15 Days Price Change

URVASHI TOTLA

URVASHI TOTLA

MBA post graduate and CFA Level II cleared, with NISM certifications in Series VIII and XV... MBA post graduate and CFA Level II cleared, with NISM certifications in Series VIII and XV. Skilled in Financial Modeling, Valuation, and Portfolio analysis, with a strong interest in equity research and investment strategies. Read more

Summary

Fino PayTech is a financial inclusion–focused fintech platform that has evolved into a profitable, scalable business driven by its stake in Fino Payments Bank (contributing ~99% revenue). With ~21% revenue CAGR, improving margins, and a strong shift toward digital and CASA-led revenues, the company has undergone a structural turnaround and now operates with better efficiency and stability.

Despite risks like regulatory constraints and margin pressure in core segments, strong growth drivers such as digital scaling, rural distribution, and potential reverse merger position it well for the future. Available on Sharescart as an unlisted opportunity, Fino PayTech offers a compelling long-term play in India’s growing fintech ecosystem.

Fino Paytech was incorporated on July 13, 2006, India had hundreds of millions of people without access to formal banking services. The solution most companies chose was to wait — for incomes to rise, for smartphones to proliferate, for the cities to expand far enough that a branch made economic sense. Fino made the opposite choice entirely.

Instead of waiting, the company set out to build the technology infrastructure that could carry banking into India's most economically remote corners. Its first products were not consumer-facing at all. They were biometric smart cards and enrollment platforms sold to banks, microfinance institutions, and government bodies — picks-and-shovels tools for an industry that was only beginning to understand what financial inclusion at scale would require.

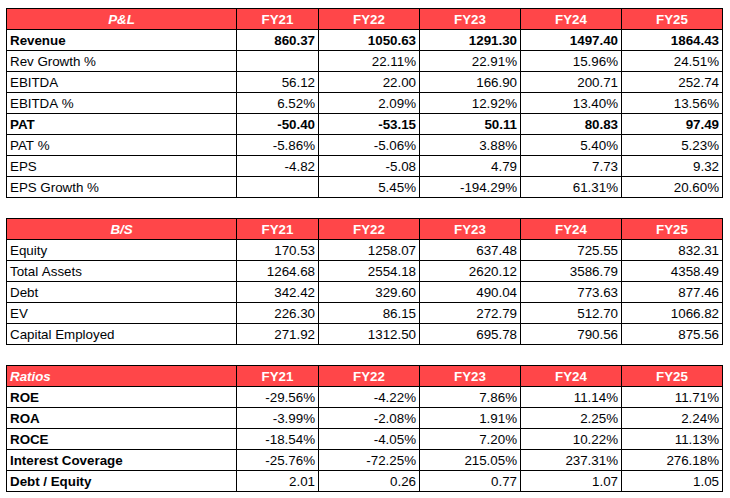

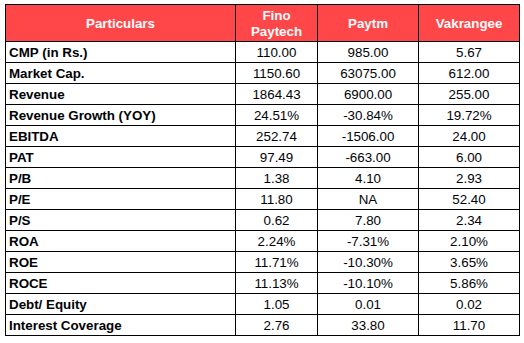

Nineteen years later, Fino Paytech is a fintech holding company with four subsidiaries, a 75% stake in a profitable listed payments bank, and a consolidated revenue base that crossed Rs.1,864 crore in FY25 — a figure that represents approximately 21% compounded annual growth from Rs.860 crore in FY21. Per the FY25 Annual Report filed July 2025, the standalone parent has also turned profitable (PBT of Rs.419 lakh after a loss of Rs.839 lakh in FY24), repaid all long-term debt, and improved its Debt Service Coverage Ratio from a deeply negative −3.48 in FY24 to a positive 10.31 in FY25. That is not a small turnaround. It is a structural one.

