15 Days Price Change

Manika Bhalla

Manika Bhalla

Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills... Economics Honors graduate and CFA Level ll cleared, equipped with strong analytical skills and a solid foundation in finance. Experienced in financial modeling and valuation, with a keen interest in equity research and investment analysis. Read more

Summary

HDFC Securities has completed a remarkable transformation - from a struggling full-service broker losing clients to discount competitors in FY23, to recording its highest-ever PAT of ₹1,125 crore in FY25. Backed by HDFC Bank and serving 6.8 million clients across four differentiated platforms, the company has successfully evolved into a lending-backed, digitally driven financial institution. Despite delivering the peer group’s highest revenue growth and ROE, it trades at the lowest P/E of 14.56x — suggesting modest undervaluation. With India’s equity participation at just 7% and a base case price target of ₹14,765 by FY2030, the long-term investment thesis remains compelling.

HDFC Securities Limited (HSL) is a leading full-service brokerage and wealth management company in India and has been in business for more than a quarter-century, having started in 2000 as a subsidiary of HDFC Bank, which is the largest bank in India in the private sector. Over this period, it has changed from a traditional broker to a digital investment ecosystem with 6.8 million clients across retail, high net worth individual, and institutional clients.

HDFC Securities’ institutional background gives it a formidable two-moat business model: HDFC’s trust equity and its 130+ branches across India, and a high-end digital platform that currently generates 96% of its brokerage digitally.

HDFC Securities has moved from a pure brokerage model to a credit model in recent years and Margin Trade Funding has become a significant growth driver for it.

Silver Jubilee Milestone: HSL recorded a record PAT of ₹1,125 Cr, a record EPS of ₹635.21, and a rise of 65% in net worth over two years, closing the chapter on the competitive trough of FY23 and embarking on the next phase of growth from a position of strength.

FY22 - Baseline

Market boom results in a period of strong performance. Low-cost brokers begin to gain traction.

FY23 - Trough

Zerodha & Groww client churn. Costs and credit losses increase. Cash decreases.

FY24 - Pivot

Launch of HDFC SKY. Expansion of MTF book as a response to competition. Income growth accelerates.

FY25 - Record

Record PAT of ₹1,125 Cr. SKY grows. Credit losses near zero. Transformation complete

HSL follows a "platform for every segment" strategy through its complex and differentiated offering in four unique verticals. This is in recognition that "one size fits all" is an old concept in a maturing market. Together, they cover the entire wealth spectrum in India, from a ₹5,000 SIP to a ₹50 Cr+ family office.

RETAIL - MASS MARKET

Discount broking platform for Gen Z and millennials through a mobile-first platform. Zero brokerage on ETFs and competitive fees. Designed for the "value and control" philosophy of the younger generation. Key growth engine for acquiring new clients in the market.

RETAIL - ADVISORY

RM-managed app providing a "human plus digital" experience. Backed by 1,500+ Relationship Managers, it serves 1.65 million active clients with curated advice driven by research. A platform that closes the gap between digital and professional advice.

WEALTH — ULTRA-HNI (₹50 CR+)

Launched October 2024. Bespoke platform for UHNIs, family offices, and corporate treasuries with assets above ₹50 Cr. Utilizes the PROSPr framework – a commission-free and arm’s length advisory methodology that delivers fiduciary integrity. Present in 145+ cities.

INSTITUTIONAL — GLOBAL RESEARCH

The intellectual engine of the firm. Covers 250+ stocks with a growth rate of 10%. Achieved 30% YoY revenue growth in the secondary market – a 6x outperformance of the Nifty 50’s 5%. Has a chaperone agreement with New York-based Auerbach Grayson.

FY25 marks a significant year in terms of operating leverage for HSL, as it recorded record revenues and profits, indicating capital-efficient scalability along with a revenue model that has become more de-risked to market cycles on a year-by-year basis.

HDFC Securities began FY21 as a simple fee-based broker. It is concluding FY25 as a diversified financial institution with a lending business. The transition between the two states has not been smooth. However, the destination is worth the turbulence.

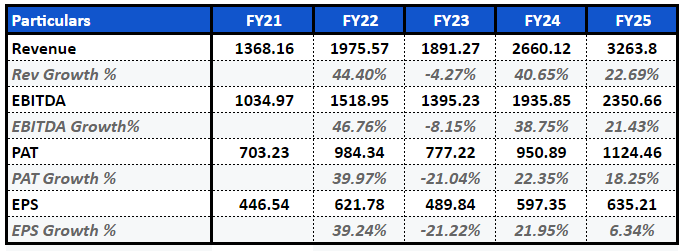

Revenue expanded from ₹1,368 crores in FY21 to ₹3,264 crores in FY25, though not always smoothly. While FY22’s 44% growth was simply market tailwind, where all brokers benefited from the post-COVID retail investing boom, FY23’s 4.27% decline was a structural issue, where discount brokers were taking active client share even while the market was rising. FY24’s strong 40.65% growth was clearly driven by the MTF lending business and HDFC SKY finally kicking in, while FY25’s solid 22.69% growth simply confirmed that the new, diversified revenue model had taken hold.

