15 Days Price Change

Nikhil Singh

Nikhil Singh

I am a versatile professional known for my expertise as a technical analyst, insightful co... I am a versatile professional known for my expertise as a technical analyst, insightful contributions as a part-time investor, and creative talents as a content writer. With a strong background in finance, I seamlessly combine technical know-how and fundamental analysis in my role as a part-time investor. Read more

Summary

This article explains that “Kurlon unlisted shares” usually refer to Kanara Consumer Products (KCPL), which is no longer the Kurlon mattress business. The actual Kurlon operations were sold and merged into listed Sheela Foam, while KCPL is now mainly a promoter-controlled holding/investment company with high price dispersion and no clear IPO timeline.

The most important thing any investor should understand is this. Kurlon unlisted shares today are not the same as the Kurlon mattress business. Kanara Consumer Products Ltd or KCPL is now a different company. This company was started in 1962 by the Pai family and was earlier known as Kurlon Limited. In June 2023 it changed its name to Kanara Consumer Products Ltd. Just about a month later it sold its main mattress business Kurlon Enterprise Ltd to Sheela Foam Ltd.

The deal was valued at around ₹2,150 crore. After that Kurlon Enterprise Ltd was merged into Sheela Foam.

This got approval in September 2025 and by April 2026 the new shares started trading. So today the full Kurlon business including brand factories dealers and revenue is inside Sheela Foam which is a listed company. Now what is being sold today as Kurlon or Kanara Consumer Products unlisted shares is something else. It is basically the remaining holding company of the Pai family. This company has around 96.43 percent promoter holding. It has very low debt and about ₹107 crore revenue. Now it is moving into areas like real estate ayurveda and consulting. There is no DRHP filed and there is no clear IPO timeline. So the investment story here is very different from what most retail investors assume. This report tries to clear that confusion. It explains the four different entities involved. It shows the financials of both KCPL and the earlier mattress business. It also compares the Indian mattress market and Sheela Foam which is now the closest proxy to Kurlon.

And it gives a clear view on whether this unlisted share opportunity makes sense or not. Looking at the history.

Kanara Consumer Products Ltd was started on 9 February 1962 in Bangalore as Karnataka Coir Products Ltd.

Over time the company changed its name multiple times.

In 1980 it became Karnataka Consumer Products Ltd.

In 1995 it became Kurl On Limited.

And finally in June 2023 it became Kanara Consumer Products Ltd. This last change happened just before selling the mattress business. There are four different entities in this whole structure.

Many people mix them up which creates confusion.

Understanding this properly is very important before making any investment decision.

The corporate chain has four entities that retail commentary regularly conflates, and getting them straight is essential.

| Entity | CIN | Role | Status today |

|---|---|---|---|

| Kanara Consumer Products Ltd (KCPL) | U68100KA1962PLC001443 | Historic Pai-family parent. Held 88.48% of KEL directly. Renamed 14 June 2023. | Independent unlisted public company. Pivoting to real estate + ayurveda. |

| Kurlon Enterprise Ltd (KEL) | U36101MH2011PLC222657 | Operating subsidiary that received the mattress business via Business Transfer in 2014. | Ceased to exist. Merged into Sheela Foam in September 2025. |

| Kurlon Trading and Invest Mgmt Pvt Ltd (KTIMPL) | KCPL's wholly-owned subsidiary; held 6.19% of KEL. | Renamed Kanara Consulting and Service Management Pvt Ltd. | |

| Sheela Foam Ltd (SFL) | L74899MH1971PLC427835 | Acquirer of KEL. NSE: SFL. Sleepwell parent. | Now also owns the entire Kurlon brand, factories, and dealer network. |

KCPL which is Kanara Consumer Products Ltd is the old holding company of the Pai family. It started in Bangalore on 9 February 1962 as Karnataka Coir Products Ltd. Over time it changed names a couple of times and became Kurl On Limited in 1995. Then in June 2023 it took its current name Kanara Consumer Products Ltd. One key thing happened earlier in 2014. KCPL separated its full mattress foam and furniture business into another company. This was done through a business transfer deal. KCPL kept assets like land buildings and the Gwalior plant. But the actual operating business was moved to KEL. KEL which is Kurlon Enterprise Ltd was the main operating company. All factories brand and dealer network were under KEL.

KCPL directly held about 88.48 percent in KEL. Another 6.19 percent was held through a group company which KCPL fully owned. So total control of the Pai family was around 94.66 percent. Sheela Foam Ltd is a listed company from Mumbai.

