15 Days Price Change

Nikhil Singh

Nikhil Singh

I am a versatile professional known for my expertise as a technical analyst, insightful co... I am a versatile professional known for my expertise as a technical analyst, insightful contributions as a part-time investor, and creative talents as a content writer. With a strong background in finance, I seamlessly combine technical know-how and fundamental analysis in my role as a part-time investor. Read more

Summary

B9 Beverages, the company behind Bira 91, spent a decade proving that Indian drinkers would pay more for better beer. The brand worked. The balance sheet didn’t. With accumulated losses of ₹2,117.98 crore, a going-concern warning from its auditor, halted production, and a founder under pressure to step down, the company now faces a single defining question: whether a $132 million rescue package closes in time to prevent insolvency. This report examines the business, the numbers, and what either outcome means for unlisted equity holders.

B9 Beverages, the company behind Bira 91, carved out an unusual space in India's beer market when it launched in 2015. The pitch was straightforward: domestic lagers were cheap and forgettable, imported craft beers were expensive, and nothing sat in between.

Founder Ankur Jain came to that conclusion after returning to India in 2008. He'd studied computer science at the Illinois Institute of Technology, co-founded a healthcare startup in New York, and spent enough time around the American craft beer scene, especially Brooklyn Brewery, to notice what Indian drinkers didn't have access to. His first move was to import craft beers from Europe and the US. That model ran into friction on logistics and margins, and in May 2014 he switched to manufacturing instead. Bira 91 launched the following year.

The brand came out with a "Imagined in India, for the World" tagline, loud packaging, and a wider flavor range than most domestic competitors. It found its audience quickly among younger urban drinkers who wanted something other than a strong lager but weren't going to pay import prices for it.

B9 Beverages' early setup was genuinely odd for a startup. Bira 91's first batches were brewed in Belgium's Flanders region the company didn't have domestic infrastructure it trusted. Ingredients came from multiple countries: hops and malt from France and Bavaria, wheat from the Himalayas. The beer was brewed in Europe, then imported back into India to sell.

That worked for reputation. It didn't work financially. After a $1 million seed round from angel investors including Snapdeal's Kunal Bahl and Rohit Bansal and Zomato's Deepinder Goyal, B9 moved production to India. Its own domestic brewing facilities were operational by 2016, though it kept the international ingredient sourcing in place.

From there, the company moved quickly on several fronts at once. The beer lineup grew beyond White and Blonde Light, Strong, and an IPA joined the portfolio, the last of which was India's first locally brewed and bottled version of the style. International markets opened up around the same time: the US debut was at the Tribeca Film Festival in New York, with the UK, Singapore, Hong Kong, Thailand, and the UAE following. In November 2018, the company signed on as a global sponsor of the International Cricket Council, a significant spend that put the brand in front of cricket audiences across multiple countries. Kirin Holdings, the Japanese beverage company, then came in with $30 million, and returned later with a $70 million Series D $100 million combined by 2022.

B9 Beverages priced Bira 91 into a gap that was easy to see but hard to fill. Too expensive to compete directly with Kingfisher, too cheap to sit alongside imported craft beers that middle band is where the company has stayed.

The business runs across four areas.

Beer. The two main products are Bira 91 White, a wheat beer with citrus and coriander at 4% ABV, and Bira 91 Blonde, a Saaz-hopped craft lager at 4.9%. Most of the volume runs through those two. The rest of the lineup has grown out in different directions: Light for calorie-conscious drinkers, Strong (7% ABV) and Bira Boom Super Strong for the segment of the Indian market that prefers high-alcohol beer, Rise as a rice lager, a few cider variants, and Grizly Hard Seltzer Ale for the low-ABV, fruit-flavored crowd. The company has also put out carbonated mixers and cold brew coffee products that have nothing to do with beer but get the brand onto shelves it otherwise wouldn't reach.

Taprooms. Four locations two in Delhi NCR, two in Bengaluru sell direct and run weekly small-batch brews that function as informal product testing. The company acquired The Beer Cafe, a pub chain spread across multiple Indian cities, in an all-cash deal.