The story told by EBITDA and PAT is one of strength in FY22, pain in FY23, and a gradual climb from FY24-25. The fall of PAT by 21% in FY23 was not a market issue; it was an investment in technology, relationship managers, and lending infrastructure that had not yet paid off. PAT in FY25 was a record ₹1,124 crores, vindicating the investment. The only constant is that PAT growth was always slower than revenue growth, a clear indicator of finance cost pressure from the MTF book.

EPS reached a high of ₹622 in FY22, plummeted to ₹490 in FY23, and then recovered to a new all-time high of ₹635 in FY25. The low growth of 6.34% in EPS in FY25, despite 18% growth in PAT, is because of the issue of fresh equity shares in FY24, where there was a dilution of earnings per share, as fresh shares were issued to expand the balance sheet.

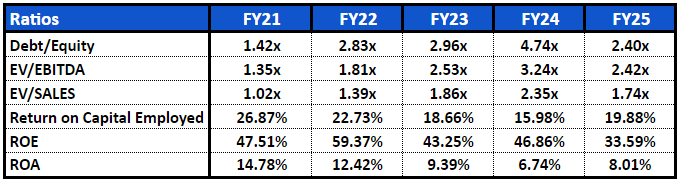

Debt/Equity ratio moved from 1.42x to a high of 4.74x in FY24, only to correct to 2.40x in FY25 – the story of leveraging the balance sheet to support the MTF book, followed by a sharp deleveraging as interest rates came down.

ROCE and ROE have both declined from their highs in FY21-22, but for obvious reasons – the massive rights issue increased the equity base, while capital was heavily invested in the MTF book and technology, causing these metrics to dip. The uptick in both these metrics in FY25 is a testament that these are now earning their keep.

A five-year increase in EV/EBITDA from 1.35x to 2.42x shows the market’s steady re-rating of this company – investors are now willing to pay more for every rupee of operating profit, a testament to the new business model.

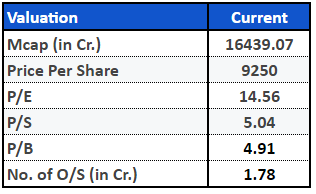

Currently, the stock is trading at a price of ₹9,250 per share, with a market capitalization of ₹16,439 crores. At a PE of 14.56x and PB of 4.91x, while growth is clearly priced, there is scope for appreciation if wealth advisory services and MTF services compound further.

HDFC Securities has had a difficult FY23, a transitional FY24, and a rewarding FY25. They have put off short-term efficiency to create a lending business, two digital platforms, and a wealth advisory vertical at the same time. This has resulted in squeezed margins for two years before recording record profits in FY25. The company that exists today, which is larger, more leveraged, more diversified, is fundamentally more capable than the company that existed in FY21. What the market is still trying to answer is whether the next phase of growth justifies the current price.

Assumptions

Overall:

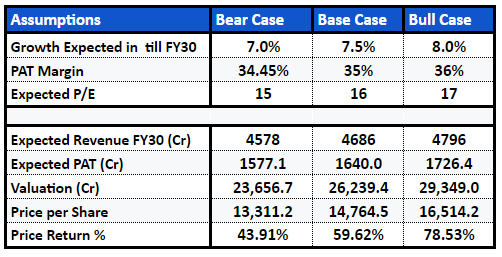

Even in the most conservative case, the model implies nearly 44% upside in the next five years, indicating a margin of safety in the current price. The bull case of a 78.5% return in six years implies a CAGR of 10-11%, which is low but believable for a financial services firm in a structurally growing market.

There are no aggressive assumptions underlying the forecast, only industry growth rates, improving but believable margins, and conservative valuation multiples. The investment case is straightforward: as the financialization story in India continues to evolve, HDFC Securities, with its MTF business, wealth vertical, and technology-enabled offerings, is poised to continue growing steadily and profitably through the decade, with the current price not fully reflecting the upside.

