agriculture, industrial, and defence.

Key products:

Garuda introduced eight brand-new drones at Aero India 2025 (February). They included rocket launcher drones, as well as drones for detecting land mines; drones for delivering logistics; UTM (unmanned traffic management) drones developed through a collaboration between Thales and Garuda; drones for firefighting; drones for dropping grenades; and drones for providing life buoys to the Navy or Coast Guard.

Drones as a service (DaaS) is the second source of revenue, which includes contracts with major fertilizer companies to conduct agricultural pesticide applications (~500 orders from 10 companies through Drone Didi); carrying out industrial inspections on behalf of NTPC and IOCL; mapping for the Survey of India via SVAMITVA; and undertaking infrastructure surveys for NHAI.

Pilot training is the third. Through its DGCA-approved RPTO, Garuda claims to have trained over 1 lakh drone pilots, which generates fees and pulls through downstream hardware and service business.

On geography: Garuda has started internationalising. Sri Lanka operations are live; a Delaware subsidiary (Garuda Technologies Inc.) anchors the North American push; and an export licence granted in July 2025 opened the US, Australia, and the Middle East. Management's stated target is 50 countries in three years — ambitious, but there's a real runway with DJI facing headwinds in Western markets.

The Indian drone market size estimates range absurdly wide — USD 654 million (MarketsandMarkets) to ₹2.5 trillion by 2030 (EY-FICCI). A reasonable middle ground: USD 1.58 billion in 2024, growing at roughly 20–22% annually. Within that, agriculture drones grow at ~28% CAGR and military drones at ~18%.

Policy has been genuinely useful here, not just in press releases:

The competitive picture is trickier. ideaForge Technology still holds roughly 50% of India's UAV market, though its FY25 revenue collapsed 49% (election-year procurement delays) and it swung to a ₹62 crore loss — a preview of the government-revenue lumpiness risk. Zen Technologies dominates anti-drone systems and simulators. Paras Defence is building counter-drone capability with a €2.2 million LOI from Cerbair and a ₹142 crore DRDO laser contract. Asteria Aerospace (74% owned by Reliance Jio) grew FY25 revenue 90% to ₹79 crore. Marut Drones raised $6.2 million in October 2024 targeting the same agri segment.

Garuda's defensible edge is the DaaS-plus-training combination. Hardware-only competitors can't easily replicate 500 certified pilots and 1 lakh trained operators. That said, Reliance's financial backing of Asteria is a legitimate threat that deserves respect, not dismissal.

Agnishwar Jayaprakash is the Founder and CEO and the main public face of the company. He comes from the Agni Group family and has a background in business law and management. He has worked on education initiatives across thousands of schools and has received recognitions like Fortune India 40 Under 40. His strong visibility helps the brand but also brings leadership concentration risk.

Rithika Mohan is the co founder and became Whole time Director in November 2025. She focuses on agritech and innovation.

The core management team includes Sanal Kumar as CFO and mentor, Shyam Kumar as COO, Dhayabaran Davarajan handling operations, and Raj Bhatia leading business development.

Vishnu Jayaprakash is a Non Executive Director with an engineering background. He is related to the founder which is important from a governance point of view.

To strengthen governance the company added independent directors between November 2025 and March 2026:

MS Dhoni joined as investor and brand ambassador in 2022. He invested around ₹10 crore and later added ₹4 crore in 2024. At IPO levels his stake could see a strong return. The company also named its consumer drone product after him. His presence helps build trust and visibility especially in tier 2 markets.

Total funding: $37–50 million across nine institutional rounds and 173 angel cheques (estimates vary by source).

| Round | Date | Amount | Lead Investor | Valuation |

|---|---|---|---|---|

| Seed | 2020 | $1M | Silver Swan Investments | — |

| Series A | Feb 2023 | $22M (~₹183 Cr) | SphitiCap ($12M), Ocgrow | — |

| Bridge | Oct 2023 | ₹25 Cr | Venture Catalysts, We Founder Circle | — |

| Series B | Apr 2025 | ₹100 Cr | Venture Catalysts (VCAT) | ~$250M (₹2,100 Cr) |

| Series B-II | Jun 2025 | $1M | We Founder Circle | — |

| Series B Extension | Aug 2025 | $1M (₹8.73 Cr) | Narotam Sekhsaria Family Office | $260M |

