15 Days Price Change

URVASHI TOTLA

URVASHI TOTLA

MBA post graduate and CFA Level II cleared, with NISM certifications in Series VIII and XV... MBA post graduate and CFA Level II cleared, with NISM certifications in Series VIII and XV. Skilled in Financial Modeling, Valuation, and Portfolio analysis, with a strong interest in equity research and investment strategies. Read more

Summary

Summary

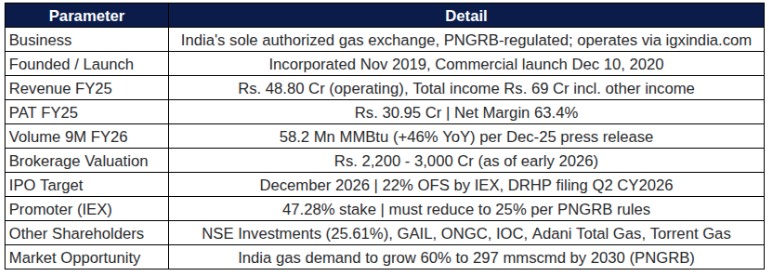

Indian Gas Exchange Limited (IGX) is India’s first and only PNGRB-authorized natural gas trading exchange — a regulatory monopoly sitting at the intersection of India’s energy transition and accelerating gas demand. With a 63.4% net margin, zero debt, ₹251 Cr cash pool, and an IPO expected before December 2026, IGX is transitioning from an early-stage platform into a structurally superior exchange business. The upcoming IPO at ₹2,200–3,000 Cr represents fair pricing on trailing metrics but is justified on forward earnings given 30%+ PAT CAGR visibility and India’s gas market set to grow 60% by 2030.

Indian Gas Exchange Limited (IGX) is not merely another commodity trading platform. It is a PNGRB-authorized monopoly — the only government-licensed entity in India authorized to operate a natural gas trading exchange. This single fact transforms IGX from an interesting business into a structurally rare investment opportunity: a regulated toll booth on one of India's most critical energy highways.

Incorporated in November 2019 and commercially launched on December 10, 2020, IGX is an IEX (Indian Energy Exchange) venture, operating via igxindia.com. In just over four years of commercial operations, IGX has grown from virtually zero revenue to ₹48.8 Cr in FY25 operating revenue, achieving a net profit of ₹30.95 Cr — a 63.4% net margin that rivals the best exchange businesses globally.

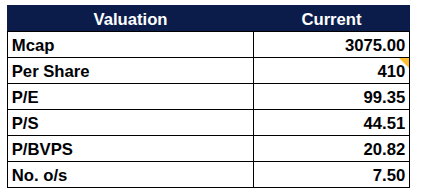

The exchange operates like a stock exchange but for molecules. Buyers and sellers of natural gas — city gas distributors, fertilizer plants, power generators, and industrial consumers — access IGX's platform to discover transparent market prices, execute trades, and settle contracts. The promoter (IEX) holds 47.28% but must reduce its stake to 25% per PNGRB rules — making the IPO a structural necessity, not just a choice. The IPO, targeting a 22% OFS by IEX, is expected by December 2026 with the DRHP filing in Q2 CY2026.

The Regulatory Moat in Plain Language: India's Petroleum and Natural Gas Regulatory Board (PNGRB) grants the exchange licence. As of today, only IGX holds this licence. Every unit of natural gas traded on an exchange in India — every discovery of transparent price, every standardized settlement — must flow through IGX. This is not a competitive advantage that can be copied. It is a government grant.

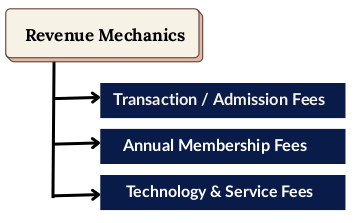

IGX's revenue mechanics are straightforward and scalable. Revenue is earned in three streams: Transaction/Admission Fees on each trade executed, Annual Membership Fees from registered participants, and Technology & Service Fees for platform access. The critical insight is the cost structure: once the technology platform is built and regulatory licences are secured, the marginal cost of each additional trade is near zero. This creates the explosive operating leverage characteristic of great exchange businesses.

This is the dominant revenue driver. IGX earns a fee on every MMBtu of natural gas traded. In the first nine months of FY26 alone, total volumes traded hit 58.2 million MMBtu — up 46% year-on-year per December 2025 press releases. As volumes compound, this revenue stream scales directly without proportional cost increase. The market currently trades spot and daily contracts; PNGRB approval for 1–2 year forward contracts and R-LNG booking would be a significant step-change catalyst.

