15 Days Price Change

Manika Bhalla

Manika Bhalla

Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills... Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills and a solid foundation in finance. Experienced in financial modeling and valuation, with a keen interest in equity research and investment analysis. Read more

Summary

India’s second largest refinery based on capacity located in Vadinar is Nayara Energy, which is shifting from being just a refiner to a downstream conglomerate player that will focus on petrochemical products, ethanol blends, and fuels. Notwithstanding the massive reduction in earnings per share of 50% in FY25 because of lower margins around the globe, the firm remains efficient and productive. In addition to venturing into polypropylene, ethanol blends, and steam cracking unit phase two, the projected return for FY2030 is between 11% and 101%. Nonetheless, the stock is valued at 29 times price-to-earnings, rendering it suitable only for long-term investment purposes.

Nayara Energy is one of the most strategically important downstream energy companies in India, based at the Vadinar refinery in Gujarat, which is India’s second largest single site refinery, producing about 8 percent of India’s total refined output. It employs more than 55,000 employees. Not only is it an energy fuel refiner; Nayara claims to be India’s strategic partner in ensuring the nation’s energy security and its alignment with the self-reliance agenda of India.

Founded and nurtured for almost two decades now, Nayara Energy is a joint venture of the Russian oil company Rosneft and is headquartered at its flagship Vadinar site in Gujarat. Nayara is presently undergoing one of the most revolutionary transformations within the Indian energy industry, changing from being a traditional pure-play refiner to become a next-generation downstream energy and petrochemicals company.

The Vadinar refinery's Nelson Complexity Index of 11.8 places it among the most sophisticated refineries globally — enabling it to process cheap heavy/sour crudes and extract premium high-margin products, a competitive advantage that translates directly to superior economics.

The company's EXCEL values (Energetic, Xtraordinary, Courageous, Ethical, Lead) underpin its culture and operational philosophy. Its leadership's stated mission is to transition from a fuel-centric model to an integrated crude-to-chemicals powerhouse, capturing the full hydrocarbon value chain from raw crude to polypropylene and ethanol.

The company operates in five different segments, with each serving different purposes in its value chain structure. The business model of Nayara has been specifically designed by the firm to ensure that high volume low-margin operations such as fuels are balanced by more value-oriented chemical and bio-fuel streams.

Refining (Engine Core)

Vadinar Refinery is Nayara's core asset and the starting point of its value creation process. Operating at 102.3% utilization level during FY25 – surpassing its nameplate capacity – the Vadinar refinery converts crude into petrol, diesel, aviation turbine fuel (ATF), LPG, bitumen, and various distillates with high-value content. The refinery's capability of processing 96.1% ultra-heavy and heavy crude provides it with the structural advantage of purchasing crude oil at reduced prices and converting it into more expensive light distillates, thereby benefiting from the complexity premium. During FY25, Nayara has applied for two Indian patents to improve ATF and MTO quality and for feedstock flexibility through asphaltene analysis.

Petrochemicals (Strategic Growth Engine)

The 450 KTPA Polypropylene (PP) plant, commissioned in July 2024 at a cost of approximately ₹6,000 Cr, is Nayara's most consequential strategic investment. Polypropylene is used in packaging, automotive components, textiles, and consumer goods — demand is structurally growing and far less cyclical than fuel margins. The plant uses propylene extracted from the refinery's Fluid Catalytic Cracking Unit as feedstock, making it a deeply integrated, low-incremental-cost operation. In its first nine months, the plant onboarded 650+ customers and produced 0.21 MMT. It currently represents approximately 8% of India's total PP capacity — from a standing start.

Retail Segment: Fuel Distribution

Nayara is one of the biggest private retailers in India with 6,683 petrol pumps spread across the nation, which constitute about 7% of the total distribution network in the country. FY25 marked the best retail year for Nayara with a record 8.3 million KL of fuel sold and the maximum throughput ever per retail outlet. Its retail network is completely automated, offering customers a digital-first shopping experience. The retail division converts the products of the refinery into end customer consumption, earning the complete value chain margin.

Bulk Institutional Segment: B2B

It includes long-term contracts for selling High-Speed Diesel (HSD) directly to institutional consumers like industries, fleets, and governments. For FY25, Nayara witnessed an increase of 9% in institutional bulk HSD sales, better than industry performance. Within the last two years, the company managed to triple its institutional bulk HSD market share from 3% to 9%. Although this segment does not offer quick cash flow like retail sales, it generates stable and consistent revenue from high-volume transactions.