It owns the Sleepwell brand and is promoted by the Rahul Gautam family. In July 2023 Sheela Foam board approved the deal to buy KEL. The agreed price was ₹588.20 per share of KEL. This valued the full company at around ₹2,150 crore.

The main stake purchase closed in October 2023. Sheela Foam paid around ₹1,940 crore in cash initially. After that it kept buying more shares till March 2024 and reached about 97.43 percent ownership. Total money spent was close to ₹2,000 crore.

To fund this deal the company raised money through different routes. Around ₹1,500 crore came from QIP. Around ₹600 crore came from bonds. Rest came from internal cash.

There was also another deal around the same time. Sheela Foam bought 35 percent in Furlenco in August 2023. Later this stake increased to about 43.89 percent.

After the acquisition the merger process started. In March 2024 Sheela Foam approved a plan to merge multiple subsidiaries into KEL and then merge KEL itself into Sheela Foam.

As part of this deal KEL shareholders received 52 shares of Sheela Foam for every 100 shares they held.

The merger got approval in September 2025. The record date was January 2026. New shares were issued in February 2026 and started trading in April 2026. After this KEL no longer exists as a separate company. Now coming back to KCPL.

KCPL was not part of this merger at all.

It is still controlled by the Pai family with around 96.43 percent holding after a buyback. It has no connection left with the mattress business. In November 2023 the company changed its business focus. It updated its objectives to enter real estate and ayurveda products. This is being done through a subsidiary called Manipal Natural Pvt Ltd. In 2026 an EGM also approved merging some of its subsidiaries into the main company. At this stage KCPL is a completely different business compared to what Kurlon used to be.

