15 Days Price Change

Manika Bhalla

Manika Bhalla

Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills... Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills and a solid foundation in finance. Experienced in financial modeling and valuation, with a keen interest in equity research and investment analysis. Read more

Summary

Hinduja Leyland Finance Limited is a vehicle-centric NBFC with a significant advantage given its integration with Ashok Leyland to efficiently source and underwrite. Despite past rate cycles and pandemic-related challenges, the company has strengthened its position through AUM growth, expansion, and an upgrade to AA+ ratings. With its improving business mix, rate relief, operating leverage, and its upcoming merger with NDL Ventures Limited, the company is transitioning from cyclical slowdown to growth and re-rating.

Hinduja Leyland Finance Limited (HLF) is not merely a run-of-the-mill NBFC. Rather, it is a focused financial services entity of one of India's most illustrious conglomerates, built around the commercial vehicle and auto finance universe centered around Ashok Leyland Limited, India's second-largest commercial vehicle manufacturer. While this may not sound too glamorous at first sight, this is not a mere footnote in terms of corporate ownership. Rather, this is at the DNA core of HLF, and this fundamentally influences how they win clients, manage credit risk, and ultimately position themselves competitively against other NBFCs in the long term.

Incorporated in 2008 and headquartered at Bandra-Kurla Complex, Mumbai, with its operating location at Chennai, Hinduja Leyland Finance Limited is classified as a 'Systemically Important Non-Deposit Taker Non-Banking Financial Company' (NBFC-ND-SI) at the 'Middle Layer' of RBI's Scale Based Regulation framework. In other words, HLF is subject to the same exacting prudential parameters and regulations as all other financial institutions, including a minimum CRAR requirement of 15%, mandatory risk-based internal audit (RBIA), and strict corporate governance requirements, without the corresponding benefit of accepting public deposits, unlike banks

The Ashok Leyland relationship provides a 'Walled Garden' for customer acquisition. Every truck, bus, or LCV sold through the Ashok Leyland distribution network represents a potential HLF financing relationship—a captive origination engine that most NBFCs spend decades trying to develop.

Most NBFCs invest enormous resources to acquire customers through dealer incentive programs, direct sales agents, and digital marketing. HLF's partnership with Ashok Leyland fundamentally alters this cost structure. When a commercial vehicle is sold through one of Ashok Leyland's dealers, HLF is at the table as the financing partner. The cost of acquiring customers is lower. Credit assessment is simpler because the underlying asset is a well-understood Ashok Leyland product with known residual values. Once a customer is acquired, HLF can leverage this relationship to sell more products through refinancing, top-up loans, and LAP products.

Moreover, this advantage has been further reinforced in FY25, wherein Ashok Leyland has made a preferential issue of one crore equity shares to HLF—a direct investment in HLF's capital base and unambiguous promoter commitment to the NBFC's long-term growth story.

Vehicle finance is the largest business segment for HLF and the main engine of its business. It includes the entire range of motorised two-wheelers, three-wheelers, passenger vehicles (cars and SUVs), LCVs, MHCVs, SCVs, and construction equipment. The increase of 15% in FY25 is significant because it has surpassed the overall growth in the Indian automotive industry, which grew by only 7.3%. This shows that HLF is gaining traction and not just benefiting from the industry trend.

LAP has turned out to be among HLF’s fastest-growing and most critical segments. While LAP is growing at 31% in FY25 as compared to 36% in FY24, it offers two things that vehicle finance by itself does not: better yields and diversification of collateral. LAP loans are secured against residential as well as commercial property, offering a significantly lower default risk profile.

The dramatic decline in portfolio buyouts is often mistaken for a negative trend. However, this is not true. Portfolio buyouts involve buying pools of loans created by other lenders. Portfolio buyouts have traditionally been a tool for HLF to expand rapidly and earn securitization fees. However, loans acquired through this route have lower yields, worse data on customers, and lower Customer Lifetime Value.

HHF, the housing finance subsidiary of HLF, is arguably one of the most under-the-radar high achievers within the Group. It has delivered a 54% growth rate in FY24 and continues to grow as a result of the housing finance cycle in India, which is underpinned by the country’s urbanization story, the government’s affordable housing initiatives, and the growing aspirations of first-time homebuyers in Tier II and Tier III cities.

In terms of the portfolio, HHF plays a very critical role from the perspective of Asset Liability Management (ALM). Vehicle finance loans have a tenure of 3 to 5 years, while home loans have a tenure of 15 to 20 years. By consolidating both of these in the same book, HLF can better match its long-term liabilities with its long-term assets, which helps to reduce the maturity mismatch risk, which can lead to liquidity pressures for vehicle finance NBFCs.