Draft. Convincing a venue to switch from bottles to tap has been one of the more effective things the company has done. B9 claims the switch increases a venue's Bira 91 sales by 25 times. The underlying logic is real even if the number is hard to verify independently: fresh beer, no packaging cost, and a tap handle that's visible every time someone walks up to the bar.

Merchandise. Branded growlers, glassware, apparel, and cricket-themed limited editions for Mumbai Indians and Delhi Capitals fans. It brings in some margin and keeps the name in front of people who aren't in a bar.

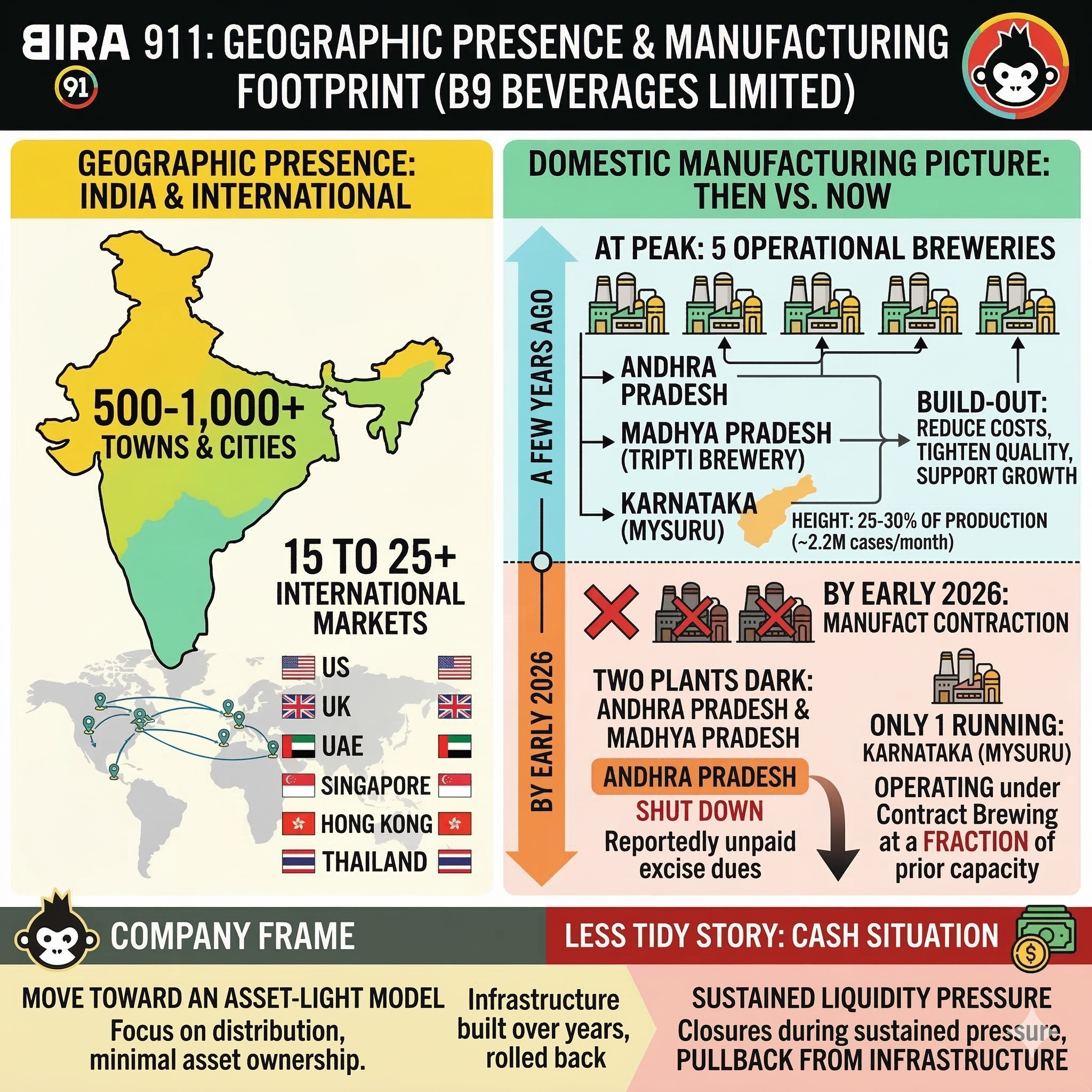

Bira 91 sells across somewhere between 500 and 1,000 towns and cities in India, and in 15 to 25 international markets the US, UK, UAE, Singapore, Hong Kong, and Thailand among them.

