Comments: 0 | Likes: 0

When we talk about retirement planning many of you might ignore it and say “dekha jaayega”. But the truth is retirement planning is one of the most important financial steps in life and it should be started as early as possible. In this article, we will understand why retirement planning is so crucial and how unlisted shares can play a big role in making it successful. With this read we guarantee that you’ll gain new insights on how to manage your finances better and prepare not just for retirement but also for the kind of lifestyle you truly want.

Understanding Retirement Planning

Retirement planning is simply the planning of funds you will need when you completely stop working. In India most people retire around the age of 60 when the body no longer allows the same pace of work after that, what everyone truly desires is a peaceful, stress free life while maintaining the same lifestyle they built over years but without an active income.

And that’s exactly what retirement planning is, creating a pool of funds that can support you for decades after retirement this pool is usually a mix of:

Safe and stable investments like Fixed Deposits, Provident Fund and gold.

Dividend paying stocks that provide regular income and

High growth stocks that over the long term multiply wealth significantly

In India, the future life expectancy will be around 80 to 90 years because of medical advancements, which means after retiring at 60 you must plan for 20 to 30 years without active work.

Let’s take a simple example:

Monthly expenses today: ₹50,000

Retirement age: 60 years

Expected lifespan: 80 years

You will need at least:

₹50,000 × 12 months × 20 years = ₹1.2 croreBut this is just the minimum base number. It doesn’t account for:

Inflation (3% to 4% annually which can almost double expenses in 20 years)

Unforeseen costs like medical emergencies, lifestyle upgrades or family obligations.

Realistically, to maintain the same lifestyle, you may actually need 2 to 3 crore or more by the time you retire.

Also, people nowadays are trying to achieve their FIRE number (Financial Independence, Retire Early). This means retiring in their 40s instead of the traditional 60.

For example - A 25 year old working in a corporate job might want to retire by 40 and then become a mountain trekker, a nursery owner or even start a small cafe. These activities may not generate the same income as a full time job but they provide life satisfaction and meaning, so to make this possible such a person must save and invest in a way that not only covers essential expenses like marriage, children’s education and healthcare but also funds the dream lifestyle in which they may not earn much but the investments will cover the expenses.

Now, looking at retirement the traditional way in India, retirement planning is still not very popular because parents usually live with their children who take care of them. In contrast, in the USA the culture emphasizes independence but the reality is different. Studies show that out of 100 retirees nearly 80 end up depending on their children or external support due to lack of proper planning in the USA and this type of culture our next generation is trying to copy.

In India, families often rely on gold and real estate as retirement cushions. These assets not only secure retirement but also allow families to pass wealth to the next generation.

But sometimes we’ve all heard inspiring stories:

“Someone’s grandfather bought Infosys shares in the 1990s and today they’re worth hundreds of crores.”How did this happen?

By investing early in trusted and stable companies

By avoiding hype or speculative bets and

By staying invested patiently for decades.

This is the real power of retirement planning through equities. It ensures financial independence in old age while also creating generational wealth for children and grandchildren.

That’s where unlisted shares come in. When investors hold promising unlisted shares for the long term their wealth truly compound, especially when they identify multibagger companies that are often available only in the unlisted market (since many listed stocks are already overvalued).

Such companies not only provide compounding benefits but also large dividends. This wealth can then be used both for traditional retirement and for early retirement (FIRE)

which is becoming more popular as people move towards a society where they value personal happiness over “log kya kahenge.”However, while investing in unlisted shares you must watch out for certain risks:

Liquidity Risk: Some unlisted shares can be very hard to sell when needed making them unsuitable if you want quick access to money.

Company Risk: Many people invest in startups and risky companies without proper knowledge hoping to grow money quickly but for retirement planning the game is long term investing not short-term trading.

Instead, focus on well established, trustworthy, undervalued, unlisted companies where your hard earned money is safe

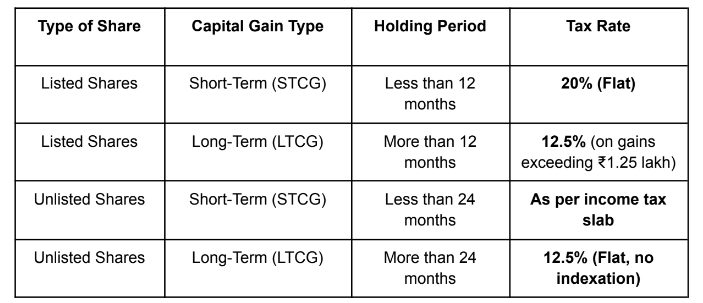

So what's left to understand… just taxation

Even if the stock later gets listed after an IPO it will still be taxed as per unlisted share rules.

(You can always compute which regime gives lower tax liability or simply ask your CA to guide you.)

Conclusion

In the end, always remember to invest wisely, not greedily.

The unlisted market is a long-term game of venture style investing but in the public domain. Always weigh the risks and rewards before committing. Ask yourself: Does this investment deserve my hard-earned money?If chosen wisely these hidden gems can not only fund your retirement and early retirement but also help you leave behind a legacy.

To explore such opportunities, visit Sharescart.com India’s No. 1 platform for unlisted shares where you can discover the hidden companies of tomorrow.

I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Stocx Research Club). I have no business relationship with any company whose stock is mentioned in this article.

I am not a SEBI Registered individual/entity and the above research article is only for educational purpose and is never intended as trading/investment advice.

Articles

Comments