The business operates through a clear hierarchy. The listed subsidiary — Fino Payments Bank Limited (BSE: 543386) — contributes approximately 99% of consolidated group revenue, with FY25 turnover of Rs.1,84,710 lakh (Rs.1,847 crore) and net profit of Rs.9,253 lakh (Rs.92.5 crore). The parent holds 75% of that bank, provides the overarching technology platform and UIDAI-registered authentication infrastructure, and also houses three wholly-owned subsidiaries: Fino Trusteeship Services Limited (profitable, Rs.40 lakh PAT in FY25), FFPL Finserv Private Limited (microfinance NBFC, Rs.60 lakh loss), and Fino Financial Services Private Limited (dormant). The group in FY25 is leaner, more profitable, and structurally more defensible than at any point in its history.

The following are the main segments of Fino PayTech's technology-driven financial inclusion platform:

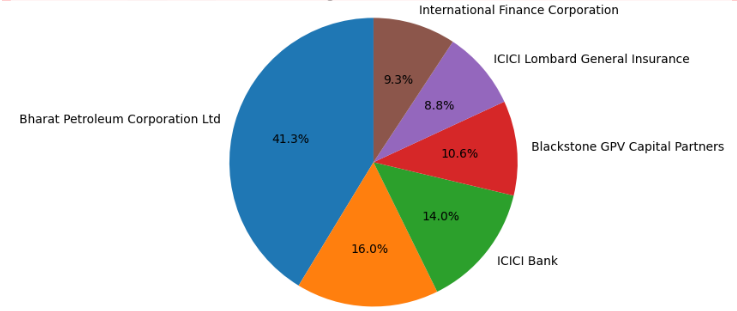

Fino Paytech's shareholder register, as disclosed in the FY25 Annual Report's notes to financial statements, is dominated by blue-chip institutional names. The company has no promoter holding — the founding shareholders have been fully diluted over successive institutional rounds. There are no Jains or Guptas listed under promoters. What remains is ownership by a state-owned oil major, India's largest general insurer, the country's largest private bank, a global private equity firm, and a World Bank group development finance institution.

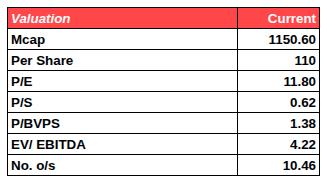

The financial picture is best understood through three lenses: the consolidated group, the standalone parent, and the bank. All numbers are sourced directly from the FY21,FY22,FY23, FY24, and FY25 Annual Reports of Fino Paytech Limited.

The consolidated revenue trajectory is unambiguous. From Rs.860 crore in FY21, the group compounded to Rs.1,864 crore in FY25 — a 21% four-year CAGR. Profitability followed and then accelerated: PAT moved from losses of Rs.50 crore (FY21) and Rs.53 crore (FY22) to profit of Rs.50 crore (FY23), Rs.81 crore (FY24), and Rs.97 crore (FY25). EBITDA followed the same arc — Rs.56 crore, Rs.22 crore, Rs.167 crore, Rs.201 crore, Rs.253 crore across FY21–FY25. The EBITDA margin expanded from 6.5% in FY21 to 13.56% in FY25 — a 700 basis point improvement that reflects genuine operating leverage in a network business where most incremental transactions flow at near-zero marginal cost once the infrastructure is in place.

Fino PayTech has evolved from a financial inclusion enabler into a scalable, profitable fintech platform with strong operating leverage and a clear shift toward higher-quality revenue streams like digital payments and CASA. Backed by a dominant stake in Fino Payments Bank, consistent revenue growth (~21% CAGR), and improving margins, the company today is structurally stronger, leaner, and well-positioned to benefit from India’s expanding fintech ecosystem—despite near-term risks around regulation and margin pressures.

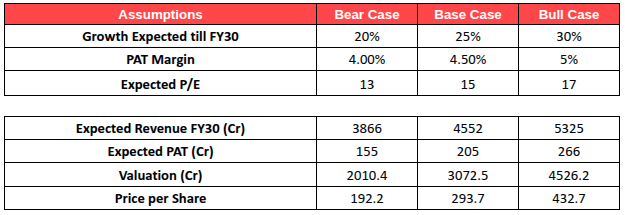

From an investment perspective, Fino PayTech is available on Sharescart as an unlisted opportunity, offering potential upside driven by digital growth, distribution expansion, and the optionality of a reverse merger. With improving fundamentals and strong industry tailwinds, it stands out as a compelling long-term fintech play in the unlisted space.

Independent Research Powered By - Actionable data