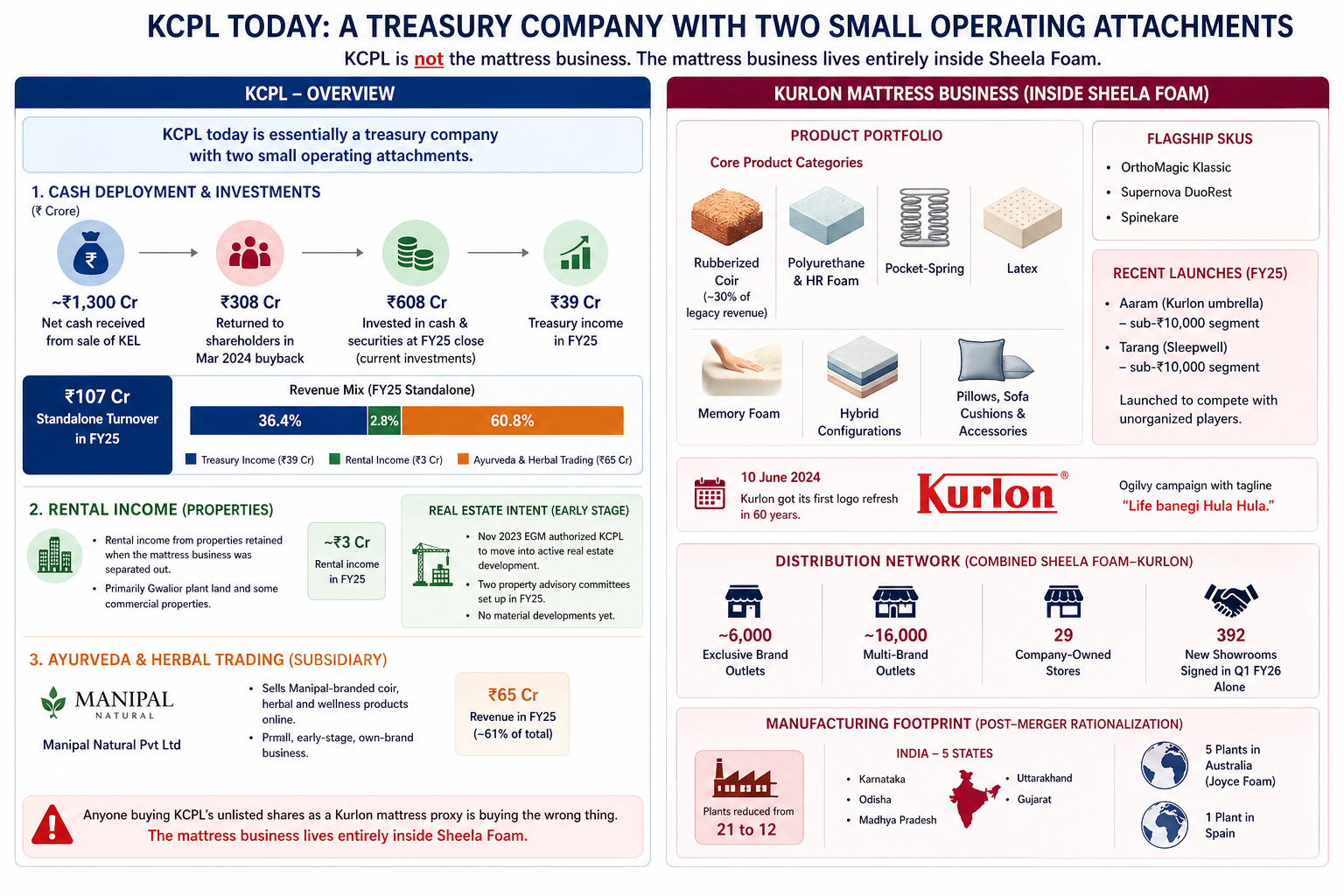

KCPL today is mostly a treasury type company with a couple of small business activities. After selling KEL it received around ₹1,300 crore in cash. Out of this ₹308 crore was returned to shareholders through a buyback in March 2024.

The remaining ₹608 crore is sitting as investments at the end of FY25. This money is parked in cash and securities and earns interest and treasury income. This treasury income alone gave around ₹39 crore in FY25. That makes it the biggest contributor to the total ₹107 crore revenue of the company.

The second income source is rent.This comes from properties that KCPL kept when the mattress business was separated.

Mainly the Gwalior plant land and some commercial properties. This gives roughly ₹3 crore per year. In November 2023 the company also got approval to enter real estate development. In FY25 it created two property advisory committees.

So there is some intent to grow here but nothing major has happened yet. The third area is ayurveda and herbal products.

This is done through its subsidiary Manipal Natural Pvt Ltd. It sells coir based products herbal items and wellness products online.

This business is still small and at an early stage. So if someone is buying KCPL unlisted shares thinking it represents the Kurlon mattress business that assumption is wrong. The mattress business is now fully part of Sheela Foam.

Now looking at what that actual mattress business includes. It has a wide range of products like rubberized coir which Kurlon started back in 1965. This still forms a big part of its revenue. Along with that there are foam mattresses spring mattresses latex memory foam and hybrid options. It also sells pillows cushions and other related products.

Some popular products are OrthoMagic Klassic Supernova DuoRet and Spinekare. In FY25 new products were launched to target the lower price segment. Aaram under the Kurlon brand and Tarang under Sleepwell were introduced.

These are focused on the under ₹10,000 category to compete with unorganized players.

In June 2024 Kurlon also updated its logo for the first time in many years. The campaign was built around the line Life banegi Hula Hula.

On the distribution side the combined network of Sheela Foam and Kurlon is quite large. It now covers around 20,000 retail points.

This includes thousands of exclusive outlets and multi brand stores along with company owned stores. In just the first quarter of FY26 around 392 new showrooms were added. After the merger the company also reduced its manufacturing footprint.

Plants were cut down from 21 to 12 to improve efficiency. Factories are spread across multiple states in India and also in countries like Australia and Spain.

So overall the real mattress business is growing and expanding under Sheela Foam while KCPL has become more of an investment and new business vehicle.