The domestic manufacturing picture looks very different now than it did a few years ago. At its peak, the company ran five breweries in India, with major facilities in Andhra Pradesh, Madhya Pradesh (Tripti Brewery), and Karnataka (Mysuru). The build-out was meant to reduce costs, tighten quality control, and support growth.

By early 2026, two of those plants had gone dark. The Andhra Pradesh facility which at its height handled 25 to 30 percent of total production, around 2.2 million cases a month shut down completely, reportedly because of unpaid excise dues. Madhya Pradesh followed. Mysuru is now the only plant running, and it's operating under a contract brewing arrangement at a fraction of prior capacity.

B9 has framed this as a move toward an asset-light model. The cash situation tells a less tidy story: the closures came during a period of sustained liquidity pressure, and the company has had to pull back from infrastructure it spent years building.

Bira 91 sells through four channels, and the mix matters.

Most volume moves through off-trade liquor vendors, supermarkets, specialty retail. That's true of the beer industry broadly; off-trade accounts for around 57% of global beer sales, and it's where Bira 91 does most of its business too.

On-trade is bars, restaurants, hotels, and pubs. The margins are better here, in part because of the draft tap push. Once a venue is serving Bira 91 on tap rather than from bottles, costs fall and volumes tend to go up.

International sales run through export, targeting the Indian diaspora and craft beer drinkers in markets like the US, UK, and UAE who want something outside their usual options.

The fourth channel is direct-to-consumer: the taprooms, The Beer Cafe network, online merchandise, and e-commerce. Smaller in scale, but it's where the company has the most control over the customer experience and the highest visibility into who's actually buying.