Biofuel/Blended Fuel

E15 and E20 blended Motor Spirit have been launched by Nayara in FY25, which successfully managed to blend at a rate of 12.7% across its network, thereby helping the nation meet its objective of E20. Nayara already has land acquisition plans to establish two ethanol plants in Andhra Pradesh and Madhya Pradesh (initial capacity of 200 KLPD per plant with 1,000 KLPD in future with five plants). This segment is in sync with India's energy transition plans, diversifies revenues to a highly backed-up industry in terms of policy, and ensures marginally better earnings than plain old fuel retailing.

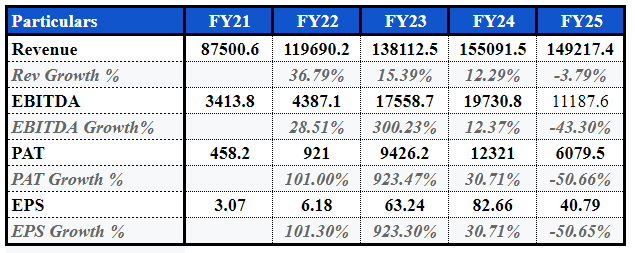

FY21 – Marginally Profitable, Recovery Post-COVID

Revenue was ₹87,501 Cr, and PAT was ₹458 Cr. The company was recovering from demand destruction due to the pandemic. Brent prices fell drastically and partially recovered, leading to low margins. The EBITDA margin was 3.9%, which was a very thin margin. The company’s operations were stable; however, there were financial limitations.

FY22 – Demand Recovery, Thin Margins Persist

There was a 36.79% rise in revenue to ₹1,19,690 Cr, marking the first time the revenue surpassed ₹1 lakh crore. This occurred owing to the recovery in global oil prices (Brent prices rose by ~82% year-over-year). There was a doubling of PAT to ₹921 Cr. However, high crude prices, increased interest on NCDs, and rising LNG prices limited margin growth. The company refined 126 types of crude (including eight new ultra-heavy crudes) and maintained an operational availability rate of 99.9%.

FY23 – Year of Gold: One-Time-In-Ten Years Bonanza

This is Nayara’s golden year. There has been a massive increase in EBITDA of 300% from ₹4,387 Cr to ₹17,559 Cr – an astounding 4 times increase within a year. PBT increased by 923% to ₹9,426 Cr. All of this happened due to the dislocations seen in the global oil market after the war between Russia and Ukraine. Nayara made hay while the sun shined by taking advantage of the Russian crude oil being sold at discounts owing to their technical ability to process heavy-sour crudes. The Global Diesel Crack spread peaked at a multi-decade high mark.

FY24 – Sustained Excellence, Smart Capital Allocation

Topline touched an all-time high of ₹1,55,092 Cr, while the PAT also recorded a record value of ₹12,321 Cr. But there was already a red flag: While raw material prices were up 18%, topline increased by just 12%. This is a classic example of the ‘negative jaws’ effect. Taking the help of a record EBITDA figure of ₹19,731 Cr, the company took aggressive steps of deleveraging, funding the ₹6,000 Cr PP plant, adding 500 new retail stores, and achieving a 3x share in the institutional HSD market. Trade receivables increased 39% (intentional, for funding institutionals), while inventories were on the rise (pre-feedstock for PP plant).

FY25 – The Profitability Dilemma

The FY25 was the most confusing year in Nayara's history. There was a decline of just 3.79% in revenue, resulting in ₹1,49,217 Cr. However, there were two major declines in profitability – one in PAT by 50.66% resulting in ₹6,080 Cr and EBITDA declining by 43.30% to ₹11,188 Cr. The year marked all-time highs in terms of throughput (146.4 Million bbls), retail volumes (8.3 MLN KL), and utilization rate (102.3%). Operating leverage is evident here, where the cost incurred (cost due to depreciation of PP plants, logistics cost, and workforce) was constant while the revenue per barrel reduced because of spread compression. The addition of capacity in the global refineries and price fluctuations of Brent between $69 and $92 per barrel resulted in compression of the spread refiners had access to.

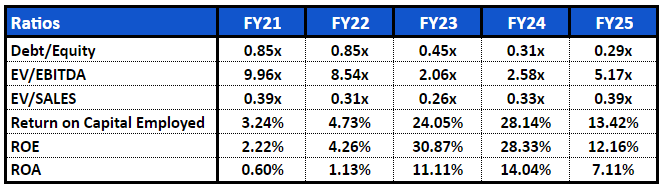

Debt / Equity: From Leveraged to Lean - D/E ratio dropped from a very high 0.85x in FY21-22 to a low of 0.29x in FY25 despite financing a ₹6,000 Cr petrochemical project. Impressive! Instead of paying out dividends and overextending itself, Nayara took advantage of its earnings windfall during FY23 to reduce leverage. Currently, at 0.29x D/E ratio, Nayara boasts the lowest level of conservatism in the industry.