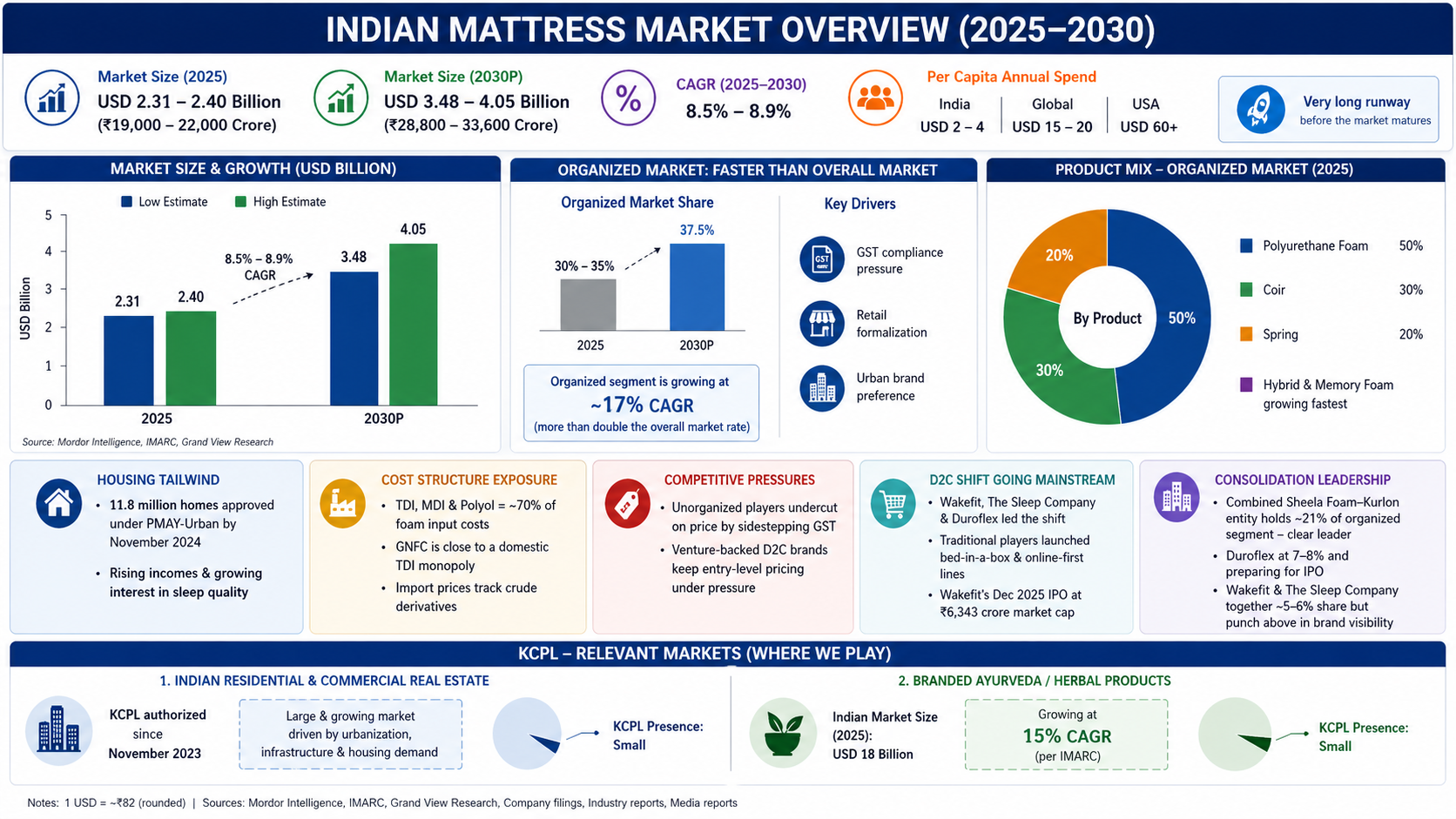

The Indian mattress market today is valued somewhere between USD 2.31 and 2.40 billion which is roughly ₹19,000 to ₹22,000 crore in 2025. Different reports suggest that this market can grow to around USD 3.5 to 4 billion by 2030 with a steady growth rate of around 8.5 to 9 percent. But the more interesting number is per person spending. In India people spend only around USD 2 to 4 per year on mattresses.

Globally this number is closer to USD 15 to 20 and in the US it goes above USD 60. This clearly shows that the market still has a long way to grow before it becomes mature.

Two big shifts are happening in this industry right now. First is the shift towards organized players.

Right now the organized segment is about 30 to 35 percent of the total market. But it is growing much faster at around 17 percent every year which is more than double the overall market growth. It is expected to reach around 37 percent share by 2030.

This growth is mainly coming from GST compliance better retail structure and people preferring branded products in cities.

Second shift is the rise of D2C brands. Companies like Wakefit The Sleep Company and Duroflex made this model popular.

Because of this traditional companies also had to launch their own online focused products and bed in a box options.

Wakefit IPO in December 2025 with a valuation of around ₹6,343 crore also gave a clear signal of how big this segment can become. Looking at product mix. Polyurethane foam has the largest share at around 50 percent in the organized market.

Coir has around 30 percent and spring mattresses around 20 percent. Along with that rising income levels and more awareness about sleep quality are helping demand grow. But there are some risks as well. Raw material costs are a big factor. Chemicals like TDI MDI and polyol form a large part of input cost.