Gaadi Mandi is a digital marketplace for buying/selling used vehicles. Currently, it is in an investment phase where it is making losses (₹1,060 lakhs loss in FY24). Its contribution to HLF in terms of money is negative in nature. However, its strategic significance is high. By controlling the used vehicle transactional layer, HLF gets three long-term advantages: access to upstream finance opportunities at the time of vehicle discovery/purchase; real-time vehicle valuation information to better manage LTVs of the entire fleet finance book; and an online customer engagement channel to reduce future dependence on cost-intensive DSA networks.

The Government of India's PM E-Drive initiative has significantly accelerated EV adoption in 2W and 3W segments. For HLF, which already has a strong ground-level presence in 2W and 3W financing in Tier II and Tier III markets, this provides a natural extension to the existing model. Although EV financing is currently at a low single digit percentage of the total book, this provides a secular growth opportunity over FY26-28.

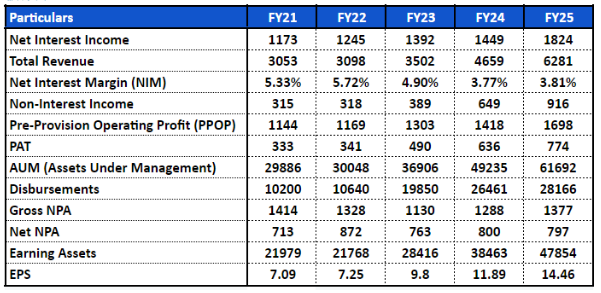

The financial journey of HLF over the five-year period from FY21 to FY25 can be divided into three acts: a halt brought about by the pandemic, a growth spurt that hid underlying earnings volatility, and a structural change that, although unfinished, points in a specific direction.

Hinduja Leyland Finance emerged financially healthy post-pandemic, with its CRAR standing at 18.71% and AA- rating holding good. However, its operational performance was not satisfactory. Its AUM increased by merely 1% to ₹30,048 crore, despite a 50% increase in M&HCV sales.

The core issues continued:

Impairment levels remained high at around ₹74,000-75,000 lakh.

Securitisation continued to be high at over 54% of PBT.

Lending profitability remained low.

Rural stress, aftereffects of COVID, and supply chain issues continued to affect repayment behavior. The treasury moved from profitability to loss. Cost pressure continued with flat disbursements.

The growth story of Hinduja Leyland Finance is evident with doubling of disbursements to ₹19,850 crores and AUM growth of 33% to ₹49,235 crores. PAT growth of 30% to ₹636 crores also looks attractive at first glance.

However, the underlying quality of the balance sheet remains substandard. Core operating PBTs are minimal, indicating the huge dependency on securitization.

The CRAR has dipped to 17.26%. Higher-cost funding and failure to adhere to norms have resulted in the compression of margins from 5.72% to 3.77%.

Hinduja Leyland Finance has recorded signs of recovery with its revenue increasing by 35% to ₹6,281 crores, AUM increasing by 25% to ₹61,692 crores, an increase in CRAR to 19.29%, an increase in asset quality, and a marginal increase in NIM, driven by the upgrade in credit ratings to AA+.

Key positives are the reduction in securitization, reflecting better earnings quality.

However, challenges remain, with finance costs increasing higher than revenue, fee costs increasing sharply, and lower growth in disbursements compared to the industry, reflecting limited market share expansion.

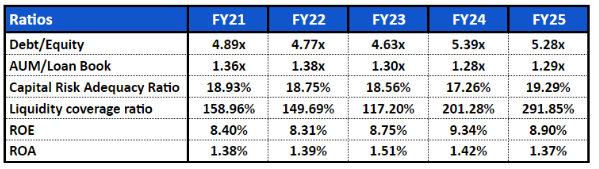

Hinduja Leyland Finance’s leverage has increased moderately, as its Debt/Equity ratio increased from 4.63 times in FY23 to 5.28 times in FY25.

The AUM/Loan book ratio has shown a gradual improvement over time, decreasing from 1.38 times in FY22 to 1.29 times in FY25.

The capital adequacy ratio decreased over time but increased significantly to 19.29% in FY25 after the infusion of capital.

The liquidity coverage ratio has shown significant improvement, increasing to 291.85% in FY25.

The profitability ratios have shown a range-bound performance over time. The company’s Return on Equity has shown fluctuations between 8% and 9%, and Return on Assets has decreased slightly to 1.37%.