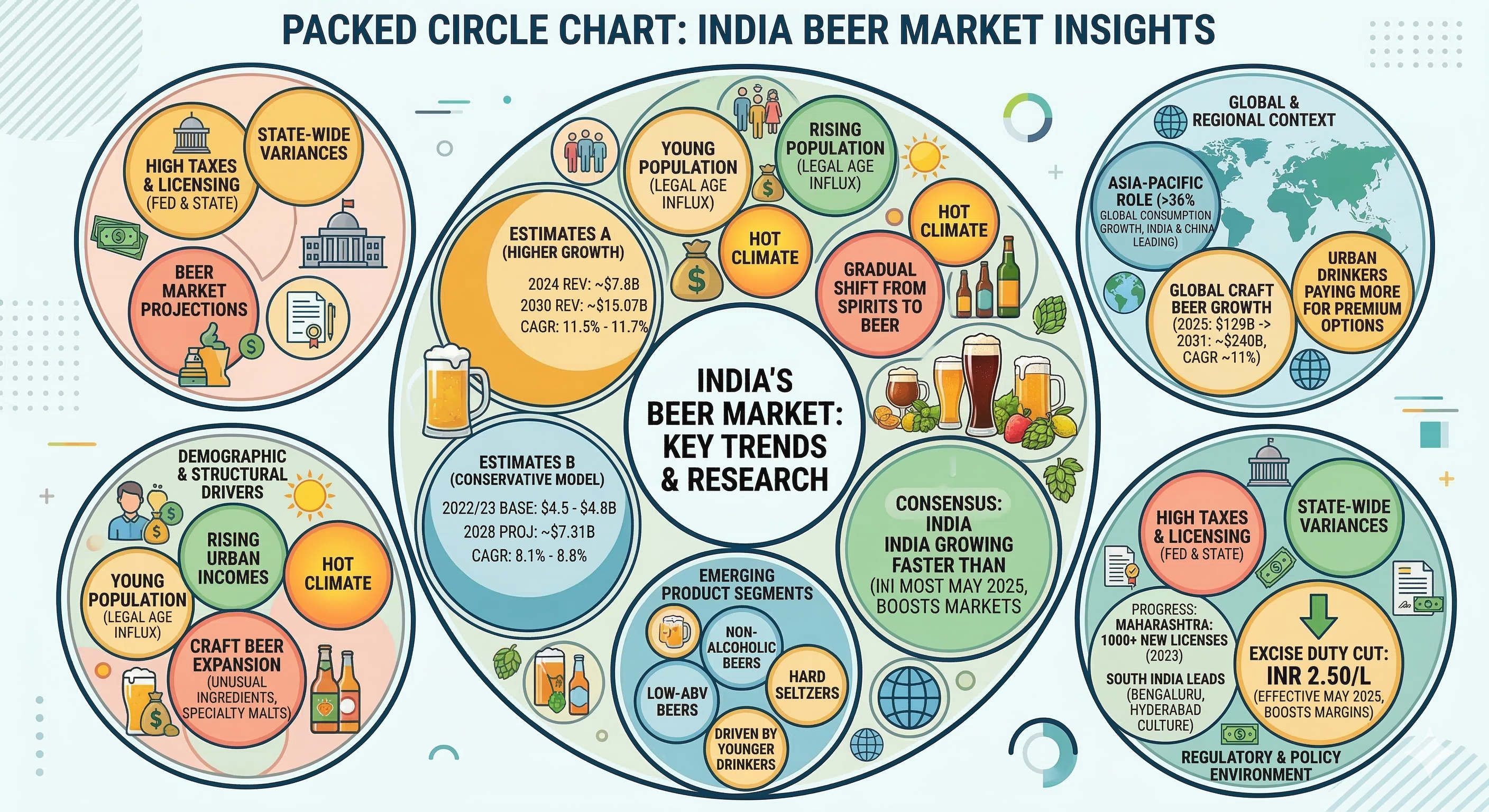

India's beer market projections vary quite a bit depending on the source. One set of estimates puts 2024 revenue at around $7.8 billion, with growth to $15.07 billion by 2030 a CAGR of 11.5% to 11.7%. More conservative models put the 2022/2023 base at $4.5 to $4.8 billion and project $7.31 billion by 2028, implying 8.1% to 8.8% annual growth. The numbers don't fully agree, but they point the same way: India is growing faster than most beer markets globally.

Asia-Pacific accounts for over 36% of projected global beer consumption growth, with India and China doing most of the heavy lifting. Craft beer, specifically, is expanding quickly worldwide from an estimated $129 billion in 2025 to around $240 billion by 2031, at roughly 11% annually.

India's beer market has a few things going for it structurally.

The population skews young, and a significant number of people cross the legal drinking age each year. Incomes are rising in cities, the climate is hot, and consumption is gradually tilting away from traditional spirits toward beer not dramatically, but consistently.

The other shift is what people are buying within the beer category. Cheap mass-market lagers are losing ground to craft and premium options. Urban drinkers are paying more for unusual ingredients specific hop varieties, fruit-forward ales, specialty malts and the segment is expanding fast enough that most major players have adjusted their portfolios accordingly.

Format is changing too. Low-ABV and non-alcoholic beers have moved from a niche offering to a real part of the market, pushed along by younger drinkers who want to drink more carefully. Hard seltzers are part of the same trend.

Regulation is harder to summarize cleanly. Alcohol taxes at the federal and state level are still high, and licensing rules vary wildly by state. But there's movement. Maharashtra issued more than 1,000 new liquor licenses in 2023. South India Bengaluru and Hyderabad especially runs ahead of the rest of the country on beer culture and has a regulatory environment that reflects that. The Ministry of Finance announced a cut of INR 2.50 per liter in excise duty on beer, effective May 2025, which should help margins across the industry.

Indian beer is effectively a three-company market. United Breweries, Carlsberg, and AB InBev have held dominant positions for years, and the structural advantages that keep them there distribution depth, manufacturing scale, balance sheet size are not easy to close.

UBL, majority-owned by Heineken, is the clear leader with around 50% market share. Kingfisher is everywhere, and UBL's distribution network reflects decades of investment across the country.

AB InBev brings Budweiser, Corona, and Hoegaarden into the market and has been responding to the craft segment rather than ignoring it. Seven Rivers is its localized craft play, and the company recently bought a 26% stake in Navin's Maltings & Breweries for roughly INR 2,500 crore ($330 million) to get more control over its local supply chain.