Prices of these depend on crude oil trends. Also one major supplier has strong control in the domestic market which affects pricing.

Unorganized players still compete aggressively on price since they can avoid taxes. At the same time funded D2C brands keep pressure on pricing especially in the entry level segment.

Competition in the industry is getting more concentrated. The combined Sheela Foam and Kurlon entity now holds around 21 percent share in the organized market. This includes about 13 percent from Sleepwell and around 8 percent from Kurlon earlier.

This makes it the clear market leader. Duroflex is next with around 7 to 8 percent share and may go for an IPO soon.

Wakefit and The Sleep Company together have around 5 to 6 percent share but they are very strong in branding and visibility.

Now if we look at KCPL. Its focus markets are different. It is now allowed to operate in real estate from November 2023.

It is also present in ayurveda and herbal products where the Indian market is estimated around USD 18 billion and growing fast.

But in both these areas KCPL is still very small right now.

KCPL board (as of FY25 filings):

| Name | Role | Background |

|---|---|---|

| T. Sudhakar Pai | Managing Director, Promoter | Pai family patriarch; Manipal Group veteran |

| Jaya Pai | Director, Promoter | Pai family |

| Deepa Pai | Director, Promoter | Pai family |

| Jyothi Pradhan | Director, Promoter | Pai family |

| K.V. Shetty | Independent Director | |

| Madhusudan K.R. | Director and CFO | Long-tenure finance executive |

| Santhosh Kamath | Independent Director | |

| Susheela Godbole | Company Secretary | Compliance officer |

KCPL today works more like a family office that also follows basic company rules like having independent directors. There is no involvement from Sheela Foam in its board. No executive from that side is part of KCPL anymore. Sudhakar Pai also stepped down from the KEL board in October 2023 when the deal was completed. That was the last real operational link between KCPL and the mattress business. So now both sides are completely separate. The actual Kurlon mattress business is being run by Sheela Foam. Rahul Gautam is the Chairman. His son Tushaar Gautam is the Managing Director and is now also handling CEO level responsibilities. Earlier the CEO Nilesh Sevabrata Mazumdar stepped down in July 2025 due to personal reasons. This happened in the middle of the integration phase which is an important point to notice.

Amit Kumar Gupta joined as Group CFO in 2023. He handled the fund raising through QIP and bonds which were used to finance the Kurlon deal. Shashwat Goswami joined in 2025 as CMO. He is responsible for managing brand strategy across both Sleepwell and Kurlon.

The CEO exit can be seen as a risk because integration was still ongoing at that time. This part is discussed in more detail later.