Annual Membership Fees — the Sticky Base

Every participant in the exchange, whether it's a city gas company, an industrial buyer, or an aggregator, pays an annual membership fee. This sets up a regular, subscription-like revenue that increases as India's gas ecosystem grows. India's PNGRB forecasts that natural gas demand will hit 297 mmscmd by 2030, a 60% rise from current levels. This would significantly expand IGX's potential membership pool.

Fees for platform access, connectivity, and services add software economics to a physical commodity exchange. These fees increase with the number of participants and usage, not just volume. This approach helps diversify revenue and encourages loyalty.

A feature often overlooked is that IGX's balance sheet holds around ₹251 Cr in cash and current investments (FY25). This amount generates about ₹20 Cr a year in other income, which is nearly 30% of total income. This recurring feature is typical of exchange businesses worldwide. As profits are retained and the cash reserves increase, this secondary income stream quietly grows alongside the operating business.

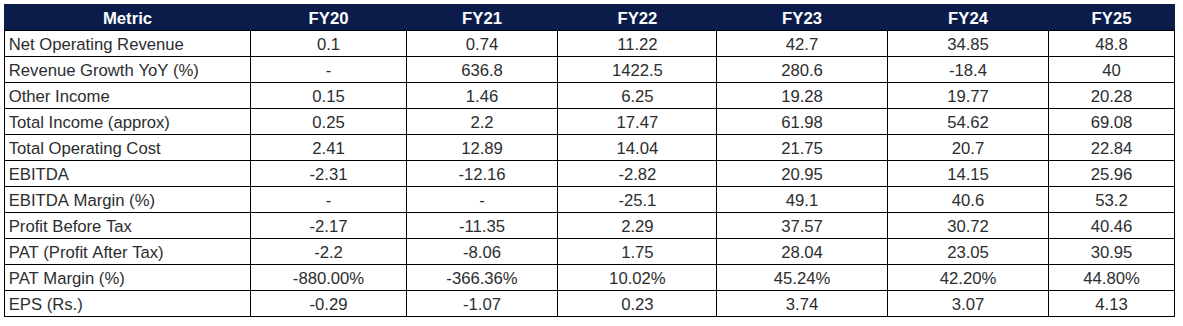

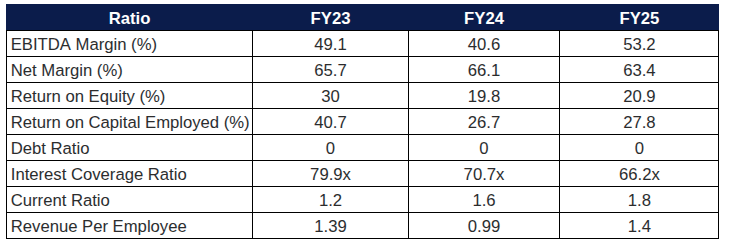

IGXs financial journey is like a story with three parts. The first part is when IGX started selling things and lost a lot of money from FY20, to FY22. Then something big happened in FY23. Igx started making money really fast. After that IGX sold a lot of things in FY24 but the prices were low so they did not make much money as they wanted. Now from FY25 IGX is getting back on track and things are looking good. The numbers below show us exactly what happened to IGX.

IGX was virtually a startup in FY20 with ₹0.10 Cr in operating revenue. The heavy operating costs in FY21 reflect the platform, technology, and team build-out needed to establish a credible regulated exchange. By FY22, revenues crossed ₹11 Cr — a 1,423% increase — but the company was still loss-making as fixed costs remained high relative to early volumes. This is exactly what the early innings of an exchange business look like: high fixed investment, steep ramp-up curve.

FY23 was transformational. Revenue surged 281% to ₹42.7 Cr, PAT crossed ₹28 Cr, and net margins hit 65.7% — demonstrating the operating leverage of the platform model in full force. The energy crisis spillover from global gas markets drove exceptional volumes. India's city gas distribution companies, industrial buyers, and power plants flocked to IGX as a transparent pricing mechanism. The exchange proved its value proposition decisively.

FY24 revenue fell by 18.4% compared to year to ₹34.85 Cr.

The reasons for this drop were clear and outside of our control.

Some key factors were:

Despite this the company still made a profit of ₹23.05 Cr with a net margin of 66.1%.

This shows that our business model is strong when sales are low.

