15 Days Price Change

Manika Bhalla

Manika Bhalla

Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills... Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills and a solid foundation in finance. Experienced in financial modeling and valuation, with a keen interest in equity research and investment analysis. Read more

Summary

A complete deep dive into Indofil Industries Limited — 60 years of chemistry, a near-debt-free balance sheet, and a ₹4,507 Cr investment bet that peers cannot match. Trading at 7x earnings and below book value, the case is straightforward: strong business, wrong price, and right direction.

Indofil Industries Limited is a Mumbai-based chemical industry, having more than 60 years of experience. It comes under K.K. Modi Group, the well-known group of the world. The company is run by Dr. Bina Modi, Chairperson & Managing Director, with two types of chemicals. They are crop protection products, used by farmers, and speciality chemicals which include construction, textile, plastics, and leather industries.

It is a huge multinational company that is present in more than 120 countries worldwide, and also it is considered as the second largest exporter of fungicides in India. Its income for FY2024-25 was ₹3,419 Crore and the Profit before Tax was ₹518 Crore, witnessing an increase of 43 percent over the last year. This growth is because of active research and development, patenting of products, investing backward integration in raw materials, and focusing on environment-friendly and bio-products. All of its Gujarat-based plants are following global quality standards. The company is aiming to achieve the enterprise value of 2 billion dollars within few years.

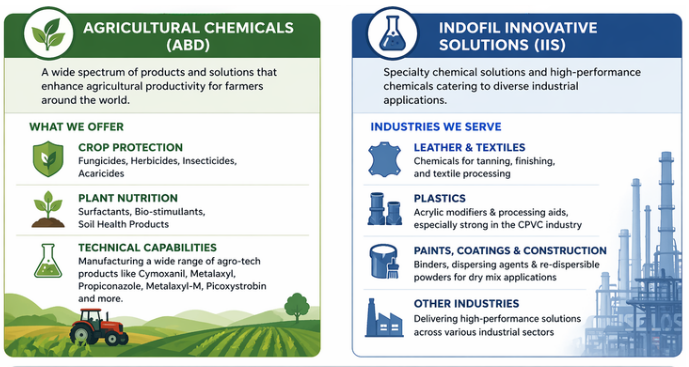

A broad range of products that contribute to increasing agricultural efficiency worldwide. This group covers Crop Protection (Fungicides, Herbicides, Insecticides, Acaricides), Plant Nutrition (Surfactants, Bio-stimulants, Soil Conditioners), and Technical Competence, which is responsible for producing agro-chemical actives such as Cymoxanil, Metalaxyl, Propiconazole, Metalaxyl-M, and Picoxystrobin.

Chemical products for various industrial sectors. This division caters to Leather & Textile (tanning, finishing, treatment), Plastics (acrylic plasticizers and processing aids – with expertise in CPVC), Paints, Coatings & Construction

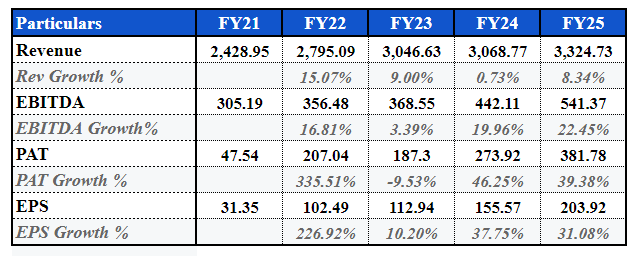

The table below shows the complete journey from FY21 to FY25. Interpret the data along with the context; every year had a unique factor influencing it and is not shown by just looking at the numbers.

Every year in this journey has its own unique factor. Below is the actual story behind each year's performance:

Worst performing year for Indofil in recent times. The total revenue for the company was ₹2,428.95 Cr, but it suffered from an extraordinary loss of ₹149.54 Cr, which led to very poor bottom-line performance and PAT being a mere ₹47 Cr even though the operations were decent enough. The impact of the COVID-19 pandemic was felt, as it affected the entire supply chain and stressed the incomes of farmers, making it very difficult for the company. However, the best thing that happened was none of the manufacturing plants closed.

The company’s revenues surged to ₹2,795 Cr (+15%), and its PAT seemed to have jumped to ₹207 Cr. However, this was mainly because the company did not face any exceptionals of ₹149.54 Cr as it had done in FY21. The noteworthy aspect was working capital management, which involved creating a sizable inventory buffer of ₹641 Cr, mostly financed through trade payables of ₹812 Cr, essentially utilizing supplier financing. This caused the operating cash flows to fall by 48%, reflecting a strategic choice of prioritizing supply chain management over cash flows. The notable growth figures for segments were India Agrochemical (10.53%) and Outside India Agrochemical (3.95%).