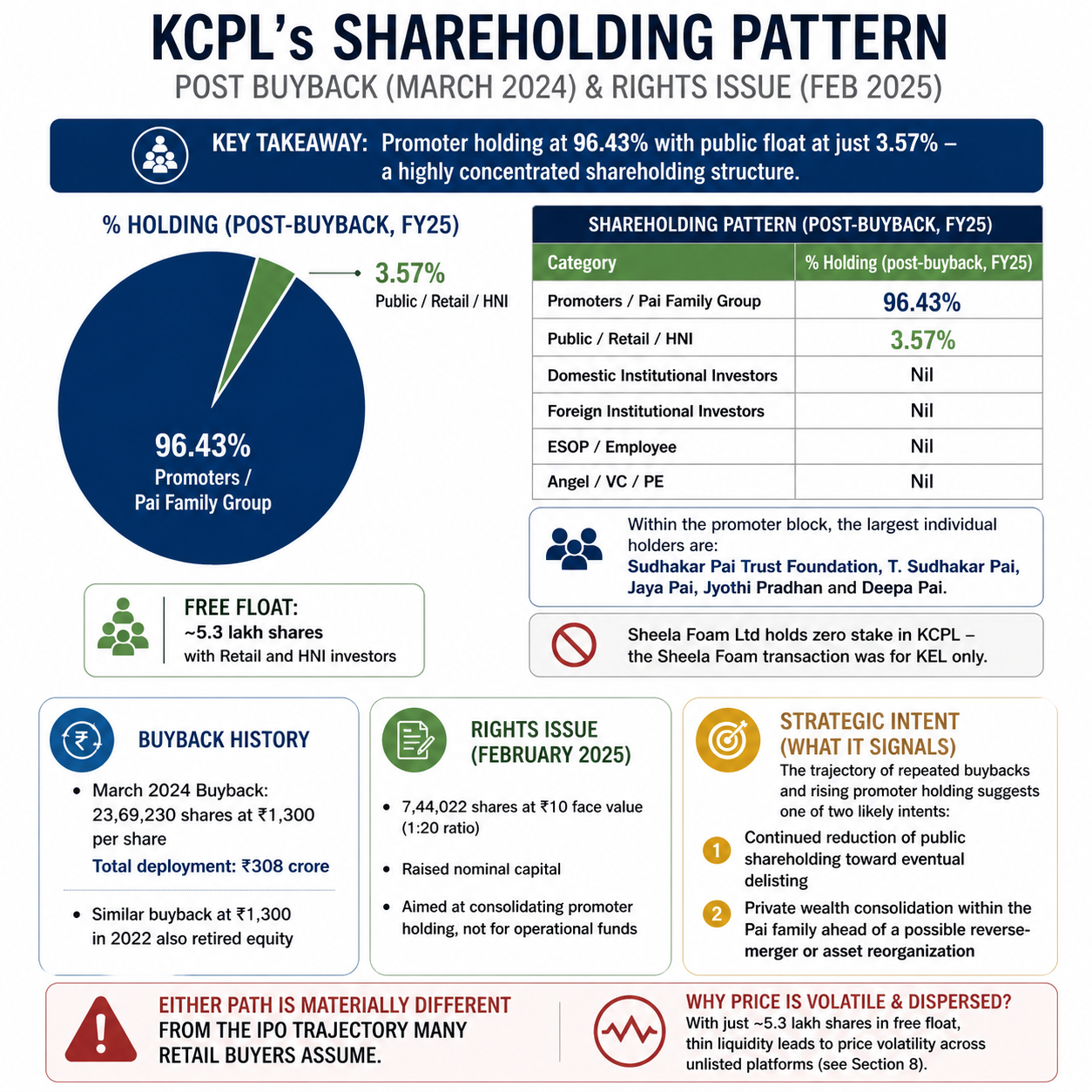

KCPL's shareholding pattern is the most telling data point in the entire investment case. After the March 2024 buyback of 23,69,230 shares at ₹1,300 per share (₹308 crore total deployment), promoter holding rose from 94.01% to 96.43%, with public float collapsing to a sliver.

| Company | FY25 Revenue (₹ cr) | FY25 PAT (₹ cr) | EBITDA margin | Mkt cap / Implied Valuation (Apr 2026) | Listed/Unlisted | Differentiating Edge |

|---|---|---|---|---|---|---|

| Sheela Foam Ltd (Sleepwell + Kurlon) | 3,439 (+15%) | 97 | 7% (Q3 FY26: 10.9%) | ~₹5,748 cr (P/E ~85x) | NSE: SFL | ~21% organized share; foam backward integration; pan-India; export footprint |

| Wakefit Innovations Ltd | 1,305 (+28%) | –35 (loss; H1FY26 PAT ₹35.6 cr) | ~7% | ~₹4,800 cr (P/S ~3.7x) | NSE listed Dec 2025 | Largest D2C; 129 COCO; 60% D2C revenue; 35% repeat customer |

| Duroflex Pvt Ltd | 1,153 (+4%) | 47.2 | ~7–8% | DRHP filed Nov 2025 (₹184 cr fresh + 2.25 cr OFS) | Unlisted (pre-IPO) | #3 by share; ~20% in South India; PE-backed (Norwest, Lighthouse) |

| Peps Industries Pvt Ltd | ~500 (target) | n/d | modest | ~₹1,500 cr (private estimate) | Unlisted | #1 in spring (54% share); Restonic license |

| The Sleep Company | 499 (+60%) | –51 (loss) | negative | ~$400–500M post Series D (₹480 cr Aug 2025) | Unlisted | Patented SmartGRID®; 150 EBOs; ChrysCapital, 360 ONE backed |

| Centuary Mattresses | ~253 (FY24); declining | declining | modest | private | Unlisted | Coir export leader; CertiPUR-US |

| Kanara Consumer Products Ltd | 107 (–78% YoY) | 75.3 | not meaningful (investment income) | ~₹1,156–1,449 cr (varies by platform) | Unlisted |

KCPL's standalone financials are split sharply between an exceptional FY24 and a normalized FY25 because the Kurlon sale gain dominated FY24 reporting.