ROCE, ROE, ROA: Permanently Higher - All of these three metrics remain 2-3 times higher even in FY25 correction than they were four years ago when they stood at ROCE 3.24%, ROE, and ROA 0.60%. The ROCE is currently at a record low of 13.42%, and ROA is at 7.11%. This shows that there is a permanent change in the earning power of this business; the company is significantly better run than before.

EV/EBITDA - EV/EBITDA moved from a very cheap 2.06x in FY23 to a very high 5.17x in FY25 not because the stock became expensive but because EBITDA declined. Once the PP plant begins operation and volumes reach unprecedented heights, the earnings should revert towards their mean of 2-3x EV/EBITDA.

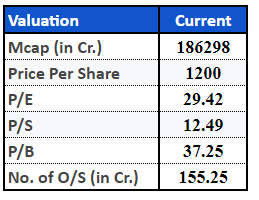

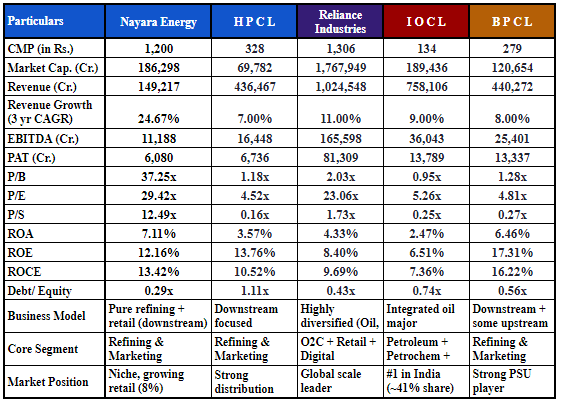

With the current valuation of ₹1,200 per share (Mcap: ₹1,86,298 Cr), the company is trading at a trailing P/E multiple of 29x, P/B multiple of 37x, and P/S multiple of 12.5x – making it one of the most expensive companies across all valuation metrics and far more than its PSU counterparts like HPCL’s 4.5x P/E ratio, IOCL’s 0.95x P/B ratio. The market is not valuing it based on its role as a refiner; it is valuing it based on the transformation story of petrochemicals.

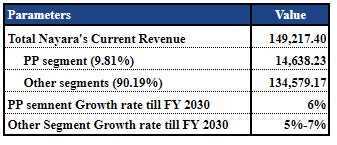

👉 Based on estimates from multiple sources, including ChemAnalyst, ICIS, and Mordor Intelligence, which indicate growth in the range of ~5%–7.5%, we have assumed an average CAGR of 6% for the India polypropylene/plastics market.

👉India’s oil demand is expected to grow at ~3.1% CAGR through 2030 (IEA), forming the base for refining volume growth. Nayara Energy’s refinery utilisation levels (CARE Ratings) suggest limited capacity-led upside, aligning volume growth to ~3–4%. Realisations are assumed to grow at ~2–3% based on World Bank oil price outlooks. Additional upside of ~1–2% is expected from retail expansion (Financial Express), while export pressures from global oversupply (Business Standard) may reduce growth by ~1–2%. Overall, non-petrochemical revenue is expected to grow at ~5–7% CAGR till FY2030.

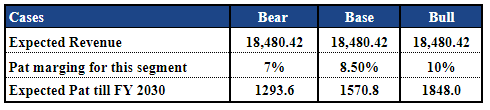

PP segment -

👉After correcting due to oversupply, polypropylene margins are expected to stabilize at mid-cycle levels, with EBITDA margins around 12–15%. Demand growth of ~4–5% should absorb excess supply, but continued capacity additions—especially from China and the Middle East—will limit upside, keeping PAT margins in the 7–10% range.

Other segments -

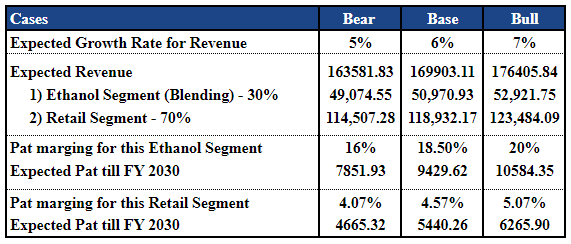

👉India’s ethanol blending target is expected to increase to 30% by 2030, up from ~20% currently (Business Standard). This policy-driven shift implies partial substitution of petrol with ethanol, leading to the creation of an ethanol-linked revenue component.

👉Retail margins are kept stable in the bear case due to the structurally low-margin nature of fuel retailing. In the base and bull cases, margins are increased by 50 bps each, supported by operating leverage, higher throughput, and a growing share of domestic retail sales, reflecting gradual and realistic improvement.