The company’s revenues reached a new high at ₹3,046 Cr. However, this growth was primarily attributed to pricing in a disrupted environment rather than volume growth. The PAT declined to ₹187 Cr due to an exceptional charge of ₹10.32 Cr and margin challenges. The trade payables were reduced drastically from ₹812 Cr to ₹412 Cr to ensure diversity in the supply chain rather than focusing on credit terms. An encouraging note was that the joint venture profit increased 4X to ₹59 Cr.

The revenue was flat, registering ₹3,068 Cr (+0.73%), but the profitability was excellent with EBITDA growth of around 20% and PAT increase of 46%, coming in at ₹274 Cr. Inventory optimization helped improve cash flow, as investments increased to ₹2,083 Cr. Domestic agro experienced a small fall, but the export business saw an increase of 7%, becoming the major factor behind the top-line performance. It turned out that FY2024 was the year when Indofil proved their operating leverage – margin improvement could be achieved without any growth in revenues.

Growth continued with the top-line rising 9.6% to ₹3,419 Cr, whereas PBT increased by around 43%. The most important event in this period was the 116% increase in investments to ₹4,507 Cr; it was the effect of international expansion and shifting towards investment-driven approach. Core businesses showed good results with India Agro growing 9%, exports by 7.7%, and support from the IIS segment. EBITDA increased by 22.45% and PAT grew by 39.38%. Deferred tax increased due to Dahej capex.

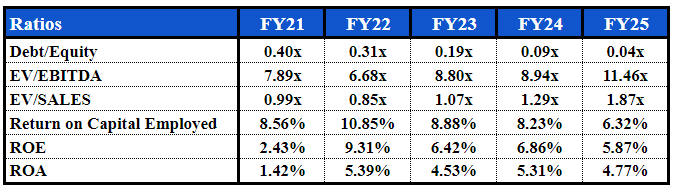

The ratio trajectory paints a very interesting story of an entity that has practically zeroed on its debts while at the same time moving into a capital deployment super cycle. The sacrifice is lower return ratios; however, it is a transient process and not necessarily a structural weakening.

The ratios for Indofil demonstrate a stronger balance sheet position where there is practically zero debt (D/E 0.04x) and valuation improvements (EV/EBITDA 11.46x). However, lower ROCE, ROE, and ROA suggest that the company is going through a capital deployment phase where the investments have not delivered full benefits yet. The trend in D/E ratios dropping from 0.40x in FY21 to 0.04x in FY25 suggests a five-year de-leveraging strategy. There is also a re-rating of the entity by the market since the profitability ratios have significantly improved.

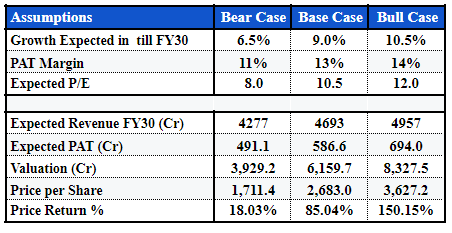

The valuation is based on comparison against agro chemical peers, adjusted with an appropriate discount due to Indofil’s unlisted parentage and lack of recognition in IIS. Base case (10.5x) is justified, in line with the peer band, citing Rallis India and adjusted lower than Dhanuka Agritech. Bear case (8.0x) has assumed weak cycle and commoditisation, while the bull case (12.0x) has assumed partial re-rating in IIS segment scaling below PI Industries’.

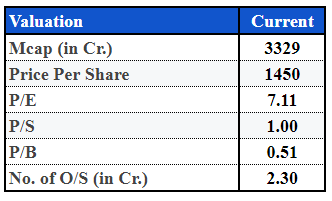

The P/B multiple of 0.51x is one of the standout facts in the report. Indofil is trading at 51% of its book value, reflecting strong skepticism about the profitability of the assets. Contrary to what many might think, the report explicitly states that the reason for such a discount is the company's unlisted parentage, lack of recognition as an IIS segment, and low return ratios due to higher reinvestment ratios. In FY25, the PAT grew by 39% while EBITDA increased by 22%.