FY25 delivered a strong recovery — revenue +40% to ₹48.8 Cr, PAT +34% to ₹30.95 Cr, and EBITDA margins at a record 53.2%. The 9M FY26 volume data (+46% YoY) suggests FY26 will be another step-change year, with IGX on course to cross ₹65–70 Cr in operating revenue.

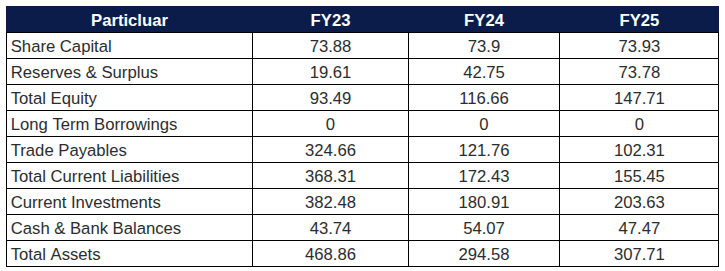

IGXs balance sheet shows they are good at using their money

The company does not owe any debt has few fixed assets and has a large amount of cash and investments saved up from their profits. This is what a good exchange business should look like at this point. IGXs balance sheet is an example- They have done a job with their money which shows they are efficient, with capital.

Note: Large trade payables represent settlement amounts owed to gas sellers, offset by corresponding receivables from buyers — a standard feature of exchange businesses.

Zero long-term debt. Net fixed assets of just ₹5.98 Cr confirm the asset-light, software-economics nature of the platform. Equity has grown consistently from ₹63.55 Cr in FY21 to ₹147.71 Cr in FY25 — entirely driven by retained profits. The ₹251 Cr cash and investment pool generates ~₹20 Cr/year in other income, a perpetual compounding engine.

The 63–66% net margins are structurally typical for exchange businesses globally — once the technology platform is built, each additional unit of volume carries near-zero marginal cost. ROE of ~21% is understated because the denominator (equity) is growing rapidly with large uninvested cash reserves. Adjusted for excess cash, ROE on operating assets would be significantly higher. The improving current ratio (1.2x → 1.8x) reflects a steadily strengthening liquidity position.

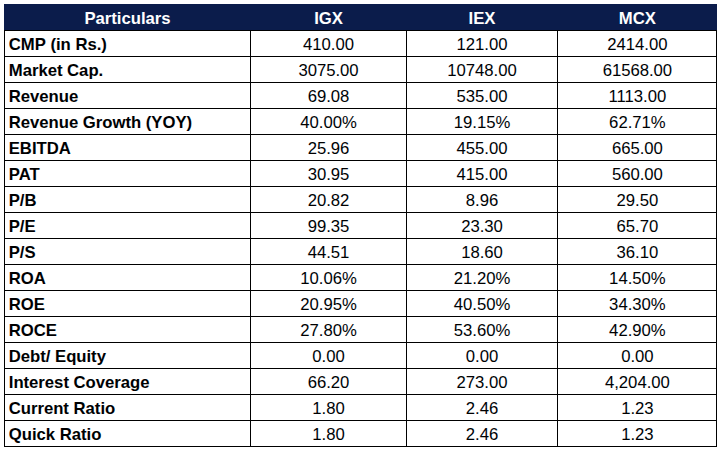

To contextualize IGX's valuation and growth profile, a comparison with its closest listed peers — IEX (Indian Energy Exchange, also its parent/promoter) and MCX (Multi Commodity Exchange) — is instructive. Both are mature listed exchange businesses; IGX is the growth-stage outlier.

IGX trades at a significant premium on trailing multiples (P/E ~99x vs IEX's 23x) — a reflection of its early-stage growth profile and monopoly status, not a validation of current earnings. IEX itself traded at similarly elevated multiples during its early listed years before earnings growth compressed the multiple. IEX remains the best-in-class peer on profitability and returns (ROE 40.5%, ROCE 53.6%) — and represents the trajectory IGX is likely to follow as it scales. MCX's strong growth (63% revenue CAGR) at 65x P/E provides a useful benchmark for what growth-stage exchange valuations look like post-IPO normalization.

The PNGRB projects India's natural gas demand to grow from ~185 mmscmd today to 297 mmscmd by 2030 — a 60% increase over five years. This is not speculative; it is backed by government infrastructure spending on city gas distribution networks (CGD), the PM Urja Ganga pipeline, industrial gas adoption, and the transition away from coal in power generation. Every additional mmscmd of gas traded in India is potential volume for IGX, the only licensed exchange to facilitate price discovery. This is a structural demand tailwind with a hard policy mandate behind it.