Carlsberg's strength is in strong beer Carlsberg Elephant and Tuborg are the main brands. It recently signed a deal with IRCTC to sell beer on select train routes, which opens up a channel that most competitors can't replicate easily.

Bira 91 has carved out around 5% share in major metros, which is a real accomplishment given the competition. But it's working with a fraction of the resources the incumbents have. That forces a particular kind of strategy: high marketing spend, frequent new products, and constant pressure to stay relevant while the bigger players try to absorb the craft trend themselves. It's not an easy position.

Ankur Jain founded B9 Beverages and remains its CEO. He studied computer science at the Illinois Institute of Technology, spent time co-founding a healthcare startup in New York, and came back to India with a particular idea of what the beer market was missing. His early strategy leaned heavily on venture capital, fast expansion, and marketing spend the kind of approach that builds a brand quickly but doesn't always build the structures underneath it.

The board composition reflected that. For years it was tightly held: Jain, his wife, and his mother. Useful for moving fast in the startup phase. Less useful when the company started facing the kind of financial and governance scrutiny that comes with institutional investors and IPO ambitions.

The restructuring started in mid-to-late 2025. Vikram Qanungo came in as CFO replacing Meghna Agarwal, who had held the role through the growth years with a focus on cost discipline and stabilizing the company's finances. Deepak Sinha joined as VP of Brand and Innovation; he has more than a decade in the drinks industry and ran Bira 91's US expansion. Dr. Manoj Mishra took the VP of Manufacturing role to handle the supply chain and manage the ongoing shift to contract brewing.

Two independent directors also joined the board: Manoj Kohli, who previously led SoftBank India, and Bharat Anand, a partner at Khaitan & Co. Adding independent directors after years of tight promoter control is the kind of change that doesn't fix underlying problems on its own, but it's the visible step companies take when they need to show stakeholders that something is changing.

By early 2026, B9 Beverages had stopped paying its employees. Salaries were outstanding for up to six months. The company had also failed for over a year to deposit Tax Deducted at Source and Provident Fund contributions money withheld from employee paychecks that was legally required to be passed on to the government.

More than 250 current and former employees responded by formally petitioning the board and the company's major institutional investors Kirin Holdings and Peak XV Partners among them demanding Ankur Jain's removal. The petition named governance failures, a lack of transparency, deteriorating finances, creditor lawsuits, and unpaid vendor bills.

Kirin and Peak XV had their own concerns about where the company was heading. The employee petition made the situation public and harder to manage quietly. Any fresh emergency capital, investors made clear, was conditional on bringing in external professional management.

By March 2026, Jain had agreed in principle to step down and give up operational control.

B9 Beverages has raised somewhere between $350 million and $457 million across 17 to 20 funding rounds, with more than 211 investors on the cap table. Early backing came primarily from venture capital; over time, the mix shifted toward strategic corporate investors. The ownership structure below reflects where things stood before the crisis that emerged in early 2026.

| Shareholder / Entity | Estimated Stake (%) | Strategic Role / Background |

| Peak XV Partners (formerly Sequoia Capital India) | 24.83% | Largest external institutional stakeholder; early-stage venture backer providing aggressive growth capital. |

| Ankur Jain & Promoter Group | 17.80% - 24.43% | Founder and family. Stake has been heavily diluted over successive rounds. Promoter shares were recently invoked by lenders due to mounting personal liabilities. |

| Kirin Holdings | 20.10% - 21.25% | Japanese beverage conglomerate. Largest strategic partner providing deep R&D, sustainability frameworks, and substantial capital injections. |

| Day1 Advisors Pvt Ltd / Other VC | ~16.29% | Early-stage investors and strategic advisors. |

| Tiger Pacific Capital | ~4.00% | New York-based investment fund; recent pre-IPO crossover investor. |

| Sofina SA & Sixth Sense Ventures | Minority | Belgian family-owned investment firm and Indian consumer-focused venture fund providing mid-to-late stage capital. |

The funding timeline over the past three years tracks a company moving from expansion mode to crisis management.

In November 2022, Kirin Holdings invested $70 million through compulsory convertible preference shares at Rs 718 per share, taking its stake from around 10% to over 20%. Kirin's domestic beer sales in Japan have been under pressure for years, and India's growth numbers made the bet look reasonable. The money was meant to go toward production capacity, international distribution, and R&D.