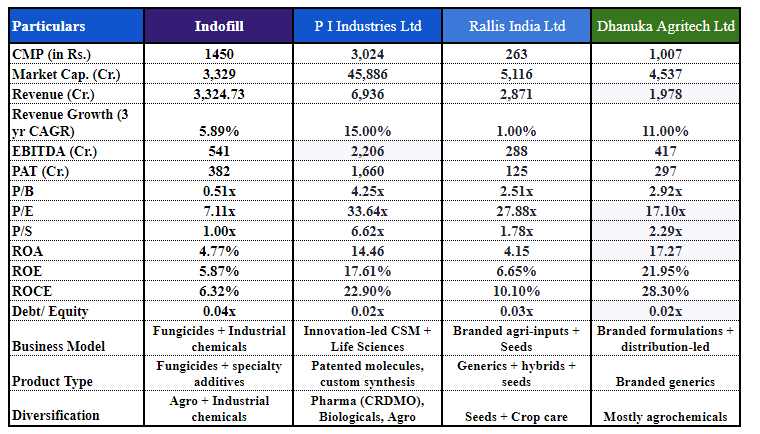

All four – Indofil, PI Industries, Rallis India, and Dhanuka Agritech - are engaged in production or distribution of pesticides in the agrochemical segment of India. All of them sell agrochemicals to Indian farmers as their ultimate consumers and face identical macro risks, such as dependence on monsoons, volatile costs of raw materials, global logistics costs, and changes in pesticide regulations. Thus, all of them make perfect benchmarks regardless of their size and business models.

In its concluding remarks concerning its peer analysis, the report is unequivocal. Indofil represents a bigger, more diversified and fundamentally stronger business compared to what its market value suggests in comparison with its peers. Its weak return ratios reflect only its current phase of aggressive capital allocation, rather than inefficiency. Indofil is the most undervalued among peers by any valuation criteria; it is profitable absolutely and has strong EBITDA results; it has no debt on its balance sheet and is expanding its capacity much faster than its peers of similar size. The only area where Indofil lags behind other companies is its revenue growth, but with its new capacity being put in place and opening up new markets abroad, there is nothing preventing Indofil from

Assumption 1 – Revenue Growth: The company’s revenue growth would be driven by a weighted average growth rate of its two business segments – agrochemicals (industry CAGR of 7–8%) and the high-growth IIS specialty chemicals segment (12–13%). Base Case (9.0%): Both segments growing at industry growth rates on the back of good capacity utilisation and gradual improvement in China+1 export volumes. Bear Case (6.5%): Agrochemicals cyclical in nature with weak monsoons, pricing pressures from China, and reduced export growth; IIS not able to completely mitigate the downside. Bull Case (10.5%): Strong traction in fungicide technical exports under China+1 and rapid ramp-up of IIS capacities.

Assumption 2 – PAT Margin: Indofil’s PAT margin is evaluated against comparable peers in the agrochemical industry such as Dhanuka Agritech (PAT margin of 14–15%) and Rallis India (10–11%). Base Case (13%): Steady mid-level peer positioning with good backward integration and gradual increase in IIS contribution. Bear Case (11%): Margins pressured by volatile raw material prices and low IIS realizations, taking them closer to agro peers.The bull case (14%) sees greater scale-up potential of the IIS business, along with better export realisations leading to leverage and margin expansion, but to the top end of the peer group (though not as good as pure specialty chemicals).

Valuation approach: The base-case P/E multiple of 10.5x is in line with the agro peer group, citing Rallis India and being lower than Dhanuka Agritech. The bear-case scenario of 8.0x considers a weak cyclical environment and commoditized status. The bull-case scenario of 12.0x represents a partial revaluation, lower than PI Industries.