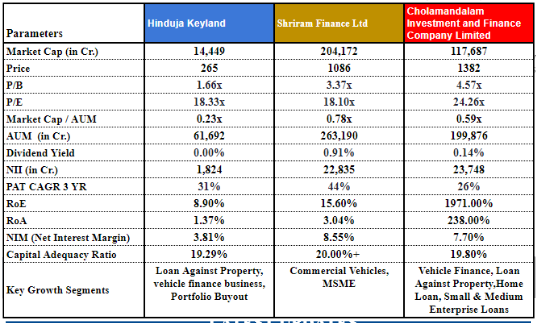

HLF is trading at a discount of 1.66x P/B compared to its peers like Shriram Finance (3.37x P/B) and Cholamandalam Investment and Finance Company (4.57x P/B).

The stock also trades at a discount in terms of its Market Cap to its AUM ratio, which stands at just 0.23x. This is due to its lower valuation per unit of its loan book.

The stock is trading at a discount due to its lower profitability. Its NIM stands at 3.81%, and its RoE stands at 8.9%.

HLF is trading at a similar P/E ratio to its peer Shriram Finance. Its P/E stands at ~18x. This means that the stock is not being discounted for its earnings.

HLF has delivered a PAT CAGR of ~31%. This has been done despite its lower NIM.

As the interest rate cycle continues to evolve, driven by actions from the Reserve Bank of India, interest rates for NBFCs start to ease after a prolonged period of upward pressure. This provides a natural tailwind to our margin expansion story, as lending yields typically lag changes in funding costs.

In addition, a better credit rating provides better access to lower-cost funding sources such as the bond market, reducing dependence on more expensive funding sources such as banks.

As a result, a structural improvement in our cost of funds is visible, and this is likely to result in margin expansion over time.

In other words, the business is transitioning from a headwind to a tailwind for our margin expansion story.

Vehicle finance branch networks go through a well-known maturation curve. Branches take 18 to 24 months to fully penetrate the local customer market. The majority of HLF’s branch expansion was in FY23 and FY24. The peak of the maturation curve is therefore in FY25 and FY26. As branches come of age, disbursement growth will accelerate beyond the current 6% to 15-20% without an increase in fixed costs. The same number of employees, same branches, same technology – 2.5 to 3 times the amount of loan origination. This is the operating leverage effect that transforms a headwind in margins into a tailwind in margins.

The FY25 growth trajectory of the Indian auto industry, with 2W growth at 9.1%, SUVs contributing 65% of PV sales, and CVs benefiting from government infrastructure spends, is set to further intensify in FY26. The premiumisation theme has long-term structural growth written all over it, with the average loan ticket size for all vehicles set to rise with increases in household incomes and changes in aspirational profiles. This will continue to positively impact HLF's NII per relationship. The PM E-Drive scheme is accelerating the adoption of EVs in the 2W and 3W segments, thereby creating a new financing vertical. Government infrastructure spends, with ₹10.1 lakh crores of capex in FY25 and set to rise in FY26, will continue to support the MHCV segment, which has a direct impact on HLF's CV business.

Used vehicle finance is one area that requires special focus for growth. India's used vehicle market is rapidly becoming more formalized in terms of documentation standards and electronic transaction facilities. In addition, the growing desire for value-for-money products will also benefit the used vehicle market. HLF's Gaadi Mandi has the potential to become a market leader in the used vehicle space as it moves from investment to revenue generation in FY26-27.

The merger of Hinduja Leyland Finance Limited with NDL Ventures Limited represents a major change in the structure of the company.

The entire business of HLF, including operations, assets, and the financial platform, will be owned by the listed entity after the merger, essentially changing the structure of the company from an unlisted NBFC to a listed financial services company.

What it means in simple terms

• Shareholders will receive the listed entity’s shares in return through the swap mechanism

• The business remains the same; the structure has changed

• The company gets the benefit of market participation and price discovery

Why this matters

• More transparent and accessible for investors

• Valuation discovery is also easier in the listed space compared to the unlisted space

• More avenues for capital-raising in the future

• Aligns with the broader market and institutional participation

Hinduja Leyland Finance Limited is an undervalued company, not because of any issues in its fundamentals but because of the challenging interest rate cycle it has gone through in the past few years. However, in this challenging scenario, the company has quietly strengthened its foundation by doubling its AUM, significantly increasing its branch footprint, lifting its credit rating to AA+, and growing its earnings per share compound annually. The challenges that the company faced were cyclical rather than structural in nature, as its margins were impacted by the interest rate cycle, its operating leverage is still to materialize as its newer branches open up, and its earnings quality is steadily improving as it moves towards direct lending. However, what is significant is that it enjoys an unparalleled relationship with Ashok Leyland, giving it an unparalleled distribution advantage. However, an upcoming merger with NDL Ventures Limited is an important inflexion point in its history as it moves to become a listed entity. The company seems to be transitioning from a challenging phase in its history to a much better phase with industry conditions as well as structural changes in its favor. This share is available with Sharescart.

Independent Research Powered By - Actionable data