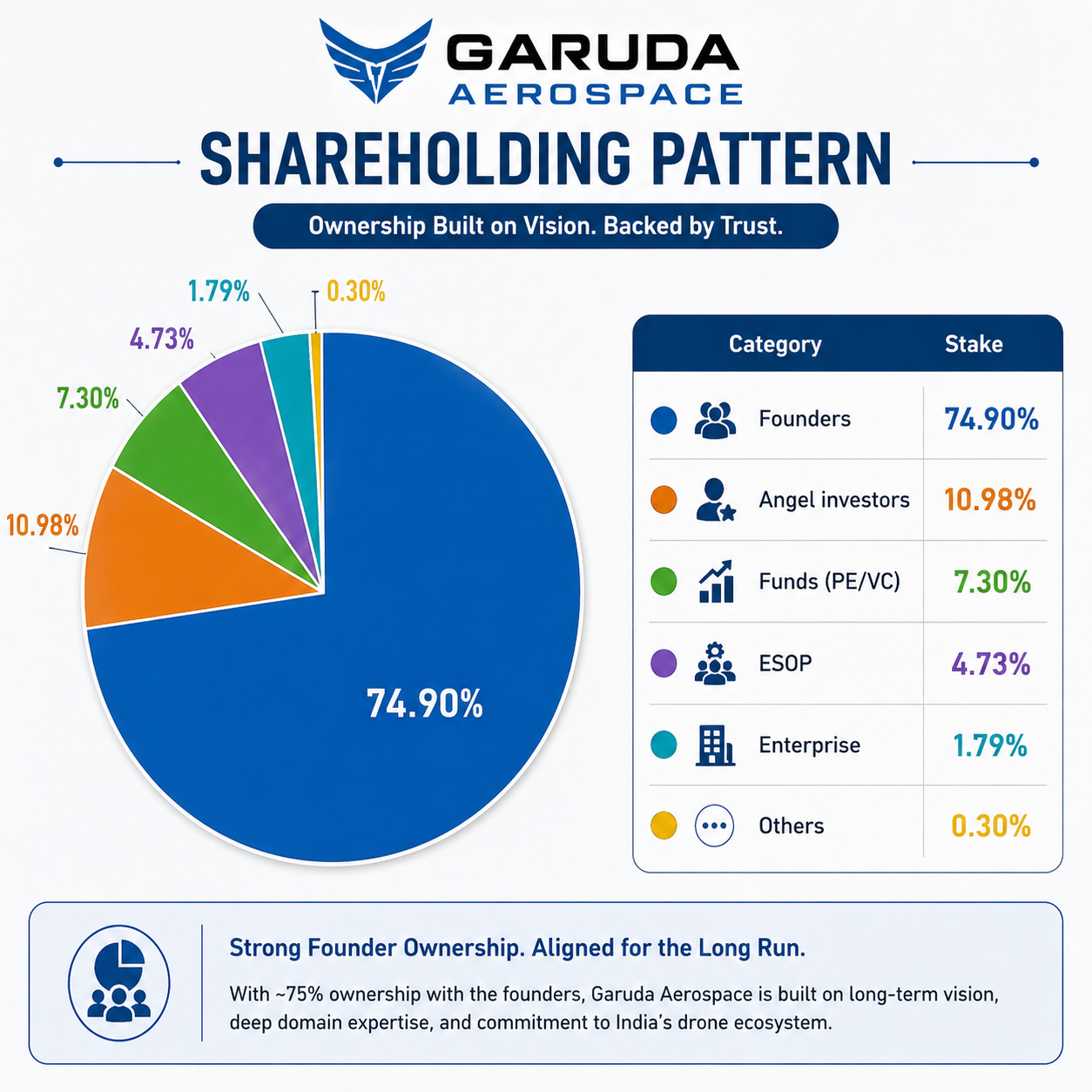

Total outstanding shares: 5.21 crore post the 1:5 stock split (face value ₹10 → ₹2) and a 7:1 bonus issue completed before the DRHP filing.

Founders retain 74.9%. That's a positive for alignment and a mild concern for minority investor influence worth being clear-eyed about.

P&L Statement

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Revenue | 47 | 110 | 117.7 |

| Cost of Material Consumed | 10.8 | 50 | 72.5 |

| Change in Inventory | -1.3 | -1.2 | -16.6 |

| Gross Margins | 79.79 | 55.64 | 52.51 |

| Employee Benefit Expenses | 8.6 | 10.6 | 9.6 |

| Other Expenses | 18 | 26 | 31.2 |

| EBITDA | 10.9 | 24.6 | 21 |

| OPM (%) | 23.19 | 22.36 | 17.84 |

| Other Income | 0 | 0.8 | 7.1 |

| Finance Cost | 0.9 | 1.92 | 1.2 |

| D&A | 1.5 | 1.98 | 3.1 |

| EBIT | 9.4 | 22.62 | 17.9 |

| EBIT Margins (%) | 20 | 20.56 | 15.21 |

| PBT | 8.4 | 21.3 | 23.9 |

| PBT Margins (%) | 17.87 | 19.36 | 20.31 |

| Tax | 2.2 | 5.5 | 6.6 |

| PAT | 6.2 | 15.8 | 17.3 |

| NPM (%) | 13.19 | 14.36 | 14.7 |

| EPS | 579.44 | 1436.36 | 1572.73 |

Financial Ratios

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Operating Profit Margin (%) | 23.19 | 22.36 | 17.84 |