Currently, IGX primarily trades spot and day-ahead contracts. PNGRB approval for 1–2 year forward contracts would dramatically expand IGX's addressable market — large industrial consumers and power plants currently bypass the exchange for long-tenure bilateral contracts. Bringing these onto the exchange would add significant volume. Similarly, approval for Regasified LNG (R-LNG) booking on the exchange would connect India's growing LNG import infrastructure to the exchange ecosystem, creating a whole new product vertical. These two approvals are the single most powerful near-term catalysts for IGX's volume and revenue trajectory.

IGX's cost base (₹22.84 Cr in FY25) is largely fixed — technology infrastructure, regulatory compliance, team, and corporate costs. Each additional trade costs IGX almost nothing. 9M FY26 volumes of 58.2 million MMBtu (+46% YoY) are heading toward a full-year record. If volumes compound at 35–40%, revenue should grow proportionally while costs grow at 10–15% — producing powerful operating leverage that will drive EBITDA margins toward 60%+ in the medium term. The business is at precisely the point where volume growth converts most powerfully into earnings.

IEX (IGX's promoter) currently holds 47.28% — well above the 25% maximum permitted by PNGRB. The IPO is therefore not optional but structurally mandated. The planned 22% OFS by IEX and DRHP filing in Q2 CY2026 will bring IGX into the public market at a projected valuation of ₹2,200–3,000 Cr (brokerage estimates). Listing provides price discovery, liquidity for existing shareholders, and access to institutional capital for future growth. For unlisted investors entering now at ~₹410/share, this is the catalytic liquidity event.

IGX's cap table reads like a who's who of India's energy and financial establishment. Beyond IEX (47.28%), shareholders include NSE Investments (25.61%), GAIL, ONGC, IOCL, Adani Total Gas, and Torrent Gas. These are not passive investors — they are India's largest gas producers, pipeline operators, distributors, and market makers. Their combined stake ensures IGX has the deepest possible access to liquidity, deal flow, and regulatory relationships. The alignment of interests between IGX and its shareholders is a powerful underappreciated structural advantage.

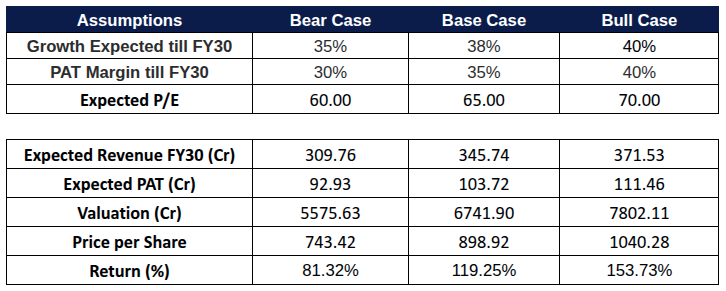

Assuming 35–40% revenue CAGR through FY30 — supported by historical growth, strong FY26 volume momentum, and structural demand tailwinds — here are the modelled outcomes with P/E normalization to 60–70x post-IPO, aligning with listed exchange comps.

The bear case assumes revenue moderation and P/E compression consistent with a slower growth trajectory. The base case — a 38% CAGR with 35% PAT margins and 65x P/E — delivers approximately 2.2x return from current levels by FY30. Even in the bear case, returns of 81% over five years represent a solid outcome for a regulated monopoly business with zero debt.

Indian Gas Exchange is a structurally superior business at an early but rapidly accelerating growth stage. The combination of a regulatory monopoly, a software-economics platform model, zero debt, ₹251 Cr cash pool, 63% net margins, and institutional backing from India's largest energy companies creates a rare investment profile — a toll booth on an energy highway that is growing 60% over the next five years.

The upcoming IPO at ₹2,200–3,000 Cr (brokerage estimates) represents fair to slightly full pricing on trailing metrics, but is justified on forward earnings given 30%+ PAT CAGR visibility. Key watch items: FY26 annual revenue (confirming 40%+ growth), PNGRB approval for 1–2 year contracts and R-LNG booking, and IPO DRHP filing in Q2 CY2026.

DISCLAIMER: This article is for informational and research purposes only. It is not investment advice or a solicitation to buy or sell any security. Valuations are model-based estimates derived from publicly available information. The author is not a SEBI-registered research analyst. Past performance is not indicative of future results. Readers should conduct their own due diligence and consult a registered financial advisor before making any investment decisions. This share is available with Sharescart.

Independent Research Powered By - Actionable data