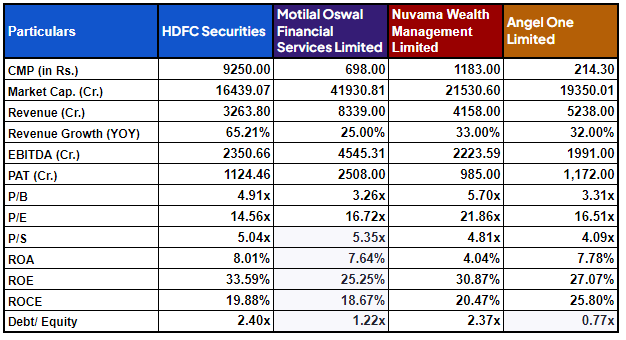

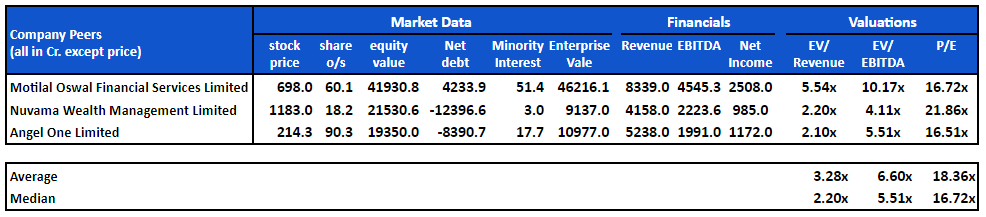

HSL is benchmarked against three listed peers: Motilal Oswal Financial Services, a full-service business; Nuvama Wealth Management, a capital-light advisory business; and Angel One, a mass-market discount business, which have structurally different business models.

Key Observation: HSL has the lowest P/E in the peer group (14.56x vs peer average ~18x) despite posting the highest revenue growth (65.2% YoY) and the highest ROE (33.59%). Motilal Oswal - the closest comparable - trades at 16.72x EV/Revenue 5.5x vs HSL's implied peer-average multiple of 3.3x, suggesting HSL may be modestly undervalued on a quality-adjusted basis.

The three peers have vastly different multiples, and it’s more important to understand why than what the actual numbers are.

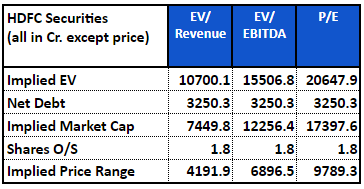

The ₹4,192 floor is almost certainly an underestimate. It's based on an EV/Revenue multiple that's been dragged down by Nuvama and Angel One's business models. If we simply use the Motilal Oswal multiple of 5.54x, the implied valuation based on the EV/Revenue metric will jump substantially and much more closely approximate the EV/EBITDA-based valuation of ₹6,897.

The P/E-based valuation of ₹9,789 represents the ceiling. And at the current price of ₹9,250 per share at HDFC Securities, the company is essentially trading at the upper limit of the valuation range based on its peers’ valuations.

On a purely peer average-based valuation metric, HDFC Securities is fully valued at the current price of ₹9,250. On a quality-adjusted valuation metric – taking into account the reality that the company's comparable is Motilal Oswal and not discount brokers – the company is essentially fair to slightly undervalued. The midpoint of the EV/EBITDA valuation band of ₹6,897 is almost certainly an underestimate of the company's intrinsic valuation given its superior parentage and its rapidly growing wealth advisory business. The investor is essentially buying a business that's more similar to Motilal Oswal than Angel One – and yet, that's a business that still holds up by

Three structural forces are converging to create a generational tailwind for HSL over the next decade, underpinned by India's macroeconomic resilience and a fundamental shift in household savings behavior.

(1) MTF book of ₹7,285 Cr untested in a sharp market correction – collateral quality must be high.

(2) Finance costs have increased by 403% as MTF books have grown – interest rate sensitivity is real.

(3) One-time fair value gains of ₹84 Cr added to FY25 PAT by ~7% – recurring earnings power is slightly lower.

(4) High payout ratio of ~80% constrains ability to reinvest in a heavy capex period.

(5) Operating leverage remains negative as investment costs in the platform continue to rise.

HDFC Securities enters FY26 as a fundamentally different company from the one that stumbled in FY23. What appeared to be a business in terminal decline, losing clients to Zerodha, seeing margins compress, and experiencing a cratering of cash flows, was in fact a company in the midst of the most transformative reinvention in its 25-year history.

The compelling proposition of HSL is the coming together of three key factors: a structurally positive macro backdrop (India's equity participation at 7% can only go one way), a business architecture that is unmatched by any competitor (a full-stack ecosystem from a ₹5,000 SIP to a ₹50 Cr family office, powered by India's most trusted finance brand), and a pending operating leverage inflection that is already apparent but yet to be fully reflected in current valuation.

At a multiple of 14.56x, the lowest in the peer group but with the highest revenue growth and ROE, HSL is fair value to modestly undervalued from a quality perspective. For a long-term investor with a 3-5 year horizon, the base case generates a price return of 59.6% to a price of ₹14,765. This share is available with sharescart.

Independent Research Powered By - Actionable data