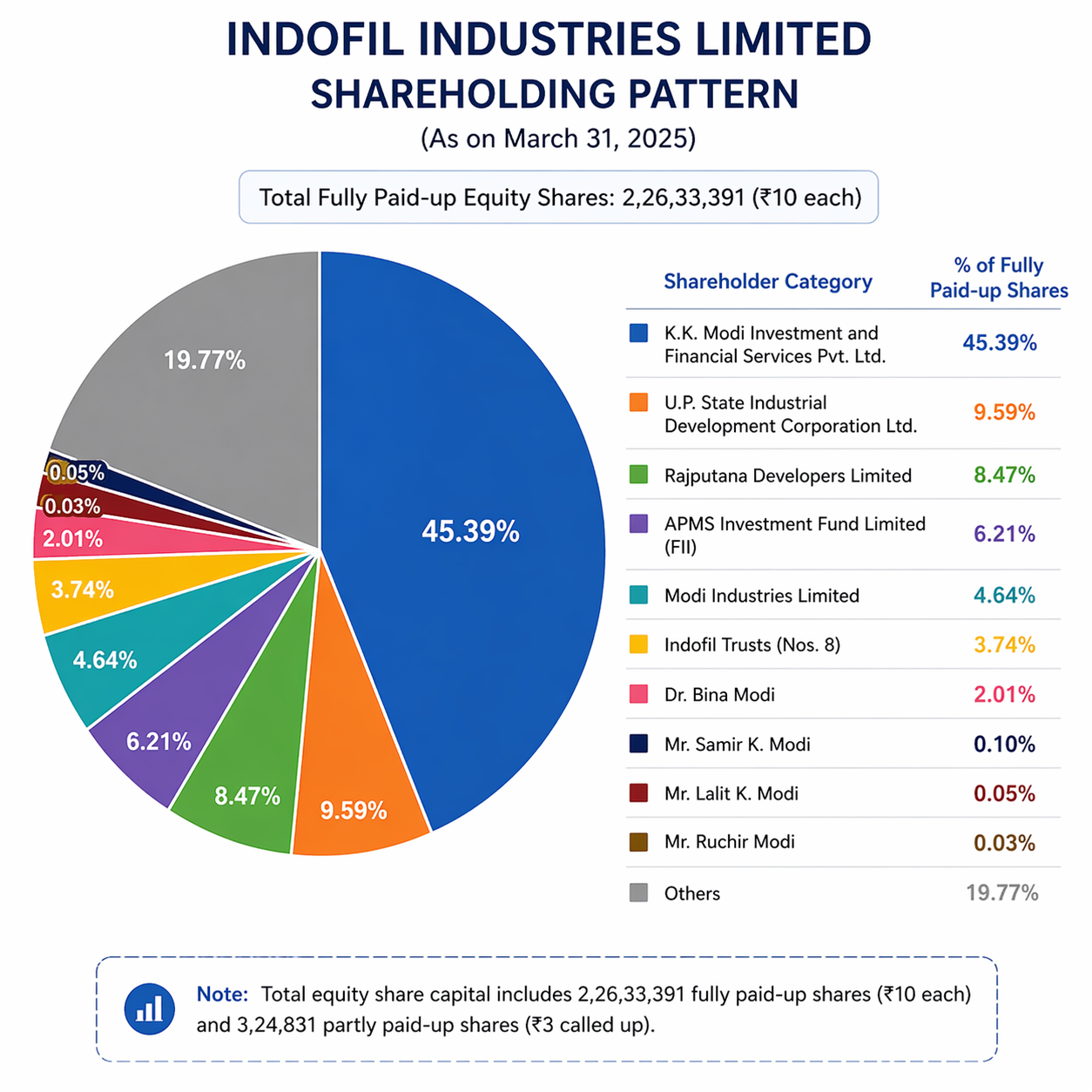

This structure of holding clearly shows that K.K. Modi Group companies dominate the holding structure of the firm. Promoter-owned structure, with large holding by promoters and related parties, is what defines this structure. Only one FII, that is, APMS Investment Fund Limited can be considered an important investor among FIIs.

K.K. Modi Group Companies jointly hold the major shares of the company. A very concentrated promoter base indicates founder-aligned management, with the fact that a ₹4,507 Cr investment in the Dahej capacity being promoter-backed. "Others," including Public & Retail Investors along with one FII investment from APMS, accounting for 6.21% equity shareholdings, form the small free float. Lack of institutional investors makes it clear why the stock is trading at a huge discount to its true worth.

Healthy Business. Incorrect Pricing. Correct Strategy.

Indofil is a highly profitable, debt-light company trading at just 7x profit and below book value – a valuation that none of its peers has enjoyed for decades, with Dhanuka trading at 17x and PI Industries at 34x. This pricing discrepancy isn’t due to negative financials, as PAT grew by 39%, while EBITDA increased by 22% during FY25. The only area of concern is the CAGR of revenue for three years, which was 5.89%. However, the commissioning of IIS specialty chemicals in April 2026 and the China+1 export thrust should be enough to remedy the situation in the coming two years.

Over the five-year period, Indofil has achieved: reduced leverage substantially (0.40x → 0.04x D/E ratio), PAT from ₹48 Cr to ₹382 Cr (8x), EBITDA margins have been expanded from 12.6% to 16.3%, and committed around ₹4,507 Cr to propel the next growth cycle. Our base case target price of ₹2,683 indicates an 85% return on CMP by FY30. While our bull-case scenario at ₹3,627 implies a 150% return on CMP by FY30. This share is available with Sharescart.

Independent Research Powered By - Actionable data