In 2023 and 2024, B9 raised $10 million from MUFG Bank and $25 million from Tiger Pacific Capital the Tiger Pacific round implying a pre-money valuation of around $600 million. Both were framed as pre-IPO rounds. Alongside those, the company raised roughly ₹100 crore ($12 million) through non-convertible debentures and another $25 million in external commercial borrowing from Kirin, primarily to cover working capital and settle debt from The Beer Cafe acquisition.

Then things deteriorated. By March 2026, BlackRock had walked away from a deal that would have provided ₹500 crore in promoter debt. The company is now in advanced talks for a $132 million rescue package $50 million in equity, $82 million in structured credit with Global Emerging Markets cited as the leading candidate. That deal, or something like it, is what stands between B9 and insolvency.

Holding a challenger position in Indian beer means competing against companies with decades of distribution infrastructure, manufacturing scale, and balance sheets that absorb losses Bira 91 cannot. The comparison isn't flattering, and it explains a lot about how the company got where it is.

Comparative Analysis with Industry Competitors

| Metric | B9 Beverages Limited (Bira 91) | United Breweries Limited (UBL / Heineken) | Anheuser-Busch InBev (India) |

| Market Share (India) | ~5% (Concentrated in targeted urban regions) | ~50% (Dominant national leader) | Top 3 National Player; strong premium segment hold. |

| FY24 Financial Profile | ₹421 Cr Net Rev; Loss of ₹749 Cr; Negative Net Worth | Highly profitable, multibillion-dollar scale; EV/EBITDA of ~59.3x - 60x. | Highly profitable; massive internal cash generation. |

| Manufacturing Model | Asset-light / Hybrid (Shrinking capacity, heavily reliant on contract brewing) | Massive scale; highly integrated national network of proprietary breweries. | Deeply integrated; recently acquired massive local malting assets. |

| Brand & Distribution Strategy | Craft, Millennial-focused, high marketing burn, agile innovation | Broad demographic appeal, entrenched brand equity (Kingfisher), 93% domestic sourcing. | Global brand leverage (Budweiser, Corona), local craft defense (Seven Rivers). |

| Liquidity & Debt Risk | Severe distress; Debt ~₹1,000 Cr; Going-concern warning issued | Robust balance sheet; Strong liquidity;AA+ credit rating. | Fortress balance sheet. |

Bira 91's real advantages over the incumbents are speed and cultural instinct. UBL runs on Heineken's supply chain and distribution scale reliable, efficient, and not particularly flexible. Bira 91 put out Mango Lassi ale, Kokum Sour, and Tamarind Chutney Dubbel. Those products exist because someone made a fast call, not because a global portfolio committee approved them. The taprooms and The Beer Cafe give the company something distribution-only players don't have:

Direct contact with customers and a low-stakes place to test ideas before committing to them at scale.

What Bira 91 doesn't have is the financial cushion that makes all of that sustainable when things go wrong. UBL and AB InBev can absorb a regulatory shock or a bad commodity year without restructuring. Bira 91 couldn't absorb several of them in a row while also running on external capital. The growth was real, but it was funded by investors, and once the funding environment tightened, there wasn't enough internal cash generation to hold things together.

Figures ( in cr )