| ₹ crore | FY23 | FY24 | FY25 |

|---|---|---|---|

| Revenue from operations | 79.5 | 71.9 | 22.7 (consol) / 107 (Tracxn standalone incl. other income) |

| YoY growth % | – | (10%) | (78%) |

| Total expenses | 84.2 | 67.4 | 49.3 |

| EBITDA | 1.8 | 4.5 | (estimated) modestly positive |

| EBITDA margin | ~2% | ~6% | not meaningful investment co. |

| Exceptional gain | – | 1,308.74 | – |

| Profit before tax | (4.8) | 1,519.55 | 96.85 |

| PAT | (3.2) | 1,165 | 75.3 |

| Net margin | n/m | 1,500%+ (one-time) | 70%+ (driven by other income) |

| EPS (₹) | (1.8) | 783.05 | 52.49 / 50.63 (post-buyback) |

The ₹1,308.74 crore exceptional gain in FY24 was the profit on sale of the KEL stake to Sheela Foam, plus ₹232.67 crore in liabilities written back. Strip the exceptional and core operations were modestly loss-making. FY25 PAT of ₹75.3 crore is largely interest and treasury income on the ₹600+ crore investment portfolio.

| ₹ crore | FY24 | FY25 |

|---|---|---|

| Trade receivables | 28.4 | 18.7 |

| Cash and bank balances | 482.78 | 30.81 |

| Current investments | 423.5 | 608.0 |

| Total debt | 14.0 | 0.0 |

| Shareholders' equity | 1,346 | 1,229 |

| Book value per share (₹) | 906 | 826.32 |

| Working capital | strongly positive | strongly positive |

The cash drop from ₹482.78 crore to ₹30.81 crore reflects the ₹308 crore buyback deployment and a redeployment into current investments. Debt is zero at FY25 end, making KCPL one of the most under-leveraged unlisted public companies of its size.

| ₹ crore | FY24 | FY25 |

|---|---|---|

| Operating cash flow | (15) | 18 |

| Investing cash flow | +1,930 (sale proceeds) | (200) (deployed in current investments) |

| Financing cash flow | (308) buyback + dividends | (15) |

| Ratio | FY24 | FY25 |

|---|---|---|

| ROCE | n/m (one-time gain) | 6.1% (treasury yield) |

| ROE | 87% (one-time) | 6.1% |

| Debt/Equity | 0.01 | 0.00 |

| Current ratio | 42.72x | 9.47x |

| Gross margin | 18% | n/m |

| Net margin | 1,500%+ | 70%+ (other income driven) |

| Receivables days | 144 | 300+ |

| P/E (at ₹900) | 1.15x (one-time distorted) | 17.8x |

| P/Sales (at ₹900) | n/m | 12.5x |

| P/BV (at ₹900) | 0.99x | 1.09x |

At KCPL which is the company retail investors actually hold shares in. Real estate development is the main new area they are trying to build. In November 2023 the company got approval to enter this space. During FY25 it also created two advisory committees for property related work. The first focus is to use and monetize the Gwalior plant land and other properties that were left after the mattress business was separated in 2014. As of now nothing has actually been developed yet.

The second area is ayurveda and herbal products. This is done through its subsidiary Manipal Natural Pvt Ltd. The company sells coir based products herbal items and wellness products online under the Manipal brand. Right now this business is still small and contributes very little to overall revenue. On the structure side there is some simplification happening.

In 2026 the company approved merging Manipal Natural and Kanara Consulting into the main KCPL entity. This is being done through a fast track process. It will make the structure simpler and more direct. Another important point is how the company is using its cash.

In the last three years it has done two buybacks. Both were done at ₹1,300 per share. This clearly shows that the promoters are returning excess cash back to shareholders instead of aggressively investing it into new businesses.

So even though the company has plans in real estate and other areas its actual actions so far show a more cautious and capital return focused approach.

At Sheela Foam (where the Kurlon brand and business actually sit):

The biggest risk here is confusion itself. Many buyers think they are getting exposure to the Kurlon mattress business.

But that is not true anymore. When this reality becomes clear the price of these unlisted shares can fall quickly.

There is no DRHP filed. There is no clear IPO timeline. At the same time promoter holding has gone up to 96.43 percent.

Because of this delisting looks more likely than listing right now. The public float is very small. Only around 5.3 lakh shares are available.