| Net Profit Margin (%) | 13.19 | 14.36 | 14.7 |

| EPS (Diluted) | 579.44 | 1436.36 | 1572.73 |

Assets

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Fixed Assets | 6.8 | 13.7 | 15.3 |

| CWIP | 0 | 0 | 3.5 |

| Investments | 0 | 0 | 0.5 |

| Trade Receivables | 37.7 | 73.8 | 114.8 |

| Inventory | 1.35 | 26 | 24.6 |

| Other Assets | 11.15 | 35.5 | 52.8 |

| Total Assets | 57 | 149 | 211.5 |

Liabilities

| Metric | 2023 | 2024 | 2025 |

|---|---|---|---|

| Share Capital | 0.107 | 0.11 | 0.11 |

| FV | 10 | 10 | 10 |

| Reserves | 29.8 | 100.5 | 168 |

| Borrowings | 14.7 | 19.7 | 6.7 |

| Trade Payables | 1.6 | 15.7 | 25.8 |

| Other Liabilities | 10.79 | 8.79 | 10.39 |

| Total Liabilities | 57 | 149 | 211 |

The balance sheet is largely debt-free. That's good. The receivables picture is not: ₹114.8 crore outstanding against ₹120 crore of annual revenue means the company is essentially pre-financing its government and PSU customers for a full year. That is a structural working-capital problem, not a timing blip.

| Company | FY25 Revenue (₹ Cr) |

FY25 PAT (₹ Cr) |

Market Cap (₹ Cr) |

Segment |

|---|---|---|---|---|

| Garuda Aerospace | 118–123 | 17.5–18.4 | ~2,500 (unlisted) | Agri, industrial, defence |

| ideaForge Technology | 161-182 | -62 (FY25 loss) | ~2,366 | Defence-heavy |

| Zen Technologies | 974 | Strong | 15,923 | Anti-drone, simulators |

| Paras Defence | 365 | ~17 (Q3) | 5,800 | Counter-drone, optronics |

| DroneAcharya (BSE SME) | 36.7 | -13.4 | 74 | Training (SEBI fraud action) |

| Asteria Aerospace (unlisted) | 79 (+90% YoY) | — | — | Agri, industrial |

ideaForge's FY25 implosion is the most instructive comp. A company with 50% market share and real defence contracts still saw revenue fall nearly in half because government procurement paused during election year. Garuda's government revenue concentration creates the same exposure — arguably worse, since Garuda is smaller and has less financial cushion.

Why the bull case is real:

Why the bear case is also real:

Mitigants:

Garuda Aerospace is not just a concept story. It is a working business with real customers patents and partnerships with Airbus and Lockheed Martin. The founder has also rebuilt the company more than once which adds some credibility. This is not something you see in every pre IPO company.

But the current price already reflects a lot of this. At around ₹485 in the unlisted market most of the positive story is already priced in. At roughly 20 times FY25 revenue and about 140 times earnings you are not buying based on current numbers. You are paying for what the company might do in FY26 and FY27. The execution gap is important here. FY26 revenue is around ₹41 crore. To meet guidance the second half needs to deliver something like ₹120 to ₹170 crore. Yes government contracts usually come in the second half but this level of back loading is still something to be careful about.

Two things can really change the situation - if FY26 revenue actually reaches around ₹200 crore and if receivables start converting into real cash. Right now receivables are about ₹115 crore while cash in the bank is only around ₹4.6 crore.

That gap is not small. It is probably the biggest operational risk before IPO. On the positive side the DaaS plus training model looks strong and still not fully valued. The export licence timing also helps the company expand faster. And defence spending is likely to stay strong for years not just short term.

So the question is not whether Garuda is a good company. It likely is. The real question is whether ₹485 is a comfortable entry price given the risks. There is also a lock in after listing and the IPO itself has already been delayed twice. If someone believes the FY26 numbers will be achieved and is ready to hold through ups and downs then there is a chance of getting listing gains. But if someone is looking for a quick trade then the margin of safety is quite limited. In this case it makes more sense to track receivables closely even more than revenue.

Independent Research Powered By - Actionable data