P&L Statement

| Metric | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|

| Revenue | 428.2 | 717.77 | 824.32 | 638 |

| Cost of Material Consumed | 87.17 | 164.4 | 265.38 | 201 |

| Change in Inventory | 4.48 | 68.44 | -26.27 | 33 |

| Gross Margins | 79.64 | 77.1 | 67.81 | 68.5 |

| Employee Benefit Expenses | 62.96 | 90.71 | 114.98 | 182 |

| Other Expenses | 378.01 | 567.45 | 710.29 | 696 |

| EBITDA | -104.42 | -173.23 | -240.06 | -474 |

| OPM | -24.39 | -24.13 | -29.12 | -74.29 |

| Other Income | 34.61 | 15.98 | 24.39 | 30 |

| Finance Cost | 76.2 | 87.72 | 96.59 | 160 |

| D&A | 74.24 | 90.09 | 121.41 | 144 |

| EBIT | -178.66 | -263.32 | -361.47 | -618 |

| EBIT Margins | -41.72 | -36.69 | -43.85 | -96.87 |

| PBT | -211.28 | -335.07 | -433.69 | -749 |

| PBT Margins | -49.34 | -46.68 | -52.61 | -117.4 |

| Tax | 0 | 0 | 11.78 | 0 |

| PAT | -211.28 | -335.07 | -445.47 | -749 |

| NPM | -49.34 | -46.68 | -54.04 | -117.4 |

| EPS | -159.22 | -69.51 | -79.56 | -125.04 |

Financial Ratios

| Metric | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|

| Operating Profit Margin | -24.39 | -24.13 | -29.12 | -74.29 |

| Net Profit Margin | -49.34 | -46.68 | -54.04 | -117.4 |

| Earnings Per Share (Diluted) | -159.22 | -69.51 | -79.56 | -125.04 |

Balance Sheet – Assets

| Assets | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|

| Fixed Assets | 76.36 | 84.45 | 431.45 | 507 |

| CWIP | 7.01 | 7.16 | 15.16 | 29 |

| Investments | 35.52 | 54.7 | 1.1 | 1 |

| Trade Receivables | 124.53 | 126.68 | 169.68 | 108 |

| Inventory | 99.25 | 74.05 | 164.2 | 108 |

| Other Assets | 578.2 | 645.76 | 492.54 | 397 |

| Total Assets | 920.87 | 992.8 | 1274.13 | 1150 |

Balance Sheet – Liabilities

| Liabilities | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|

| Share Capital | 13.27 | 48.206 | 55.99 | 59.9 |

| FV | 10 | 10 | 10 | 10 |

| Reserves | 28.07 | -72 | 106 | -422 |

| Borrowings | 246.94 | 346.71 | 314.6 | 594 |

| Trade Payables | 138.07 | 187.26 | 290.05 | 438 |

| Other Liabilities | 494.52 | 482.45 | 507.63 | 558.1 |

| Total Liabilities | 920.87 | 992.63 | 1274.27 | 1228 |

Cash Flow Statement

| Metric | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|

| PBT | -211.28 | -335.07 | -433.69 | -749 |

| OPBWC | -75.43 | -138.64 | -198.35 | -437 |

| Change in Receivables | -36.56 | -7.7 | -60.75 | 37 |

| Change in Inventories | -19.65 | 17.37 | -103.91 | 56 |

| Change in Payables | 45.44 | 17.68 | 138.6 | 241 |

| Other Changes | -36.09 | -68.5 | -59.43 | 41 |

| Working Capital Change | -46.86 | -41.15 | -85.49 | 375 |

| Cash Generated From Operations | -122.29 | -179.79 | -283.84 | -62 |

| Tax | 0.81 | 0.06 | 0.63 | -3 |

| Cash Flow From Operations | -121.48 | -179.73 | -283.21 | -65 |

| Purchase of PPE | -30.02 | -42.3 | -128.26 | -148 |

| Sale of PPE | 0 | 0 | 0 | 0 |

| Cash Flow From Investment | -66.04 | -57.24 | -227.18 | -189 |

| Borrowing | 79.85 | 96.34 | -25.09 | 181 |

| Dividend | 0 | 0 | 0 | 0 |

| Equity | 5.6 | 0 | 609.02 | 76 |

| Others From Financing | 102.8 | 134.71 | -47.57 | -79 |

| Cash Flow from Financing | 188.25 | 231.05 | 536.36 | 178 |

| Net Cash Generated | 0.73 | -5.92 | 25.97 | -76 |

| Cash at the Start | 12.07 | 12.8 | 8.83 | 24 |

| Cash at the End | 12.8 | 6.88 | 34.8 | -52 |

By March 2024, accumulated losses had hit ₹2,117.98 crore enough to wipe out the company's net worth completely. By late 2024, liabilities exceeded assets by around ₹600 crore. Total debt was approximately ₹1,000 crore, and operating cash flow came in at -₹42.26 crore for FY24. The statutory auditor, Walker Chandiok & Co., noted all of this in the FY24 annual report and flagged unmitigated market, credit, and liquidity risk as a threat to the company's status as a going concern. That's auditor language for: we're not sure this business can keep running.