👉We have modelled the ethanol segment using industry cost benchmarks from Balrampur Chini Mills, deriving a unit-level spread of ~₹13–14 per litre. After adjusting for blending dynamics and operational costs, we assume sustainable PAT margins of 16–20% for the ethanol segment, reflecting its structurally higher profitability compared to the core refining business.

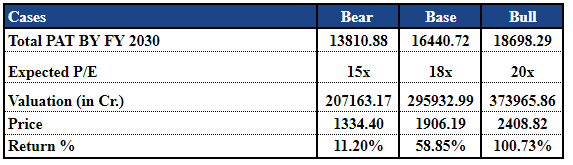

👉While the company currently trades at ~29x P/E, we have conservatively applied a lower range of 15x–20x to account for the cyclical nature of refining margins. However, we do not assume a deep discount (e.g., 10x average industry value), as the increasing contribution from ethanol blending is expected to improve earnings quality, stability, and overall business mix, justifying a moderate re-rating over time.

The FY2030 outlook for Nayara Energy is highly promising regardless of the scenario. The company can deliver an 11% gain even under the pessimistic scenario, while the base and optimistic scenarios offer gains of around 59% and 101%, respectively, compared to the current stock price. The major earnings drivers are Nayara’s ethanol blending segment expansion, consistent retail segment performance, and revival of polypropylene margins, which should result in PAT of ₹13,810–18,698 Crore in FY2030.

a) Integration of Petrochemicals — Phase 2 Steam Cracker

The feed analysis for Phase 2, which entails a 1.2 MMTPA world scale steam cracker facility, along with other derivative units, has already commenced. A steam cracker is a unit that cracks naphtha/ethane to produce ethylene and propylene, the base materials of plastics and chemicals. It would enable Nayara to become a one-stop destination for all forms of petrochemical products from a mere polypropylene manufacturer. The presence close to the petrochemical demand centres of Western India and integration with the refinery makes Nayara structurally cost-advantaged relative to greenfield sites.

b) Refinery Optimization Projects

Various reliability and capacity improvement projects are currently being undertaken by the company such as VGO MHC (Mild Hydrocracker) revamp, to increase the yield of middle distillates; Coke Drum Replacement, to ensure improved operational reliability; and SBM-2 (Single Buoy Mooring), to accommodate more crude tanker sizes.

c) Ethanol and Biofuels Buildout

The project by Nayara to construct five ethanol plants to produce 1,000 KLPD is in perfect harmony with the policy-led aim by India to reach a 30% E30 blending target by 2030. Ethanol projects enjoy margin advantages (16%–20% for PAT) compared to fuel retailing (4%–5%) due to its revenue stream, which is managed by the government. The first two ethanol plants (each producing 200 KLPD) will be built in Andhra Pradesh and Madhya Pradesh, laying the groundwork for a biofuel venture that will add value to the bottom line by FY28–FY30.

d) Retail Growth and Digitization

Given that there are 6,683 existing outlets and a fully automated retail network by Nayara, it will definitely gain market share within the fast-growing fuel retail market of India. Fuel consumption in India is estimated to increase by 3.1% CAGR through 2030 (IEA). Digital Retail of Nayara has created an opportunity for data-enabled management of outlets, loyalty programs, and enhanced operational efficiencies.

e) Internal Market Deepening

India's economy growing at a rate of 6.5%, along with the increasing rate of urbanization and the penetration of automobiles in the country, will generate an internal demand support to every market that Nayara is operating in, which includes fuel, petrochemicals, and biofuels. Also, its marketing strategy of being "In India, For India" is a smart decision, considering the current geopolitical environment.

Nevertheless, Nayara Energy stands out as a sound company whose earnings pressure is due to cyclical reasons rather than poor operational performance. The company had to suffer huge drops in profitability in FY25 due to poor refining margins, while at the same time setting record-high throughput figures and operating above capacity, generating its record high retail sales.

In light of the current share price of ₹1,200, the valuations look stretched due to a high multiple in comparison to other stocks. Although the premium valuation is well-deserved considering the company's growth potential, efficiency, and low debt load, all of the expected growth in the coming years appears to be priced into the stock.

As a result, Nayara Energy may work well only in hands of long-term investors who can sustain the company during a cyclical pressure. The best choice for such an investor would be to have faith in India's energy consumption growth and transformation.

Nonetheless, the situation is not without its uncertainties. Assumptions on growth within each segment are in line with broader industry dynamics, yet successful execution within new fields such as petrochemicals and ethanol, along with margin and regulatory cycles, will be essential for continued profitability. The normalised approach to valuation implies that a more appropriate multiple is necessary.

In conclusion, Nayara is a business with sound fundamentals, operating in a cycle of recession—where prospects exist for the future, although valuation requires caution at present. This share is available at Sharescart.

Independent Research Powered By - Actionable data