This means the price cannot handle heavy selling from retail investors. Even small selling pressure can move the price a lot.

The wide buy and sell spread in the market already shows this issue. Another point is the cash position. Right now a big part of company income is coming from interest on cash and investments.

But this may not last. In 2024 the company already used ₹308 crore for buyback. If they keep returning cash like this then future income from investments will reduce. The new business areas like real estate and ayurveda are still at a very early stage. There is no strong track record yet. So there is uncertainty on how these will perform at scale.

Competition from D2C brands is getting sharper. Wakefit is now listed after its December 2025 IPO.

Duroflex is also preparing to list. The Sleep Company has raised over 100 million dollars and is spending aggressively.

These are serious players now not small startups. Raw material risk is still a structural issue. Inputs like TDI MDI and polyol depend on global prices and crude oil trends. Sheela Foam usually passes on these costs to customers but there is always some delay. Because of that margins can get squeezed when prices move fast. The CEO transition is another risk to watch.

Mazumdar stepped down in July 2025 during the integration phase. Now most of the responsibility is on Tushaar Gautam.

At the same time the company still has a lot of synergies left to achieve. Working capital is also tight. The current ratio was around 0.64 times in Q3 FY26 which shows some pressure on liquidity. There is also a pending GST issue.

A notice of around ₹20.26 crore has been raised by the GST Intelligence department. This is still unresolved and adds another layer of uncertainty.

Net cash and investments per share are around ₹430. The share price is roughly ₹900. So almost 48 percent of the price is supported by cash itself. This is before giving any value to the real estate or ayurveda businesses. That creates a basic downside floor to some extent.

The buyback price of ₹1,300 also matters. It works like a soft reference point. It shows the level where promoters were comfortable putting money. At the same time it also acts like an informal ceiling for how much the valuation can stretch in the near term.

The company also has no debt. This gives flexibility for any future restructuring or new plans. They have room to move if they decide to change direction later.

India organized mattress segment is growing fast at around 17 percent every year. The combined company has about 21 percent share in this segment. That is large enough to have some control on pricing and market direction. The shift from unorganized to organized market is still in early stages.

This change is being driven by GST rules and better compliance. As more players move into the formal system organized companies benefit.

The move from unorganized to organized segment along with export growth in GCC markets and demand for premium products are all supporting growth together.

On top of that the company still has more synergies left to capture. Around ₹60 crore of benefits are still pending beyond what has already been achieved.

The instinct is understandable. Kurlon unlisted shares sound like an easy way to enter the organized mattress story in India.

But that is not what this is. The real mattress story is somewhere else. That 21 percent market share the ₹190 crore synergies the shift from unorganized to organized and the move towards 14 to 15 percent EBITDA margins all sit inside Sheela Foam.

If someone wants exposure to this theme that is the company to look at. Sheela Foam is not cheap though. It trades at around 85 times earnings based on FY25 which was a weak year.

But recent Q3 FY26 numbers show margins are starting to improve again. What platforms like Sharescart and Planify are selling under the Kurlon name is KCPL. And KCPL is a very different business. It has around ₹107 crore revenue and about ₹75 crore profit.

But most of that profit comes from interest income not operations. There is no IPO filing. Public shareholding is very small.

And the company has almost no debt.

In reality this is a Pai family investment holding company. It has a history in consumer products but now it is slowly moving into real estate and herbal products. Both of these are still early stage.

At current prices it trades close to 1.1 times its book value. So if someone bought this thinking it is a proxy for the mattress business

then they are holding the wrong asset. But if someone is looking at it differently as a low leverage company with strong asset backing promoter alignment and a past buyback level of ₹1,300 acting as a rough reference then the price range of around ₹777 to ₹900 can be evaluated on its own logic.

The most important takeaway from all this is clarity. There are four different entities involved and most people mix them up.

KCPL KEL KTIMPL now called Kanara Consulting and Sheela Foam They share history but not the same business anymore. Understanding this difference is what decides whether someone is buying a growing mattress company or just a holding company trading near its asset value.

Both are very different bets.

Independent Research Powered By - Actionable data

Apollo Green Energy Limited: Comprehensive Equity ...

February 2026

Excelsoft Technologies : Should you invest?

November 2025

The Booming India EV Industry : Where Future Lies ...

September 2025

Shakti Pumps: Powering Sustainable Solutions for a...

September 2025

Polycab India: A Rising Giant

August 2025

Difference between Stock Market and Share Market

February 2025