An asset turnover ratio of around 0.66, based on FY23 data, reflects a manufacturing setup that was too capital-heavy relative to the revenue it was producing. The shift to contract brewing is partly an attempt to correct that.

Some of the more recent figures are more encouraging. Q3 FY25 showed 42% year-on-year revenue growth, with quarterly revenue reaching ₹67 crore and volumes up 50%. Variable margins reportedly jumped from around 25% to over 43%, driven by a BCG-assisted supply chain restructuring and the lower overhead of contract manufacturing. EBITDA losses for H1 FY25 came in at -₹111 crore, compared to -₹153 crore in H1 FY24 a 28% improvement, achieved through cost cuts, layoffs, and plant closures.

The improvement is real. It's also coming off a base that was bad enough that the company is still in serious trouble.

B9 Beverages isn't publicly listed, so there's no clean way to value it. The best available reference points are the most recent institutional funding round and grey market share activity and they're not saying the same thing.

In early 2024, Tiger Pacific Capital paid $25 million for roughly 4% of the company. That puts the pre-money valuation at $600 million (around ₹4,980 crore) and post-money at $625 million slightly above the $540–$550 million implied by Kirin's 2022 Series D investment.

In the unlisted grey market, shares with ISIN INE833U01014 and a face value of ₹10 are being quoted across a wide range: ₹110.25 at the low end, ₹471 in the middle, and ₹615 at the top. The Tiger Pacific deal implied something close to that upper figure. The ₹110.25 quotes reflect retail sellers getting out at whatever price they can amid the liquidity and leadership crisis that accelerated through 2025 and into 2026. A spread of over ₹500 between the lowest and highest quotes on the same share isn't normal market volatility it reflects genuine uncertainty about whether the company can be turned around.

The risks

Cash is the immediate threat. Net worth has been wiped out, working capital is gone, and two of the three main plants are no longer running. Without the $132 million rescue package, the company runs out of road.

Regulation is a longer-term vulnerability that didn't cause this crisis but has made it worse. Alcohol in India is governed state by state, and the rules are inconsistent and heavily enforced. A label change, a delayed excise payment, or a compliance lapse can freeze inventory and cut off revenue fast. The ₹80 crore write-off shows what that looks like in practice.

The workforce damage is harder to quantify but probably slower to fix than the finances. Six months of unpaid salaries, over a year of withheld statutory contributions, and a public employee petition against the founder don't get resolved by a leadership change announcement. Vendors and staff both have reasons to be cautious about trusting the company again, and rebuilding that takes time a turnaround plan rarely accounts for.

The openings

Jain stepping back and independent directors coming onto the board removes a specific objection that institutional investors had. Manoj Kohli and Bharat Anand bring credibility that makes conversations with lenders and equity investors easier than they were six months ago.

Closing the Andhra plant and consolidating production at Mysuru under a contract brewing model converts fixed manufacturing costs into variable ones. That's not a fix by itself, but it lowers the breakeven point and reduces the exposure that comes with running underutilized owned infrastructure.

Summer is also approaching. Beer demand in India peaks in the warmer months, and Bira 91 still has meaningful brand recognition in urban markets. If capital arrives before Q1 FY27, the taprooms and Beer Cafe network give the company a faster path back to volume than it would have starting from nothing.

Bira 91 changed what Indian beer looked like. That's not nothing. Ten years ago, the choice in most urban bars was between cheap domestic lagers and expensive imports. Bira 91 sat in the middle and made that position work on product, on branding, and on timing. The brand built real loyalty with a generation of drinkers who hadn't been particularly loyal to anything before it. What it didn't build was the financial foundation to survive a bad stretch. The governance was too concentrated, the cash burn was too high, and when regulatory and liquidity shocks hit in sequence, there wasn't enough resilience in the structure to absorb them. As of March 2026, the company has better management than it did a year ago, a leaner cost base, and a credible if painful path toward operational sustainability. Whether any of that matters depends on whether the $132 million rescue financing closes in time. If it does and production restarts before peak summer demand, the brand is recoverable. If it doesn't, ten years of building something distinctive ends in insolvency court which would be an avoidable outcome, and that's the part worth remembering.

Independent Research Powered By - Actionable data